PMIs Rebound: Bringing Both Optimism and Caution

4 Min. Read Time

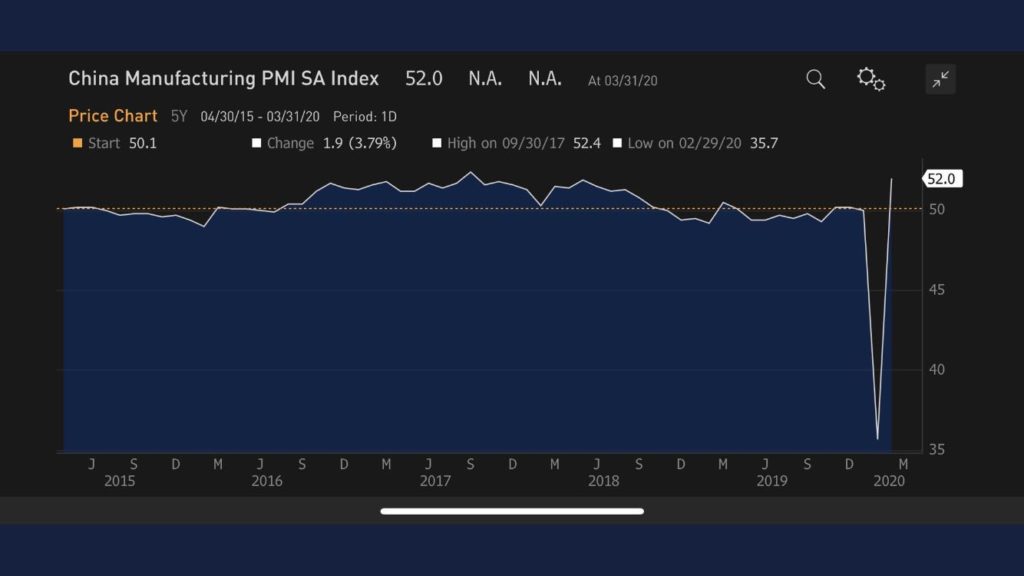

PMI Data Shows Surprise Expansion

| Manufacturing PMI | 52 versus estimate 44 and Oct’s 35 |

| Non-Manufacturing PMI | 52.3 versus estimate 42 and Oct’s 29.6 |

Takeaway: This is a massive uptick versus analyst expectations. PMIs are calculated on a month to month basis which helps explain the jump. The National Bureau of Statistics compiles the “official” PMI by surveying several thousand large and mid sized companies, many of which are State Owned Enterprises. Caixin China PMIs are calculated by IHS Markit (a NYSE publicly traded company) by surveying several hundred small private companies. The government mandated SOEs go back to work first, while private companies were much slower to do so. I would suspect that, for this reason, the Caixin PMIs won’t show as robust of a rebound when released on Thursday. Skeptics of Chinese data will have a field day on this data release, although it proves they might not fully understand how the data is calculated. Commodity prices including copper rallied on the news, lending validity to the release. However, the data wasn’t all roses as input/output prices were weak and lessened export orders raises the concern that China will be adversely effected by the global economic slowdown. This is a very valid concern, as even the NBS commented on it and voiced a very cautious tone in its outlook. Business expectations in both releases were quite strong, providing some optimism.

Key News

Asian equities were largely higher following the strong US performance on Monday. Outliers included Japan, as brokers noted a lack of buying from the Bank of Japan which owns an exceedingly high percentage of local equity ETF AUM, and Australia. The cautious tone of the NBS weighed on sentiment, despite the strong March data. The HK market continues to come off a very oversold position as a local media source noted the Hang Seng traded below book value during March. The market overlooked the release of HK retail sales -44% in February as energy companies rode a bounce in oil prices. Alibaba’s HK stock price (9988 HK) rose +1.72% while Tencent (700 HK) +0.96% and Meituan Diangping (3690 HK) rose +6.42% following yesterday’s earnings announcement. The mainland markets had light volume as investors try to balance the effect of China’s increased stimulus versus the effect of the global economic slowdown.

