Week In Review, Hang Seng Drops Alibaba Bombshell, JD.com Earnings Beat Raised Expectations

4 Min. Read Time

Yesterday we hosted a webninar on the reopening of China's economy and investing after COVID-19.

Please click here to view the replay!

Week In Review

- Hong Kong listed equities rallied on Monday in anticipation of Tencent’s earnings release on Wednesday as well as ADR earnings to come. Meanwhile, South Korea’s coronavirus flare-up, which originated in a nightlife district that had recently opened up, weighed on sentiment in the country.

- Asian equities were largely lower in Tuesday trading on increased US-China political rhetoric. Political appointee board members of the Federal Thrift Savings Plan, which manages US federal workers’ pension funds, decided to delay an index switch that would have resulted in an allocation to Chinese equities. We believe it is unfortunate that America’s federal employees may miss out on an excellent investment opportunity.

- Tencent announced impressive Q1 2020 results on Wednesday. According to the release, quarterly revenues, powered by increased gaming activity during quarantines, increased to RMB 108 billion compared to an estimated RMB 101 billion. MSCI also announced that China’s weight in its Emerging Markets Index would rise by 1% from 40.6% to 41.6% this year.

- A grim outlook proffered by US Fed Chair Powell caused Asian equities to follow Wall Street lower on Thursday.

Friday's Key News

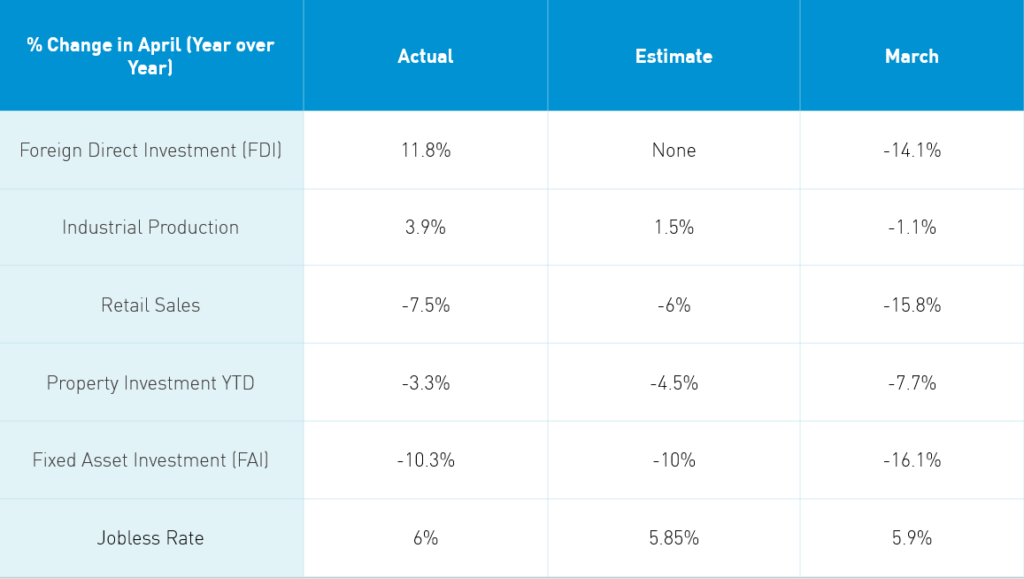

Asian equities were mixed overnight following modest gains on Wall Street. Mainland China saw a series of encouraging economic releases on the supply side while retail sales were low in April. Mainland markets were mixed while Hong Kong ended the session lower as investors became concerned over April retail sales and also await a final decision from the PBOC on a rate cut.

