NetEase Rides China’s Quarantine Gaming Binge

3 Min. Read Time

Key News

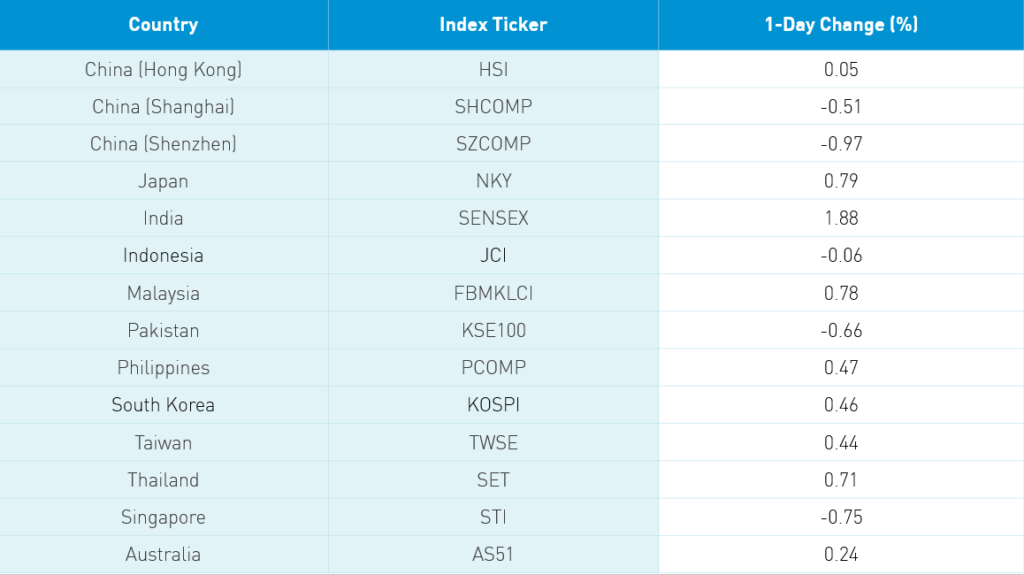

Asian equities ended the session mostly higher despite the fading of hope for Moderna producing a vaccine. Hong Kong managed a small gain on the shoulders of volume leader Tencent’s strong performance +2.33%. Volume leaders were mostly growth names as Tencent was followed by Alibaba HK +0.57% and Xiaomi +1.11% following their earnings release and Meituan Dianping +2.15%. Ping An Healthcare rebounded +5.15% after clarifying the removal of their CEO by their board was for performance reasons. The stock is up +86% year to date, thus accounting for the majority of the 93% return since its May 2018 IPO.

Mainland China saw profit-taking after yesterday’s strong performance. As expected, China’s Loan Prime Rate was left unchanged at 1-year 3.85% and 5-year 4.65%. Unlike in Hong Kong, growth stocks were off on the Mainland including health care. Mainland health care was off after WuXi Apptech announced a sale of shares. Ironically, the Mainland market is anticipating increased policy support for growth sectors as “new infrastructure” has become a buzzword. Healthcare is apt to see increased attention as well.

I noticed an interesting factoid. What is the average prediction by Wall Street economists for China’s GDP in 2021? The number is 8%. I was pleasantly shocked as well. Part of the reason is the low 2020 GDP prediction of only +1.8% from 2019. Year over year, Q2 2020 is expected to be 1.1% which feels low to me though the rebound accelerates to 5% in Q3, 6% in Q4, and a whopping 14.5% in Q1 2021! US GDP is expected to follow a similar path, though not quite as robust on the upside to the upside. Remember that US Q2 GDP won’t be released until July. Economists predict US Q2 GDP will fall -9.6% year over year and -34% quarter over quarter. I certainly hope they are wrong, but we are currently in a recession after all. What I am getting at is that ratcheting up a trade war during a recession seems like pure insanity! It might make for a great sound bite, but the reality is that people vote with their wallets. If the US is to achieve the strong Q3 rebound that is being predicted, tailwinds, not headwinds, are a necessity.

