The White Horses Stampede, Week In Review

4 Min. Read Time

We will be hosting a webinar on the reopening of China's economy and investing after COVID-19 on Thursday, May 14th at 8:30 am EST.

Please click here to sign up!

Week In Review

- Asian equities traded lower on Monday upon fresh tariff threats coming out of the White House, but Mainland Chinese markets were closed. Also, it was announced that China’s first-ever publicly-traded REITs will be launched to fund infrastructure upgrades.

- While markets remained closed on the Mainland on Tuesday, Hong Kong saw a healthy rebound as bargain hunters flocked to the market to sweep up discounted equities. We also found out that Netease will pursue a secondary listing in Hong Kong and gaming giant Kingsoft will spin off its could computing business Kingsoft Cloud by pursuing an IPO in the US.

- Although they were expected to fall, Mainland markets rose on Wednesday upon opening from market holidays on Monday and Tuesday. Semiconductor Manufacturing (981 HK) lead gains upon news that the company would list shares on the STAR board as well as expectations for tech companies in China to source domestically due to trade rhetoric.

- Multiple economic releases spurred a slight downturn in Mainland markets on Thursday. The mixed releases included the April Caixin Services PMI, which was unexpectedly weak at 44.4, as well as import/export growth, which was also weak but well within expectations.

Friday's Key News

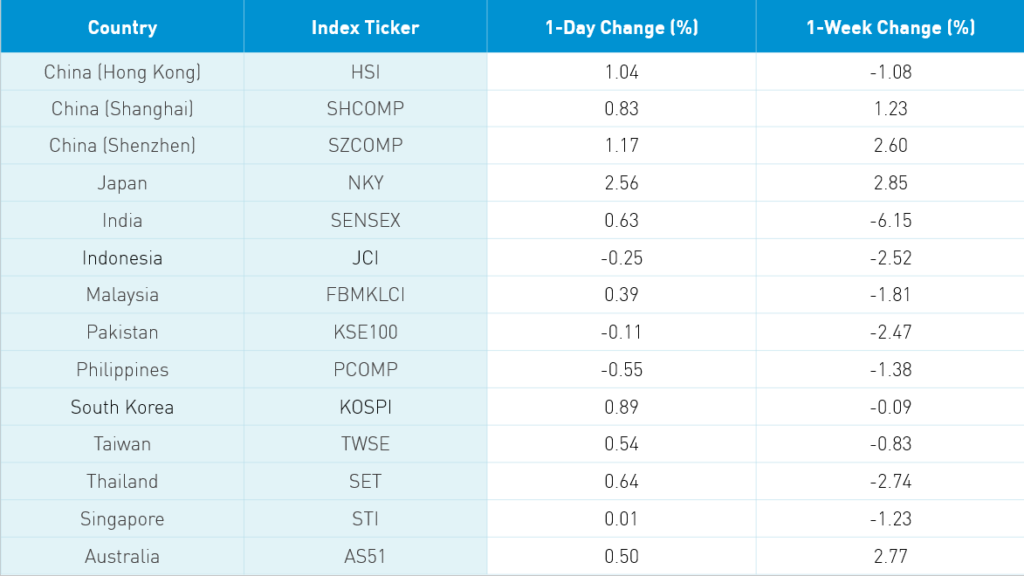

Asian equities ended the holiday-shortened week on a high note. Monday’s plunge feels like a century ago. Without question, the US-China trade conference call helped on sentiment as Mnuchin and Liu He agreed that both countries are making good progress on fulfilling commitments under the phase one deal signed in January.

Hong Kong had a strong day led higher Tencent +2.7%, mobile phone maker Xiaomi +8.11% as their stores reopened and customers bought 5G hand-over-fist, and Alibaba +1.52% on chatter their Labor Day holiday sale promotion was a success. Hong Kong Exchanges fell -1.46% after the legendary CEO Charles Li announced his retirement. Budweiser Brewing rebounded +5.42% after yesterday’s plunge and Macau casino operators also had a nice rebound.

