April PMIs Mixed As Export Activity Falls

4 Min. Read Time

April Manufacturing PMI

50.8 versus estimate 51 and March’s 52

April Non-Manufacturing PMI

53.2 versus estimate 52.5 and March’s 52.3

April Caixin China PMI Manufacturing

49.4 versus estimate 50.5 and March’s 50.1

The “official” Purchasing Managers Indexes (PMI) released by the National Bureau of Statistics involves a survey of large companies and many SOEs. The Caixin PMI, which is calculated by IHS Markit, is narrower survey of smaller companies. The PMIs gauge month over month activity. The PMIs are diffusion indices that use 50 as a baseline meaning above 50 shows growth and under 50 contraction. For both manufacturing PMIs, the culprit was export weakness as the global quarantine hits the global economy. Very simply, the demand for the stuff China makes is slowing. While exports make up around 18% of China’s GDP, many are surprised that this work is mainly done by private companies that are not affiliated with the government. Unemployment in manufacturing increased as new export orders fell. While China’s old economic engine of export-driven manufacturing slowed due to plunging external demand, the pickup in the non-manufacturing PMI was primarily driven by a strong pickup in construction activity. Caixin’s Services PMI will be released next Wednesday.

Key News

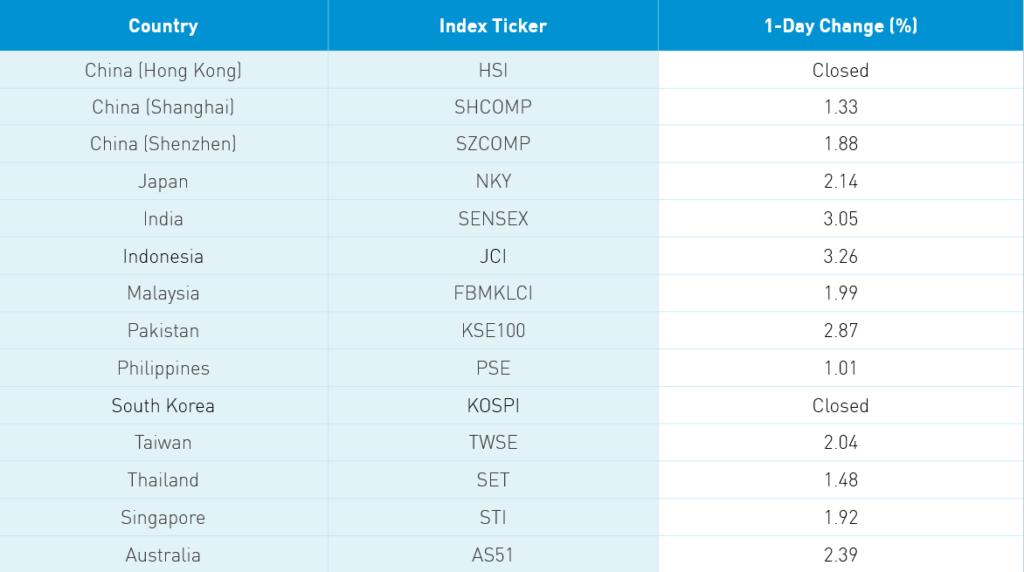

I hope Hong Kongers and South Koreans enjoyed their well-deserved holiday. Unfortunately, they missed out on a strong day across Asian equities, largely driven by promising news of Gilead’s drug results. Mainland China had a strong day led by tech after positive results overnight from Facebook, Qualcomm and Microsoft. Our institutional brokers predominantly work out of HK so unfortunately I didn’t receive a lot of color on today’s market action. I did notice that Huawei sold more processors for smart phones than Qualcomm for the first time ever in April, according to a Mainland media source. Increased talk of economic decoupling would be a significant policy mistake considering how fragile the global economy is at the moment. The unintended consequences for US firms, consumers and inflation are grossly underestimated. The strong performance of materials, industrials and the broad market indicate investors believe the weakening Manufacturing PMIs will lead to further stimulus.

China’s main policy meeting, the “Two Sessions”, will take place in mid-May. China’s policymakers, who have significant dry powder as they’ve not cut the broad interest rate, can expand the budget deficit further, allow for more bond issuance to support economic activity and implement consumption support. Leading sectors staples and healthcare were off on the day as investors pocketed some vacation spending cash. The coming holiday is apt to see a significant uptick in domestic travel. The only market in Asia open tomorrow is Australia though we’ll publish our weekly review.

A major media outlet had a piece on a mainland China fund manager who is bearish on the market so her whole fund is in cash. Guess how much money the manager runs? $28 million. It must have been hard work finding a manager who is bearish! Looking at equity ETFs listed in China they have seen $8.8 billion of inflow year to date. Not going to read about the latter other than here.

MSCI’s Semi-Annual Index Rebalance (SAIR) is on the horizon. The review requires passive managers benchmarked to MSCI indexes to rebalance their ETFs and index funds. Based on the vast outperformance of China versus other Emerging Market countries, I would expect more Chinese companies to enter the index. This is not due to MSCI’s dedicated inclusion of Chinese A-shares, but rather their free-float market cap screen will “capture” more Chinese companies since they are larger and other countries’ stocks are smaller. China today already represents 40% of the MSCI Emerging Markets Index, accounting for 704 of 1404 stocks, while the #2 country South Korea accounts for 110 stocks with a 12% weight. How many more names? One early broker estimate was several dozen. We won’t know until May 12th when the MSCI’S pro forma is released, which will then be implemented at the market’s close on May 29th.

I’m reading an interesting book called Factfullness by Hans Rosling, which explores misperceptions about the world today and the vast improvements in the quality of life in the world over the last several decades. It examines life spans, child mortality, income, etc, which have all improved dramatically even if the vast majority of us don’t realize it. The author runs a website called gapminder.org that has several interesting tools. According to the website’s GDP per capita section, China has risen from $1,000 to $16,000 from 1980 to 2019. China’s WTO inclusion is cited as a seismic change for China though a strong upward trend had already been in place twenty years prior. What drove it? We believe urbanization, which has risen from 20% to nearly 60%. What comes with living in a city? Proper housing and access to education, services, and health care. If you need something optimistic to read Factfullness is a great read.

Hong Kong - Closed

A-Share Update

Shanghai & Shenzhen jumped higher and grinded higher all day to close +1.33% and +1.88%, respectively, as volumes popped +27% from yesterday and were above the 1-year average. Breadth was very strong with 3,109 advancers and 83 decliners as mid and small caps outperformed large caps. The Mainland stocks within the MSCI China All Shares Index gained +1.65% led higher by tech +5.32%, discretionary +3.04%, industrials +2.6%, materials +2.35%, communication +1.62%, financials +1.24%, energy +1.22%, utilities +0.52% and real estate +0.14%, while staples and health care were off -0.16% and -0.59%. Northbound Connect was closed today.

Last Night's Prices & Yields

- CNY/USD 7.06 versus 7.08 yesterday

- CNY/EUR 7.69 versus 7.68 yesterday

- Yield on 1-Day Government Bond 0.88 versus 0.71 yesterday

- Yield on 10-Year Government Bond 2.54 versus 2.50 yesterday

- Yield on 10-Year China Development Bank Bond 2.82% versus 2.79% yesterday