Muted Market Reaction To Mixed Economic Data

3 Min. Read Time

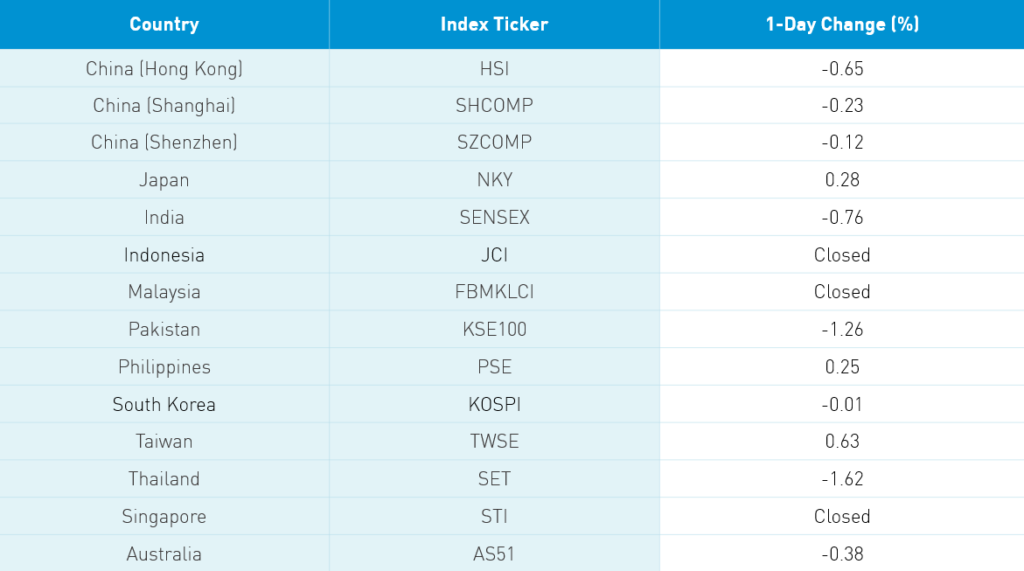

Key News

Caixin China PMI Services

44.4 versus estimate 50.1 and March’s 43

April Trade Data in CNY Year over Year

| Exports | -14.1% versus estimate -14.1% and March’s -3.5% |

| Imports | -12.2% versus estimate -12.2% and March’s +2.4% |

| Trade Balance | 39.5B versus estimate 39.5B and March’s 139B |

April Trade Data In US $ Year over Year

| Exports | -11% versus estimate -11% and March’s -6.6% |

| Imports | -10% versus estimate -10% and March’s -0.9% |

| Trade Balance | $8.68B versus estimate $8.6B and March’s $19.9B |

| Foreign Reserves | $3.056 trillion versus estimate $3.056 trillion and March’s $3.060 trillion |

Asian equities took a breather after yesterday’s strong move in lackluster trading. China’s trade data came in better than expected though the Services PMI was weak. The trade data is likely to get worse as global quarantines sap demand for China’s exports while imports will likely slip as global production is constrained. The Caixin Services PMI focuses on smaller companies, which generate 60% of China’s GDP and account for 80% of employment. The Services PMI is a very small sample, which makes it more volatile and diminishes its relevance to some degree. Real-time data providers generate huge amounts of data that have made government data releases less relevant. Want to know the status of industrial production? Use a satellite to check pollution. Want to know if factories are running? Track cell phones going into the factories. We had noted the uptick in China returning to work by using mobile phone GPS showing people sitting in traffic. Ultimately, policymakers will use the data to engineer stimulus measures for the economy as the “Two Session” policy meetings begin May 21st and May 22nd. One broker noted the positive performance around these meetings, which hopefully occurs this year.

It was quiet on individual stock moves less Budweiser Brewing Co APAC (1876 HK, I love this ticker as derived from the founding of Budweiser) -2.53%, which reported disappointing results pre-market. Top volume leaders were off in lackluster trading Tencent -0.68%, Alibaba -1.6%, and Semiconductor Manufacturing +0.24 after a massive gain yesterday. Mainland China also had a fairly lackluster day as investors weighed the mediocre trade data and potential for more stimulus.

H-Share Update

The Hang Seng traded in a narrow range in a lackluster day of trading to close -0.65%/-156 index points on light volumes off -21% from yesterday. Breath was atrocious with only 7 advancers and 41 decliners led lower by today’s worst performer Hong Kong Exchange & Clearing -2.76%/-24 index points, Tencent -0.68%/-18 index points, and China Construction Bank -0.82%/-16 index points. Today’s best performer was CSPC Pharmaceutical +2.11%/+4 index points. Following Hong Kong Exchanges, China Overseas land -2.66%/-7 index points, Swire Pacific -2.11%/-1.5 index points and CK infrastructure -2.05%/-2.2 index points.

China-domiciled companies outperformed Hong Kong-domiciled companies -0.44% versus -0.86% using the HS China Enterprise and HS HK 35 indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index eased -0.34% led lower by communication -0.71%, staples -0.59%, energy -0.57%, real estate -0.5% utilities -0.46%, discretionary -0.44%, financials -0.37%, tech -0.09% industrials -0.08%. Healthcare and materials managed gains of +1.63% and +0.63%. Southbound Connect volumes were light and lower from yesterday in mixed trading. Volume leader Semiconductor Manufacturing saw buying volume outpace seller volume by a small margin, Tencent was sold nearly 3 to 1 and Hong Kong Exchange was heavily sold. Mainland investors bought $150mm worth of Hong Kong stocks today as Southbound Connect turnover accounted for 10% of Hong Kong’s trading.

A-Share Update

The Shanghai & Shenzhen traded in a tight range all day closing -0.23% and -0.12% on volumes that were down -7% from yesterday. Breadth was off with 1,312 advancers and 2,225 decliners with large, mid and small caps all lower. The Mainland Chinse companies within the MSCI China All Shares Index were off -0.1% with staples, communication, healthcare and materials managing gains of +1.18%, +0.62% and +0.57% and +0.16%, respectively. On the downside were discretionary -0.09%, financials -0.49%, industrials -0.54%, utilities -0.61%, tech -0.81%, energy -0.85% and real estate -0.94%. Northbound Connect volumes were moderately high in mixed trading. Volume leader Kweichow Moutai was flat, Inner Mongolia Yili Industrial was sold 3 to 2 and Ping An insurance sold slightly. Foreign investors sold $444mm worth of Mainland stocks today as Northbound Connect accounted for just over 5% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 7.09 versus 7.10 yesterday

- CNY/EUR 7.64 versus 7.68 yesterday

- Yield on 1-Day Government Bond 0.88% versus 0.88% yesterday

- Yield on 10-Year Government Bond 2.63% versus 2.58% yesterday

- Yield on 10-Year China Development Bank Bond 2.96% versus 2.88% yesterday