Autos rose on news that China’s auto sales increased year over year for the first time in 21 months. Curb your enthusiasm as car sales rose a “whopping” +0.9% year over year. However, electric vehicle maker BYD fell -1.47% after reporting a decline in sales.

We had mentioned China Literature replaced its CEO with a Tencent executive. The company’s stock rose another +7.78% today. Meituan Dianping also had a strong day gaining +3.62%.

Mainland China ended the holiday-shortened week on a high note as the white horses, a term for appliance and liquor stocks, led the market higher. Today’s highest volume stock Gree Electric Appliances +5.34% while Kweichow Moutai +0.2%.

Back in the yonder year when I would walk barefoot in the snow to school there was a program through which foreigners could access Mainland Chinese equities called QFII. However, repatriation rules, rules about getting your money out of China, always posed a problem for foreign investors making use of the scheme. Finally, it has been announced that rules to pull money out of China have been eliminated in order to facilitate foreign investing in the Mainland. While a nice gesture, the most effective way to increase foreign investment is to address the issues upon which MSCI has made continuing their A-share inclusion contingent. The three main issues are 1) coordinating Hong Kong and Mainland holiday schedules 2) listing of MSCI China A Index futures 3) Mainland Chinese equity trades settle T+0 which means when I buy a stock I have to deliver the cash today versus T+2, in which I deliver the cash trade date plus two days. Addressing these issues as well makes a world of sense to me.

H-Share Update

The Hang Seng grinded higher to close +1.04%/+249 index points at 24,230 on volume that rose +12% from yesterday, which is slightly above the 1-year average. Breadth was strong with 44 advancers and just 5 decliners as index heavyweights led the way higher including Tencent +2.7%/75 index points, HSBC +1.8%/+35 index points and China Construction Bank +1.32%/+26 index points. Today’s best performer was Macau casino operator Galaxy Entertainment +5.09%/+17.9 index points while Hong Kong Exchanges was the worst performer -1.46%/-12.8 index points on news legendary CEO Charles Li will retire. China-domiciled companies outperformed Hong Kong-domiciled companies by a small margin +1.07% versus 1% using the HS China Enterprise and HS HK 35 indexes as proxies. The Hong Kong stocks within the MSCI China All Shares Index gained +1.72% led higher by tech +3.36%, discretionary 2.83%, communication +2.23%, materials +1.98%, real estate +1.92%, industrials +1.45%, health care +1.36%, energy +1.3%, financials +1.05%, staples +1.05% and utilities +0.-02%. Southbound Connect volumes were moderate in mixed trading as volume leader Tencent was sold 6 to 1, Xiaomi was bought 4 to 3 and Hong Kong Exchanges was sold 6 to 1. Mainland investors bought $54mm worth of Hong Kong listed stocks today as Southbound Connect trading accounted for nearly 11% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen ended a short but good week +0.83% and +1.17% on moderate volumes that were above the 1-year average. Breath was strong with 2,823 advancers and 791 decliners as mid and small caps outperformed large caps by a small margin. The Mainland stocks within the MSCI China All Shares Index gained +1.16% led higher by discretionary +2.22%, real estate +1.49%, tech +1.45%, financials +1.38%, materials +1.24%, energy +0.96%, communication +0.9%, healthcare +0.88%, industrials +0.86%, staples +0.73% and utilities +0.55%. Northbound Connect volume was strong. Shenzhen Connect had stronger volume and buying activity than Shanghai Connect. Foreign investors bought $687mm worth of Mainland stocks today as Northbound Connect accounted for just over 5% of mainland turnover. For the week, foreign investors bought a total of $403mm worth of Mainland stocks.

Last Night’s Prices & Yields

- CNY/USD 7.06 versus 7.08 yesterday

- CNY/EUR 7.65 versus 7.64 yesterday

- Yield on 1-Day Government Bond 0.88% versus 0.88% yesterday

- Yield on 10-Year Government Bond 2.62% versus 2.63% yesterday

- Yield on 10-Year China Development Bank Bond 2.95% versus 2.96% yesterday