What will the next round of China stimulus look like? We have clues based on recent statements from the government that it could include: running a budget deficit, issuing special Treasury bonds for the third time, and infrastructure. This is accompanied by loose monetary conditions, emphasizing business lending by banks and support for private companies. One broker puts the combination of fiscal, monetary and easing policies at more than 10% of GDP. There is no question that policy makers are looking to support the economy in advance of global economic weakness. The key questions will be how quickly can the US and Europe contain their outbreaks and what effect will stimulus measures have in offsetting weakness.

E-commerce company Pindouduo (PDD US) announced it is selling $1.1 billion worth of newly issued shares to undisclosed investors. The new shares increase the company’s shares by 2.8%. What we don’t know is what discount the investors received versus the current share price.

H-Share Update

The Hang Seng closed +1.85%/+428 index points, nearly exactly where it opened, although not before a mid-day slump almost pushed the index into negative territory. The late afternoon rally brought the index back to 23,603 on volumes +5% from yesterday with strong breadth of 47 advancers and 3 decliners. Top index movers were AIA +2.93%/+71 index points, China Mobile +3.13%/+33 index points and China Construction Bank +1.6%/+33 index points. Today’s top performers were PetroChina +8.4%/+15 index points, Sino Land Company +7.42%/+6.9 index points and energy giant CNOOC +7.4%/+32 index points. The Hang Seng’s two pharma names, CSPC and Sino Biopharma, were off -4.32%/-9.5 index points and -4.31%/-10 index points following the latter’s earnings release, which came in below expectations. HSBC was also off -0.79%/-17 index points.

HK and Chinese domiciled companies traded in-line with each other, +2.17% and +2.05% respectively, using the HS HK 35 and HS China Enterprise as proxies. The Chinese companies listed in HK within the MSCI China All Shares Index were up +2.11% led by energy +5.64%, tech +3.38%, discretionary +3.03%, real estate +3.01%, industrials +3%, staples +2.42%, materials +2.34%, utilities +1.89%, financials +1.83%, communication +1.39% and health care +0.41%. Southbound Connect volumes were light but buyers still outpaced sellers. Volume leader Tencent had sellers outpace buyers by a small margin, Meituan Diangping had buyers outpace sellers by a small margin and SinoPharma had sellers outpace buyers by a small amount. Mainland investors bought $235mm of HK stocks today as Southbound Connect trading accounted for 8% of HK turnover.

A-Share Update

The Shanghai and Shenzhen Stock Exchanges traded in a tight range all day, closing at +0.11% and +0.51% as volume slumped -11%, below its 1-year average for the first time since 12/31/2019. Breadth skewed negative with 1,505 advancers and 2,089 decliners as large caps lagged mid and small caps. The mainland stocks within the MSCI China All Shares Index gained +0.49% led by staples +4.01%, health care +1.39%, materials +0.81%, energy +0.7%, , utilities +0.65%, communication +0.45% and discretionary +0.1%. Real estate was off -1.2%, financials -0.79%, industrials -0.55% and tech -0.31%. Northbound Connect volumes were light, although foreign investors bought mainland stocks more than they sold. Shenzhen Connect volume outpaced the Shanghai’s but only by a small margin. Volume leader Kweichow Moutai had 4 to 1 buying, Jiangsu Hengrui Medicine had buyers outpace sellers by a small margin, and Ping An had buyers outpace sellers by 1.5 to 1. Foreign investors bought $232mm of mainland stocks today as Northbound Connect accounted for 5.6% of the mainland’s turnover.

Last Night’s Prices & Yields

- CNY/USD 7.10 versus 7.09 yesterday

- CNY/EUR 7.77 versus 7.85 yesterday

- Yield on 1-Day Government Bond 1.20% versus 1.24% yesterday

- Yield on 10-Year Government Bond 2.67% versus 2.7% yesterday

- Yield on 10-Year China Development Bank Bond 3.12% versus 3.17% yesterday

- Commodities were higher on the Shanghai & Dalian Exchanges with most metals higher, although Dr. Copper was +1.81%