All Quiet on The Western Front

3 Min. Read Time

We will be hosting a webinar on the human, economic, and market impact of COVID-19 on China and the world this morning at 11 am EST. CFP & CIMA CE credit is available.

Please click here to sign up!

Key News

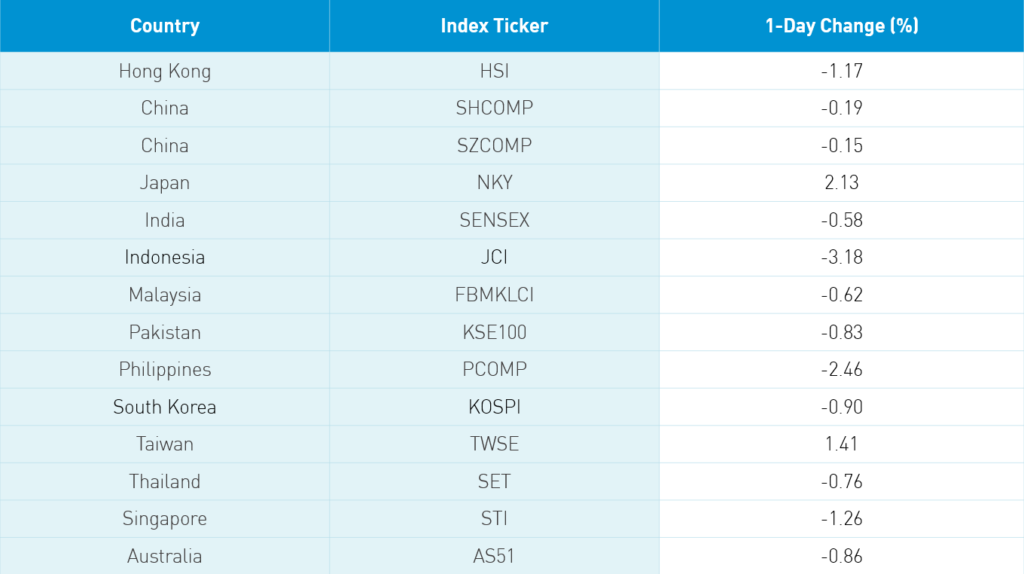

Asian equities were largely lower following the S&P 500’s big intraday reversal. Japan and Taiwan were the only positive performers. The downdraft was on light volumes, which is good news for bulls. While most countries registered small losses, Indonesia, the Philippines, and Thailand had especially difficult sessions. India was off slightly after big gains yesterday though one broker noted the strength of India pharma stocks on rumors that the country’s manufacturers would increase exports of drugs to the US. Hong Kong announced its $18 billion stimulus plan to support displaced workers after the market’s close. Tencent (700 HK) was the most heavily traded security by value -0.67% while Semiconductor Manufacturing (981 HK) +5.12% and Meituan Dianping (3690 HK) -0.77%. Alibaba HK (9988 HK) was off -0.73%. Ping An Healthcare and Technology (1833 HK) was up +3.59% after announcing an English version of its tele-doctor service.

After the close, Apple supplier AAC Tech (2018 HK) pre-announced that Q1 earnings would fall 85% to 90% due to work stoppage. The company did say its operations got back up and running by mid-March. Telecom was weak on chatter that smartphone buyers are waiting for a broader 5G rollout prior to buying new phones. Mainland China was off slightly though both the Shanghai and Shenzhen closed above the 2,800 and 1,700 levels. ZTE (000063 CH), which makes 5G equipment, was the most heavily traded stock by volume off -1.37% which makes 5G equipment while ventilator manufacturer Jiangsu Yuyue Medical (00223 CH) saw profit-taking off -5.48%.

Yesterday, a short-selling firm announced that Baidu spin-off iQIYI (IQ US) was inflating their user data. The stock fell on the news -13% but rebounded strongly closing up +3.22%. Baidu still owns the majority of IQ while several very prominent active investors are amongst the holders, unlike Luckin Coffee. After the close, TAL Education (TAL US) announced an employee had inflated sales in a non-core business unit and been arrested by the police. The unit, not involved in the company’s core classroom and online courses, comprises a small percentage of revenues of around 3%. I suspect the employee’s compensation had been tied to sales within the business to business unit, which may have led to the fraudulent activity. Regardless it is a reminder of why investors want to be diversified. On the positive front, I read an article about consumer pent demand leading to an uptick in e-commerce activity following China’s quarantine.

H-Share Update

The Hang Seng was off all day with the market slumping into the close -1.17%/-282 index points to close at 23,970. Volumes were off -25% from yesterday while breadth was dismal with only 2 advancers and 47 decliners. The biggest index contributors were China Mobile -2.69%/-30 index points, China Construction Bank -1.11%/-22 index points, and Industrial & Commercial Bank of China (ICBC) -1.9%/-21 index points. Techtronic Industries was +2.33%/+5 index points while telecom China Unicom was the worst performer -3.37%/-3 index points with Sunny Optical -3.28%/-7 index points. Hong Kong companies outperformed Chinese companies -0.76% versus -1.68% using the HS HK 35 and HS China Enterprise indexes as proxies. The Chinese stocks listed in Hong Kong within the MSCI China All Shares Index lost -1.25% led lower by energy -2.28%, real estate -1.91%, staples -1.82%, discretionary -1.58%, materials -1.53%, financials -1.39%, tech -1.38%, communication -1.07%, utilities -0.54%, industrials -0.3% and health care -0.2%. Southbound Connect volumes were light though buyers were back. Volume leader Tencent had 2 to 1 buyers, Semiconductor Manufacturing (SMIC) had 2 to 1 buying and China Construction Bank had 7 to 1 buying. HSBC also had very large buying today. Mainland investors bought $303mm worth of Hong Kong stocks today as Southbound Connect trading accounted for 9.4% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen had a choppy day opening lower, rebounding and then stalling to close -0.19% and -0.16%, respectively, as volume decreased nearly 8% from yesterday. Breadth wasn’t that bad with 2,182 advancers and 1,419 decliners. Performance amongst large, mid and small caps was fairly uniform as sector exposure was the big driver of stock dispersion, which tends to be the case. The Mainland stocks within the MSCI China All Shares Index were off -0.54% led lower by communication -1.17%, staples -1.07%, real estate -0.79%, financials -0.79%, discretionary -0.72%, materials -0.28%, utilities -0.24%, health care -0.24%, tech -0.17% and industrials -0.11%. Northbound Connect flows were light as foreign investors were slight sellers of mainland stocks. MSCI inclusion stocks diverged with Kweichow Moutai seeing 7 to 5 buyers while Ping An was sold 4 to 1. Foreign investors sold $488mm worth of Mainland stocks as Northbound Connect trading accounted for 4.5% of mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 7.06 versus 7.05 yesterday

- CNY/EUR 7.69 versus 7.67 yesterday

- Yield on 1-Day Government Bond 0.81% versus 0.67% yesterday

- Yield on 10-Year Government Bond 2.48% versus 2.51%

- Yield on 10-Year China Development Bank Bond 2.82% versus 2.88% yesterday

- Commodities on the Shanghai & Dalian Exchanges were mixed with Dr. Copper pulling a James Bond -0.07%.