After the close in Hong Kong, Hang Seng announced that the Hang Seng Index and Hang Seng China Enterprise constituents would not change. That noise in the background was my jaw hitting the ground. Alibaba’s Hong Kong listing (9988 HK) will not be added, which means we still do not know whether the stock will be included in Southbound Connect. I am literally speechless. The announcement was supposed to be Monday after the close in Hong Kong. I suppose the index provider hopes people that people will forget over the weekend. The passive inflow being added would be nice but the real goal of listing in Hong Kong was Southbound Connect. The news will be devastating for Hong Kong Exchanges due to the lost trading volume. HK Exchanges (388 HK) had been up +1.12% on Friday though I expect the stock will plummet on Monday. Fortunately, there is still hope for Meituan Dianping to be included in the benchmark.

Takeaway: Industrial production was surprisingly strong while retail sales was somewhat soft. However, it is important to recognize that online sales grew, just not enough to tip the scale overall. I was surprised that property investment and FAI came in soft, but at least they were above estimates. Overall, we know that an element of China’s economy is effected by the global economic slowdown. The 10am release led to rally as the market’s view is more policy support will be coming.

JD.com reported Q1 results before the US market open. JD had audaciously raised its Q1 revenue forecast during its Q4 results, which came in the thick of China’s quarantine. JD met and beat its raised expectations.

- Revenues +20.7% to $20.6 billion (RMB 146.2B)

- Revenues from general merchandise products +38.2% to $7.4B (RMB 52.5B)

- Income from Operations $0.3B (RMB 1.2B

- Diluted EPS $0.10 (RMB 0.72

- Non GAAP Diluted EPS $0.28 (RMB 1.98B)

- Active customer accounts +24.8% to 387mm

H-Share Update

The Hang Seng bounced around the room to close -0.14%/-32 index points to close the at 23,797 on volumes -12% from yesterday though above the 1 year average. Breadth was off with 22 advancers and 27 decliners led by Tencent -2.18%/-61 index points, AIA +1.64%/+39 index points and Hong Kong Exchanges +1.12%/+10 index points. Apple suppliers were the best performers AAC Tech +6.49%/+5 index points and Sunny Optical +3.2%/+8 index points while pork producer WH Group was the day’s worst -4.49%/-8 index points. HK and Chinese domiciled stocks were inline +0.08% and -0.13% using the HS HK 35 index points and HS China Enterprise as proxies. The Chinese companies listed in HK within were off -0.31% with tech +1.85%, health care +1.74%, utilities +1.06% and materials +0.68%. One the downside financials -0.04%, real estate -0.05%, discretionary -0.09%, energy -0.1%, industrials -0.16%, staples -0.59% an communication -1.64%. Southbound Connect were light/moderate with mainland investors net buyers of HK stocks. Volume leader Semiconductor Manufacturing was sold slightly. Mainland investors bought $268mm of HK stocks today as Southbound Connect trading accounted for just over 8% of HK turnover.

A-Share Update

Shanghai & Shenzhen chopped around to close -0.07% and +0.16% as volume picked up +2% from yesterday which is just above the 1 year average. Breadth was decent with 2,049 advancers 1,521 decliners as mid and small caps outperformed large caps. The mainland stocks within the MSCI China All Shares were off -0.17% as tech +1.15%, communication +0.14% and industrials +0.09%. Real estate was off -0.05%, utilities -0.06%, materials -0.13%, energy -0.17%, financials -0.18%, discretionary -0.64%, staples -0.85% and health care -1.14%. Northbound Stock Connect volumes were light/moderate though foreign investors were buyers of mainland stocks. Volume leaders Gree Electric Appliances and Kweichow Moutai saw modest buying. Foreign investors bought $168mm today as Northbound Connect turnover accounted for less than 5% of Hong Kong’s turnover. For the week, foreign investors bought $574mm worth of Hong Kong stocks.

Last Night’s Prices & Yields

- CNY/EUR 7.68 versus 7.67 yesterday

- CNY/USD 7.10 versus 7.10 yesterday

- Yield on 1-Day Government Bond 0.68% versus 0.70% yesterday

- Yield on 10-Year Government Bond 2.68% versus 2.70% yesterday

- Yield on 10-Year China Development Bank Bond 2.97% versus 3.00% yesterday