Follow The Leader

2 Min. Read Time

Key News

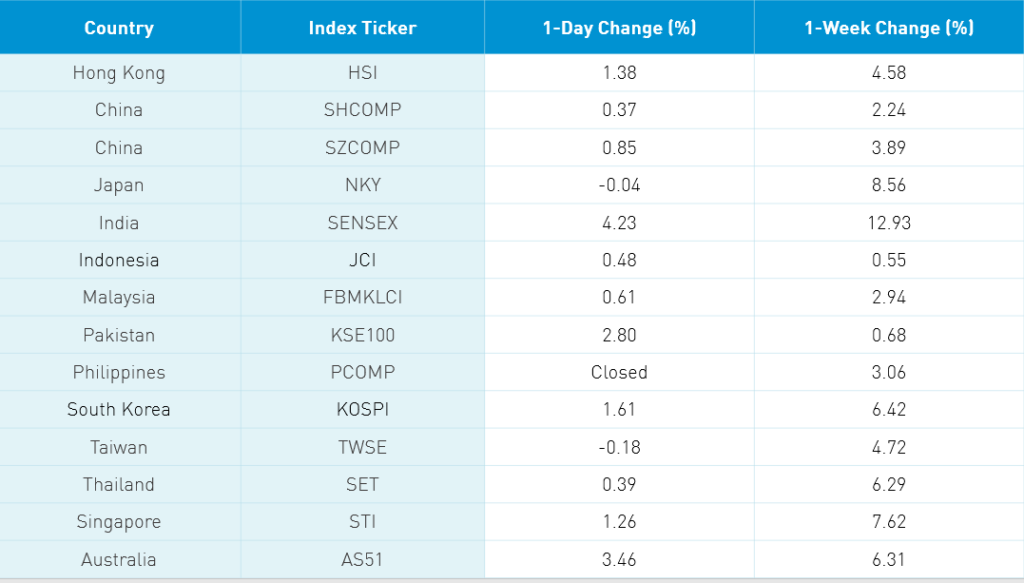

Asian equities followed the US higher today after India enjoyed another strong session. South Korea had a nice rebound though foreigners continued to sell. This was a head scratcher for me as China is FIFO (First In First out) SK is SISO (Second In Second out) with regard to coronavirus. The Hong Kong government’s stimulus package and subsequent financial liquidity injection led to a solid session as well. Macau casino stocks gained as traders focused on capturing pent up demand and bottom fishing rather than Hong Kong stimulus benefitting the companies.

The market shrugged off Apple supplier AAC’s pre-announcement that their revenue is going to fall 80 to 90% in Q1. It does give you a sense of what could be in store for Q1 earnings. Tencent was Hong Kong’s most traded security by value +1.66% as a new round of online games having been approved in China should benefit the company along with Netease and other gaming companies. Alibaba HK +0.8% was the second-highest volume security in Hong Kong. Healthcare had another strong day in both the Mainland and Hong Kong. The Mainland’s communication sector was led higher by 5G related companies while auto EVs had a strong day as Hanian, the Hawaii of China, announced an EV push.

In yet another sign that China has recovered from COVID-19, cosmetic sales saw an uptick in March compared to other retail sectors. Jeffries analysts noted that the cosmetics sector declined by only 20% against other retail in March compared to 60% to 80% in February. Evidently, people are leaving their homes and beginning to care about their appearance again.

Bilibili (BILI US) announced this morning that Sony will take a 4.98% stake in the online entertainment platform known for its live streams of people playing video games. The deal is worth $400mm and comes on the heels of Tencent raising its stake in HUYA.

Hong Kong will be closed Friday and Monday while Mainland China will be open. I’m sure that the last month or so has been mentally exhausting for you as well. Enjoy the three day weekend!

H-Share Update

The Hang Seng had a strong day grinding higher into the close +1.38%/+329 index points to close at 24,300. Volumes were slightly higher than they were yesterday and the 1-year average while breadth was strong with 46 advancers and 3 decliners. HSBC rebounded +2.76%/+55 index points followed by Tencent +1.66%/+43 index points and Macau casino operator Galaxy Entertainment +6.31%/+19 index points. Sands China was the day’s best performer +7%/18 index points while AAC slumped -4% after yesterday’s pre-earnings announcement warning. Hong Kong-domiciled stocks outperformed China-domiciled stocks for the third day in a row +1.94% versus +1.33% using the HS China Enterprise and HS HK 35 indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index +1.5% led higher by discretionary +4.31%, staples +2.74%, industrials +2.35%, health care +2.3%, utilities +1.86%, energy +1.83%, real estate +1.62%, communication +1.36%, materials +1.32%, financials +0.72% while tech lost -0.13% weighed down by AAC and Xinjyi Solar (-1.97%). Southbound Connect was a rare sale day though volumes were light. Volume leader Tencent was off 2 to 1, Ping An was sold heavily, and Sunac was bought 2 to 1. Mainland investors sold $72mm worth of Hong Kong stocks today as Southbound Connect accounted for 8.9% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen gained +0.37% and +0.85%, respectively, as both indexes edged above 2,800 and 1,700 levels on volume off from yesterday but still above the 1-year average. Breadth was positive with 2,458 advancers and 1,043 decliners as small caps and mid-caps outperformed large caps. The Mainland stocks within the MSCI China All Shares Index gained +0.6% led by health care +3.1%, communication +1.25%, discretionary +0.91%, financials +0.58%, staples +0.56%, materials +0.26%, and industrials +0.24%. Real estate was off -0.53%, tech -0.34%, utilities -0.28% and energy -0.15%. Northbound Connect was closed today.

Last Night's Prices & Yields

- Yield on 1-Day Government Bond 0.68% versus 0.81% yesterday

- Yield on 10-Year Government Bond 2.52% versus 2.48% yesterday

- Yield on 10-Year China Development Bank Bond 2.86% versus 2.82% yesterday

- CNY/USD 7.05 versus 7.07 yesterday

- CNY/EUR 7.71 versus 7.68 yesterday