Friday Profit-Taking, Week In Review

4 Min. Read Time

Week In Review

- On Monday, policy developments lent themselves to positivity in Mainland markets. As expected, the PBOC cut its 1 and 5-year Loan Prime Rates (LPR) by 20 bps and 10 bps, respectively, to 3.85% and 4.65%. Investors also looked favorably upon new policies for salient investing themes such as 5G, AI, and big data.

- On Tuesday, oil’s plunge shocked the world as Brent Crude dipped below $20 per barrel and futures for May delivery turned negative. As the world’s top energy importer, China may see some advantages in low crude prices. However, China's investments in oil exploration and production may suffer.

- On Wednesday, Kweichow Moutai, the largest liquor company in the world and the top constituent in the MSCI China A Index by weight, announced 2019 results that beat most estimates. The company announced revenue growth of 15.5%.

- On Thursday, energy and cyclicals rebounded. It was also confirmed that Chinese equities exhibited the lowest volatility over the past 30 days among major global markets. 30-day volatility in the S&P 500 Index came to 74 compared to 26 for the Hang Seng Index.

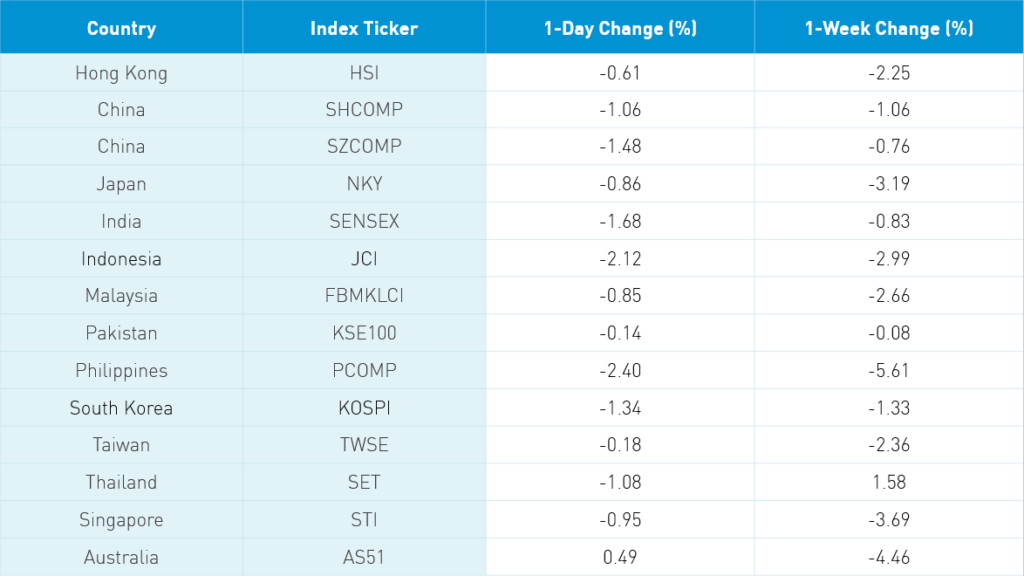

Key News

Asian equities ended an off week with a thud following the US equity markets lower on news of Gilead’s failed COVID-19 drug trial, US jobless claims, and Intel’s disappointing earnings announcement delivered after the US close. Japan has extended its quarantine. However, the country may be compelled to open up relatively soon considering that the Golden Week holiday begins on May 4th. Chinese automakers received good news after the Ministry of Finance announced that EV purchase tax breaks would be extended. Bellwether Ping An Insurance fell after announcing that Q1 net income fell -43% year over year, which caused the company’s Hong Kong and Mainland share classes to fall by -0.96% and -2.3%, respectively.

After the Mainland market closed, the PBOC announced a 20bps cut in the Targeted Medium Loan Facility, which loans to smaller banks, to 2.95%. The previous TMLF loans expiring today were larger than the newly issued loans. This suggests that there is plenty of liquidity in the banking system and that the PBOC has seen fit to dial back support to some extent.

