ADR Earnings Parade: Baidu Beats, Bilibili Gets Jiggy With It, Sina Beats Estimates on Lower Costs

5 Min. Read Time

Last week we hosted a webninar on the reopening of China's economy and investing after COVID-19.

Please click here to view the replay!

Key News

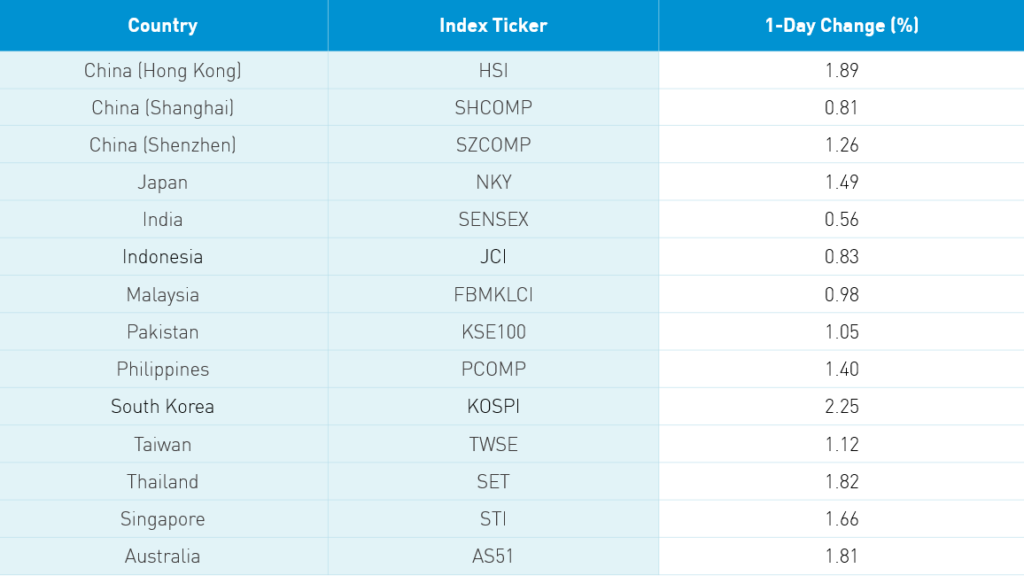

Asian equities ripped on vaccine optimism as travel, airlines, casinos, and leisure names all rebounded strongly. Alibaba HK (9988 HK) +3.35% unseated Tencent (700 HK) +1.65% as the top performer on news Hang Seng Indexes would allow dual-listed and weighted voting rights companies in their August Hang Seng Index rebalance. Meituan Dianping (3690 HK) jumped +3.2% as it too might be added to the widely followed index. Xiaomi (1810 HK) also popped on the news +5.15% along with Hong Kong Exchanges (388 HK) +4.08%.

Semiconductor Manufacturing (981 HK) ripped +7.58% after the US decision to limit Taiwan Semiconductor from selling chips to Huawei. Tech stocks had a strong day on the Mainland as the decision to cut Huawei off means it has to get chips elsewhere. I’ve been a little surprised by the muted reaction among US semiconductor stocks considering that they are losing one of their biggest customers.

Reuters reported that Nasdaq will be tightening listing standards for foreign companies. The move is fairly symbolic as it would prevent companies raising less than $25mm from listing on the exchange, which would have affected only 40 of the 225 Nasdaq China listings. Small-cap companies globally have lower listing requirements because they have trouble accessing capital. I’m all for the move though some of these companies may list in Hong Kong or the Mainland going forward. One Hong Kong broker noted JD.com is holding a meeting next week to discuss a Hong Kong listing.

The WSJ had a good article on US companies doing well in China. Despite escalating US-China political rhetoric, US companies continue to capitalize on China’s growing urban middle class. The article speaks to the strong brand recognition of US firms such as Walmart, Tesla, McDonald's and Popeyes. The WSJ may be catching onto the consequence of political rhetoric on US companies. The choice of a Walmart store photo was likely done on purpose considering that a certain Arkansas senator has been vehemently anti-China. However, a glaring omission from the article was the reality that China is the third-largest destination for US exports behind Canada and Mexico.

Yesterday I noticed that Singapore’s non-oil exports unexpectedly rose +9.7% in April versus analysts’ estimate of -5%. What drove the rebound? Pharmaceutical exports jumped +174%. 3M has a large mask factory in Singapore.

Bytedance is known for its popular TikTok short video social media platform. The company announced that Disney veteran Kevin Mayer, who ran the Disney+ online streaming service, will become TikTok’s CEO. Though passed over for taking over Disney’s reins following Bob Iger’s retirement announcement, it is quite the coup for TikTok. Hiring a Western executive makes me wonder about an IPO. TikTok has received scrutiny for its Chinese ownership of late. Segregating the non-China business through a US IPO might be feasible.

Baidu reported Q1 results after the US market close yesterday. The results look outstanding to me as the firm beat lowered expectations and cut costs to mitigate quarantine’s effect on revenue.

- Q1 Revenues declined -7% year over year to $3.185 billion (RMB 22.545B) versus estimate RMB 21.929B.

- Adjusted Operating Income +258% to $203mm (RMB 1.437B)

- Adjusted Net Income +219% to $435mm (RMB 3.5082B)

- Adjusted EPS $1.25 (RMB 8.84) versus estimate

- Q2 Revenue forecast RMB 25B to 27.3B versus estimate RMB 25.61B

- Approved a $1B share buyback

- Baidu App averaged 222mm daily users in March +28% YoY

Baidu spin-off and online entertainment company iQIYI reported Q1 results after the US close. There was clearly demand for the company’s content during the quarantine though advertising revenue was off. Costs also increased, which hurt the bottom line.

