Alive & Kicking

3 Min. Read Time

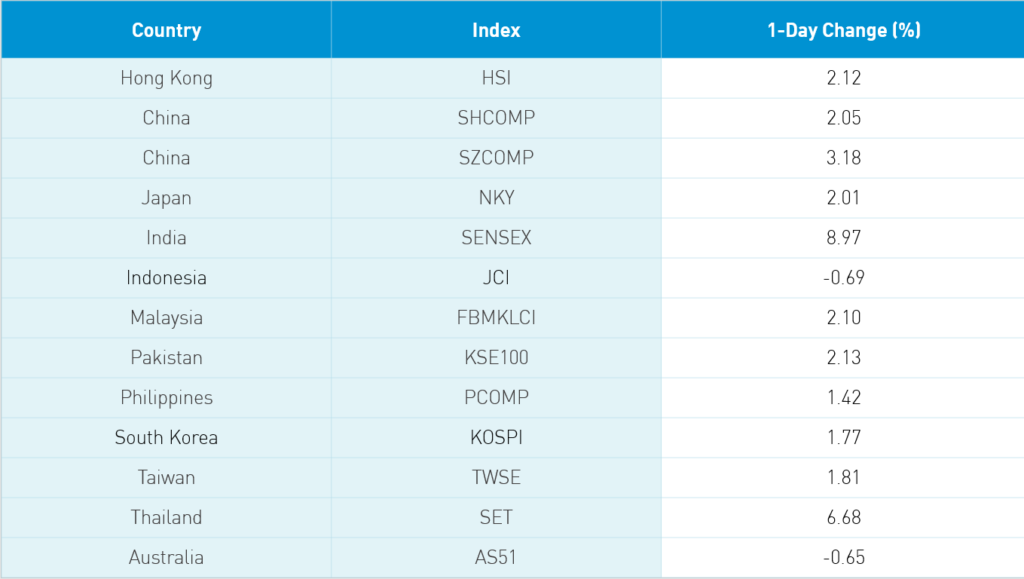

Key News

Asian equities followed Wall Street higher last night as investors cheered declining rates of coronavirus growth in Europe and New York City, details on further stimulus from other countries, and strong earnings releases coming out of South Korean from MSCI Emerging Markets behemoth Samsung. Japan managed a positive day on news of stimulus rather than increased quarantine measures. India returned from yesterday’s market holiday in very good spirits gaining nearly 8% while Mainland China returned with only 2-3% gains though the breadth was incredible with only 88 declining stocks. The PBOC announced another cut to the bank reserve requirement ratio after Friday’s close, demonstrating the central bank’s commitment to support private companies by freeing up banks’ cash to make loans.

Mainland China also benefited from a very strong inflow from foreign investors, who bought $1.79 billion worth of Mainland stock. Increased infrastructure stimulus in China had investors buying materials in both China and Hong Kong. Hong Kong volume leaders Tencent, Alibaba HK and HSBC rebounded +1.63%, +1.54% and +3.08%, respectively. It is worth noting that the value of shares traded in Tencent was twice that of the shares traded in Alibaba. Investors continue to voice displeasure with HSBC on its dividend cut and suspect that it may make up for the missed April payment later in the year.

An old friend Kenneth with ICBC in Hong Kong noted that many rallies following steep declines are led by the lowest quality names. I note this as several names that are clearly in the pain cave such as airlines and casinos fared well today. I didn’t hear much about short covering, but one should assume it is occurring as well.

Today’s title is inspired by the old Simple Minds song. We are not out of the woods yet as the economic consequence of coronavirus will begin to show up in Q1 economic releases and corporate earnings over the coming weeks. The data is going to be awful, which is why my favorite sector continues to be health care followed by asset light, growth companies in the internet space. What companies are seeing a pick up in usage? Clearly health care. I read an interesting article from the Bangkok Post that 8,950 Chinese companies are now producing masks to meet global demand. China is now generating a staggering 116mm masks a day! A broker noted Indian healthcare names had a strong day as well. What are we are going to do while quarantined? We still need groceries (e-commerce), likely conversing more via social media, downloading TVs/movies/music and playing more video games. Markets are moving in unison showing that macro headlines will drive stock prices though we are apt to see a breakdown as investors discern winners and losers.

China’s March FX reserves were announced overnight with $3.060 trillion versus estimate of $3.097 trillion and Feb’s $3.106 trillion. Plenty of dry powder is an understatement.

H-Share Update

The Hang Seng opened +1.45% higher but drifted to an intra-day low of +0.2% before rallying in the afternoon session close just off the highs at +2.12% at 24,253. Volume surged 45% back 1/3 higher than the 1 year average while breadth was strong with 49 advancers and 1 decliner. The index was led by AIA +2.54%/+64 index points, HSBC +3.08%/+61 index points and Tencent +1.63%/+42 index points. Macau casino operator Galaxy Entertainment was the best performer +735%/+2 2 index points with snack food maker Want Want China Holdings +7.13%/+7 index points. HK conglomerate Swire Pacific was off -1.26%/-0.9 index point. Chinese domiciled companies outperformed Chinese domiciled companies +2.56% versus +2.02% using the HS HK 35 and HS China Enterprise as proxies. The Chinese companies within the MSCI China All Shares +2.14% led by materials +5.36%, discretionary +4.12%, staples +3.22%, industrials +3.19%, real estate +2.72%, tech +2.53%, health care +2.36%, communication +1.78%, financials +1.57%, utilities +1.4% and energy +0.69%. Southbound Connect volumes were moderate with mainland investors trimming HK positions. Volume leader Tencent had 2 to 1 sellers, smart phone maker Xiaomi 3 to 1 sellers while HSBC had 10 to 1 buyers. Mainland investors sold $60mm of HK stocks today.

A-Share Update

The Shanghai & Shenzhen opened higher and grinded higher following yesterday’s market holiday +2.05% and +3.18% with both indices closing above the 2,800 and 1,700 levels. Volumes picked up 28% from Friday while breadth was very strong with 3,680 advancers and 88 decliners. Mid and small caps outperformed large and mega caps. The mainland stocks within the MSCI China All Shares gained +2.97% led by materials +4.04%, communication +3.83%, staples +3.62%, industrials +3.41%, tech +3.37%, health care +3.31%, discretionary +2.64%, energy +2.46%, financials +2.05%, real estate +1.7% and utilities +2.15%. Northbound Connect volumes were elevated though the level of buying was very strong. On Shanghai Connect, MSCI inclusion stock Kweichow Moutai was the top volume leader with 2 to 1 buying. On Shenzhen Connect, liquor maker Wuliangye Yibin was the volume leader with 3 to 1 buying followed ventilator maker Shenzhen Mindray with 2 to 1 buying. Foreign investors bought $1.79 billion of mainland stocks today.

Last Night’s Prices & Yields

- CNY/USD 7.05 versus 7.09 yesterday

- CNY/EUR 7.69 versus 7.67 yesterday

- Yield on 1-Day Government Bond 0.68% versus 0.82% on Friday

- Yield on 10-Year Government Bond 2.51% versus 2.60% on Friday

- Yield on 10-Year China Development Bank Bond 7.05% versus 7.09% on Friday