Online gaming company NetEase (NTES US) reported solid results after the US close yesterday. What did kids in China do while in quarantine? They played mobile video games! According to the company, “flagship titles such as the Fantasy Westward Journey series, New Westward Journey Online II, and newer hit titles including Life-After, Onmyoji, and All About Jianghu also maintained their popularity.” Writing that sentence made me feel old and completely out of touch! The results speak for themselves.

- Revenue grew +18.3% YoY to $2.409B (RMB 17.1B) from RMB 14.422B versus analyst estimate RMB 15.65.

- Online gaming revenue increased to RMB 13.518B ($1.909B) from RMB 11.850B YoY and RMB 11.604B quarter over quarter.

- Gross profit increased to $1.324B (RMB 9.377B) from RMB 7.737B YoY and RMB 8.210B QoQ

- Gross profit margin +64.1%, up marginally YoY and QoQ

- Net Income $501.5mm (RMB 3.551B) from RMB 2.732B YoY

- Non-GAAP net income $595mm (RMB 4.219B) up from RMB 3.353B YoY versus analyst estimate RMB 3.96B

- Non GAAP EPS and diluted net income were $4.60 and $4.54

- $1B share repurchase program has been announced after being approved by the board

H-Share Update

The Hang Seng opened higher though quickly sold off just into negative territory most of the day until a slight uptick at the close pushed it to +0.05%/11.8 index points at 24,399. Volumes were off -19% from yesterday though remained above the 1-year average. Breadth was mixed with 22 advancers and 26 decliners as index heavyweight Tencent +2.33%/+68 index points, HSBC -2.53%, and China Mobile -1.84%/-19 index points. AAC rebounded +6.82%/+6 index points as today’s best performer while China Unicom -3.65%/-3 index points. China-domiciled companies outperformed Hong Kong-domiciled companies +0.15% versus -0.32%, using the HS China Enterprise and HS HK 35 Indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.52% with communication +1.71%, health care +1.36%, tech +1.01%, utilities +0.67%, discretionary +06%, staples +0.4% financials +0.06%, materials -0.16%, real estate -0.8%, industrials -1.1%, and energy -1.11%.

Southbound Connect volume was light in mixed trading as volume leader Tencent was sold 3 to 1, Semiconductor Manufacturing bought slightly and China Mobile sold 5 to 1. Mainland investors bought $105mm of Hong Kong stocks today as Southbound Connect trading accounted for nearly 10% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen declined -0.51% and -0.97%, respectively, as volume increased +6% from yesterday on mixed breadth of 1,003 advancers and 2,688 decliners. Large caps “outperformed” i.e. they didn’t fall as much as mid and small caps. The Mainland stocks within the MSCI China All Shares Index declined -0.56% with Financials +0.24%, Utilities +0.13%, Materials -0.11%, Discretionary -0.32%, Industrials -0.53%, Consumer Staples -0.63%, Energy -0.71%, Communication -0.98%, Real Estate -1.04%, Tech -1.37%, Health Care -1.43%.

Northbound Connect volumes were moderate as foreign investors were buyers of Mainland stocks today. Shenzhen volume exceeded Shanghai’s, which has been the trend for quite some time. Volume leader and MSCI China A Inclusion stock Kweichow Moutai saw buyers outpaced sellers by 8 to 5. Meanwhile, Contemporary Amprex Technology saw 2 to 1 buyers. Foreign investors bought $287mm worth of Mainland stocks today, brining the week’s total to $1.286B. Northbound Connect trading accounted for nearly 5% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 7.10 versus 7.10 yesterday

- CNY/EUR 7.79 versus 7.76 yesterday

- Yield on 1-Day Government Bond 0.82% versus 0.98% yesterday

- Yield on 10-Year Government Bond 2.69% versus 2.73% yesterday

- Yield on 10-Year China Development Bank Bond 3.01% versus 3.05% yesterday