Earnings Lead Hong Kong Higher, JD.com Prepares Secondary Listing

3 Min. Read Time

Key News

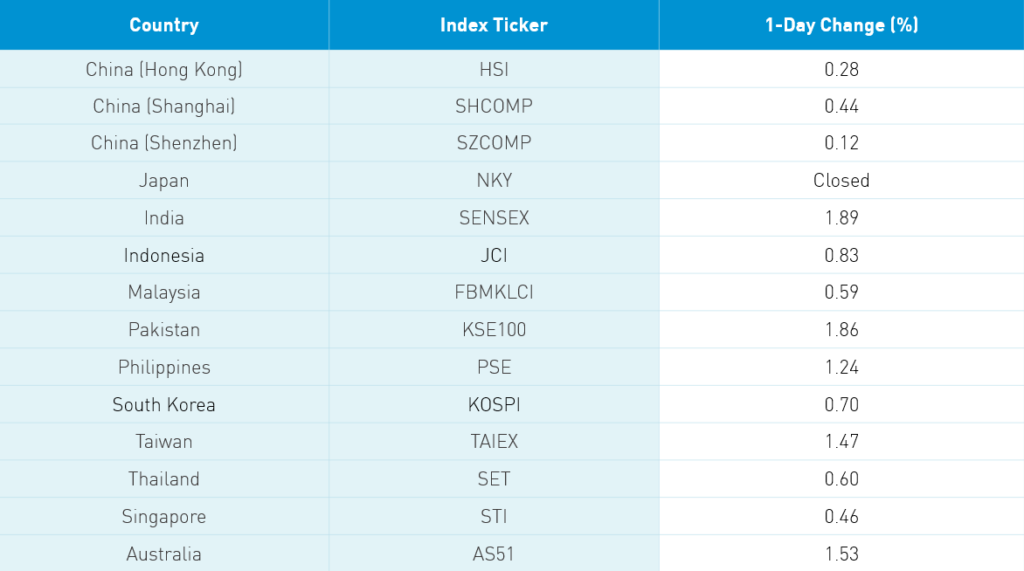

Asian equities had a nice uptick on light volumes as investors prepare for Japan’s closure for Golden Week holidays. Hong Kong closed out its week and month buoyed by earnings. No new cases for four days in a row raises the probability of the quarantine being lifted. Hong Kong retailers and real estate firms rallied on hopes that the quarantine could be lifted.

Standard Chartered (2888 HK) gained +6.17% after releasing earnings and joining the ranks of global banks posting decent earnings while raising loan provision reserves. BYD (1211 HK) had a strong day +7.73% after releasing an optimistic outlook for EV and auto sales, projecting a rebound in the second half of 2020. Auto names helped lead the discretionary sector higher. However, Alibaba HK (9988 HK) was off -1.01%. Materials had a strong day as analysts/economists are focusing on increased Chinese infrastructure projects to offset global economic weakness.

China’s National People's Congress will take place during the third week of May in a sign of life returning to some semblance of normality. Mainland financials and real estate followed Hong Kong’s lead higher while staples were off on liquor weakness and health care saw a bout of pre-holiday profit-taking. China’s May PMIs will be released tomorrow with economists expecting a continued rebound.

Following in the footsteps of Alibaba, JD.com (JD US) filed for a Hong Kong listing. The company will issue 5% more shares that could raise between $2B to $3.4B based on different sources. Why relist in HK? US investors don’t properly value Chinese internet companies so they are going to a geographic area where they don’t need to explain themselves. Furthermore, there is the possibility that the companies relisting will be added to Southbound Connect, allowing investors from Mainland China, who are certainly familiar with them, to buy shares for the first time. Another factor is the rise of high-frequency trading. What did BABA have to do with the trade war? Throughout 2019, BABA shares fell after every trade tweet due to algorithms being programmed to sell the Chinese stocks. (Michael Lewis’ book Flash Boys speaks to high-frequency trading though Lewis’ Against the Rules podcast provides a shorter explanation.) Compared to US internet companies, Chinese companies are at a valuation discount. After the Luckin fraud debacle, these companies may garner more scrutiny from US regulators. Ultimately, the US and China need more communication, not less. Collaborating on the prosecution of Luckin would be a great place to work together.

There are rumors that Chinese e-commerce companies will be hosting Golden Week sales events. I haven’t been able to gauge whether these sales will compare to Singles Day given speculation of pent up consumer demand post-quarantine. I’ll do some work and report back.

Yum China (YUMC US) reported earnings after the US close yesterday. Q1 revenue fell -24% year over year to $1.75B while Diluted EPS -72%. The company also temporarily cut its dividend and stock buyback program. The company plans to open 800 to 850 new restaurants in the remainder of 2020.

Starbucks (SBUX US) reported Q1 earnings after the US close yesterday as well. While Starbucks (SBUX US) will open 500 new stores this year in China, revenue dropped -50% in the quarter. However, declines are expected to moderate over the next several quarters with store sales declining between -25% to -35% in Q3 and -10% to flat in Q4.

Caterpillar (CAT US) also reported earnings yesterday. Asia/Pacific sales were off in resource industries -29%, construction -31% and financial products -3% in Q1 2020 versus Q1 2019, which the company primarily attributed to a slowdown in China. The company was optimistic that the worst is over for China’s declines.

H-Share Update

The Hang Seng opened higher though eased over the trading day ending +0.28%/+67 index points to close at 24,643. Volumes were flat day over day and below the 1-year average while breadth was mixed with 28 advancers and 20 decliners. Index heavyweights led the way with China Construction Bank +1.12%/+23 index points, Ping An Insurance +1.14%/+16 index points and HSBC +0.75%/+14 index points. Wharf Real Estate was the day’s largest gainer +2.66%/+2 index points with Geely Auto right behind it +2.02%/+4 index points. Pork processor WH Group -4.59%/-9 index points followed by Want Want China Holdings -3.97%/-3 index points. China-domiciled companies listed in Hong Kong outperformed Hong Kong-domiciled companies +0.57% versus +0.12% using the HS China Enterprise and HS HK 35 indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.49% led higher by materials +2.04%, discretionary +2%, real estate +1.55%, energy +1.34%, industrials +0.98%, financials +0.95% and utilities +0.55%. Staples were off -1.51%, health care -0.98% , tech -0.41% and communication -0.14%. Southbound Connect was closed today.

A-Share Update

Shanghai and Shenzhen had a lackluster session trading in a narrow range +0.44% and -0.1% on volumes off -20% from yesterday and below the 1-year average. Large caps outperformed mid and small caps though sector performance was the biggest driver of gains. The Mainland stocks within the MSCI China All Shares Index +0.37% led higher by real estate +2.29%, financials +1.9%, communication +1.5%, discretionary +0.85%, materials +0.54%, energy +0.46%, industrials +0.43%, utilities +0.16% and tech flat. Healthcare and staples were off -1.14% and -1.45%. Northbound Connect trading was closed today.

Last Night’s Prices & Yields

- Yield on 1-Day Government Bond 0.71% versus 0.62% yesterday

- Yield on 10-Year Government Bond 2.50% versus 2.53% yesterday

- Yield on 10-Year China Development Bank Bond 2.79% versus 2.81% yesterday

- CNY/USD 7.08 versus 7.08 yesterday

- CNY/EUR 7.68 versus 7.67 yesterday

- Commodities on the Shanghai & Dalian Exchanges were mixed with Dr. Copper +0.64%