Sectors that have recently outperformed in Mainland China and Hong Kong such as healthcare and tech were weak in what might be an emerging pattern of profit-taking on Fridays. In Hong Kong, the most heavily traded stocks were Tencent (700 HK) -1.26% and Alibaba (9988 HK) -3.13%. Meanwhile, the IPO of biotech name Akeso (9926 HK) rose by 50%.

Macau casino names were also weak on the day. However, I expect the stocks to garner a great deal of interest leading up to the May 1st Mainland holiday. Will Chinese gamblers return to Macau? With international travel curtailed, there is a good chance.

US-listed Chinese companies were weak yesterday after the market took note of an SEC release that had been issued a few days ago. The release highlighted three longstanding issues with US-listed Chinese companies: 1) the companies only issue audited financials annually versus quarterly, 2) PCAOB cannot audit the work of auditors in China and 3) the SEC has no recourse to prosecute a company’s management. I found the release to be fair and balanced. The SEC is making sure investors are aware of these risks following the Luckin Coffee fraud. The release also speaks to the size of China’s economy and rising weight in global indexes. There is a real opportunity to put these issues to bed through better communication.

NAVER (035430 KS) is a South Korean technology conglomerate with business lines including web search, instant messaging, online videos, and a digital comics platform called NAVER WEBTOON. The company reported strong Q1 financial results led by operating revenue growing 14.6% year over year and net income jumping 54% YoY. However, the company did see declines on a quarterly basis due to South Korea’s quarantine with operating revenue off -3.1% and net income off -31.3%.

H-Share Update

The Hang Seng opened lower and stayed put to close -0.61%/-145 index points at 23,831 on light volume equal with yesterday’s volume and just a touch above the 1-year average. Breadth was off with only 10 advancers and 39 decliners. The index was led lower by Tencent -1.26%/-34 index points, Ping An Insurance -0.96%, and China Mobile -0.73%/-8 index points. Apple supplier AAC Technology was the day’s best performer +2.88%/+2 index points while Wharf Real Estate was the day’s worst performer -3.44%/-3 index points. Hong Kong-domiciled companies declined -1.07% while China-domiciled companies were off -0.49% using the HS HK 35 and HS China Enterprises indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index lost -0.85% with only utilities +1.26% while energy was off -0.2%, discretionary -0.29%, financials -0.39%, staples -0.54%, materials -0.81%, industrials -0.94%, real estate -1.01%, communication -1.17%, tech -2% and health care -2.33%. Southbound Connect volumes were light in mixed trading. Volume leader Tencent was bought nearly 3 to 1 while Semiconductor Manufacturing was sold 2 to 1. Mainland investors bought $62mm worth of Hong Kong-listed stocks today while Southbound Connect trading accounted for just over 8% of turnover in Hong Kong.

A-Share Update

The Shanghai & Shenzhen were off -1.06% and -1.48%, respectively, as volume increased by 10% from yesterday and came in above the 1-year average. Breadth was terrible with just 644 advancers and 3,077 decliners with large caps declining slightly less than mid and small caps. The Mainland stocks within the MSCI China All Shares Index lost -0.9% with utilities and staples +0.45% and +0.2% while materials -0.29%, discretionary -0.7%, industrials -0.82%, financials -1.05%, real estate -1.1%, communication -1.22%, tech -1.68%, energy -1.77% and health care -1.84%. Northbound Connect volumes were moderate as foreign investors were active buyers of the Mainland stock market. Volume leader and MSCI Inclusion stock Kweichow Moutai saw buyers outpace sellers by a small amount. Meanwhile, Ping An Insurance was sold by a small amount. Foreign investors bought $459mm worth of Mainland stocks today, bringing the weekly total to $341mm. Foreign trading of Mainland Chinese stocks via Northbound Connect accounted for 4.4% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 7.08 versus 7.07 yesterday

- CNY/EUR 7.65 versus 7.66 yesterday

- Yield on 1-Day Government Bond 0.61% versus 0.56% yesterday

- Yield on 10-Year Government Bond 2.51% versus 2.52% yesterday

- Yield on 10-Year China Development Bank Bond 2.80 % versus 2.82% yesterday

- Commodities on the Shanghai & Dalian Exchanges were lower with Dr. Copper +0.24%