- Q1 Revenues +9% YoY to $1.1B (RMB 7.6B)

- Membership services revenue +35% to $654mm du to “increased entrainment demand during the Lunar New Year holiday and the COVID-19 pandemic.”

- Online advertising services revenue was $217mm -27% YoY “…due to the challenging macroeconomic environment in China related to the DOVID-19 pandemic.”

- Cost of revenues +9% YoY to $1.1B

- Selling, general administrative expenses +15% to $185mm

- Net loss $406mm (RMB 2.9B) from 1.8B YoY

- Paying subscribing members +23% to 118.9mm YoY

- Q2 Revenue forecast $1.02B to $1.08B, +2% to +8%

Last but not least was online entertainment company Bilibili (BILI), which reported strong Q1 revenue growth and user growth but net income was lower on rising costs. If there is one company that I am least able to properly describe is BILI. It allows users to upload anime/cartoon videos of themselves, online gaming, and watching others play video games. BILI likely gets a bit of a pass as the firm is still in the high growth stage. Sony Corporation of America took a 4.98% or $400mm stake in the company on April 8th. With the ink barely dry, the benefits of leveraging Sony have yet to be implemented. The company’s Q3 forecast was very positive.

- Revenue +69% to $327mm (RMB 2.315B)

- Average monthly active users +70% YoY to 172mm while mobile users +77% to 156mm

- Average paying monthly users +134% to 13.4mm

- Total operating expenses +117% to $151mm (RMB 1.074B).

- Net loss was $76mm (RMB 538mm)

- Adjusted EPS loss was ($0.20)

- Q2 revenue forecast is between RMB 2.5B and RMB 2.55B

Online news and media outlet Sina reported Q1 results before the US market open. The company was able to beat lowered estimates due to a fall in advertising revenue and cut expenses, leading to a pick up in the bottom line. Impressive! Kudos to management.

- Revenues -8% YoY to $435mm from $475mm YoY

- Advertising revenues -20% to $310mm from $388mm YoY

- Non-advertising revenues +44% to $125mmGross margin declined t o66% from 76% YoY

- Operating expenses declined to $257mm from $272mm

- Net income increased to $82mm from $33mm YoY

- Diluted EPS $1.21 versus $0.46%

Sina spinoff Weibo, often called the Twitter of China, reported Q1 before the US market open today. Like Sina, the company beat lowered estimates though the weaker Q2 forecast could weigh on shares.

- Revenues -19% to $323mm from $399mm.

- Advertising and marketing revenues -19% to $275mm from $341mm

- Monthly average users +85mm to 550mm YoY

- Costs & expenses declined to $265mm from $276mm

- Net income was $52mm versus $150mm YoY

- Diluted net income EPS $023 from $0.66 YoY

- Q2 revenue forecast is a -7% to -12% decline

H-Share Update

The Hang Seng opened higher and stayed there closing +1.89%/+453 index points at 24,388 as volumes surged +15% from yesterday. Breadth was strong with 48 advancers and 2 decliners led by AIA +3.07%/+75 index points, HSBC +3.27%/+63 index and Tencent +1.65%/+47 index points. Today’s best performer was Swire Pacific +4.56%/+3 index points while CK Hutchison -1.96%/-8 index points. Hong Kong-domiciled and China-domiciled stocks did well +1.87% and +1.61%, respectively, using the HS HK 35 and HS China Enterprise indexes as proxies. The Chinese companies within the MSCI China All Shares +1.57% led higher by Tech +4.04%, Discretionary +2.89%, Energy +2.78%, Industrials +2.18%, Utilities +1.94%, Financials +1.71%, Communication +1.3%, Real Estate +1.13%, Staples -0.01%, Materials -0.18%, and Health Care -0.46%.

Southbound Connect volumes were moderate as Mainland investors were net buyers of Hong Kong stocks though trading was choppy. Volume leader Semiconductor Manufacturing saw sellers outpace buyers by a small margin while Ping An Good Doctor was bought 20 to 1 and Meituan Dianping by nearly 5 to 1. Mainland investors bought $157mm worth of Hong Kong stocks as Southbound Connect trading accounted for 8% of Hong Kong turnover.

A-Share Update

The Shanghai & Shenzhen gained +0.81% and +1.26% as volumes slipped -12% from yesterday though still above the 1 year average. Breadth was strong with 2,456 advancers and 1,106 decliners as mid and small caps outperformed large caps. The mainland stocks within the MSCI China All Shares +1.02, led higher by Tech +3.09%, Discretionary +1.59%, Energy +1.43%, Communication +1.16%, Health Care +0.98%, Industrials +0.86%, Financials +0.82%, Materials +0.52%, Staples +0.18%, Utilities +0.01%.

Northbound Connect volumes were moderate as foreign investors were buyers of Mainland stocks. Volume leader Kweichow Moutai saw sellers outpaced buyers 3 to 2 while Gree Electric Appliances saw sellers outpace buyers by a small margin. Foreign investors bought $520mm worth of Mainland stocks today as Northbound Connect trading accounted for nearly 5% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 7.10 versus 7.11 yesterday

- CNY/EUR 7.77 versus 7.73 yesterday

- Yield on 1-Day Government Bond 0.98% versus 0.68% yesterday

- Yield on 10-Year Government Bond 2.73% versus 2.73%

- Yield on 10-Year China Development Bank Bond 3.05% versus 3.03%