VIPS Successfully Navigates China’s Quarantine

4 Min. Read Time

Key News

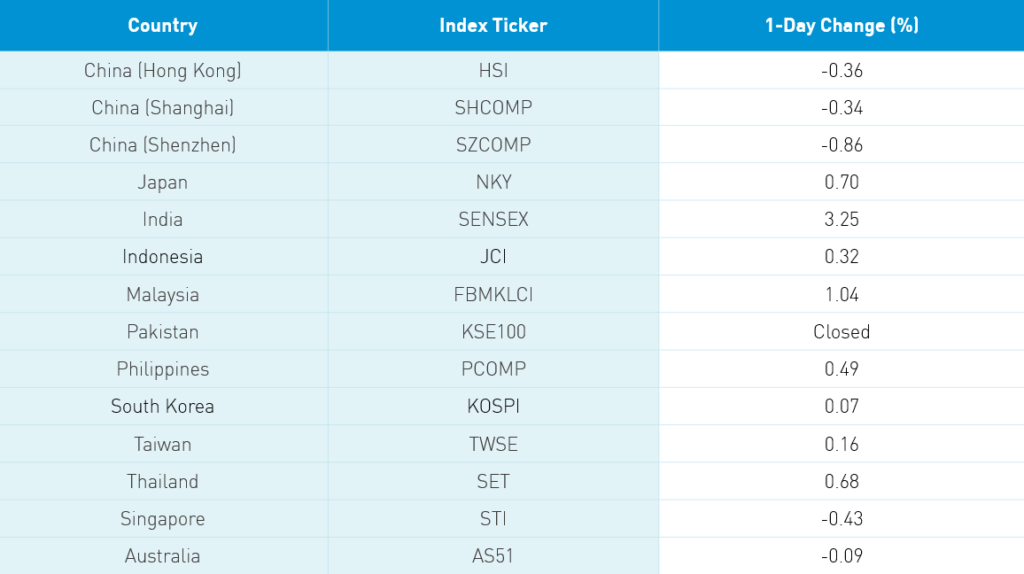

Asian equities had a mixed day as rising US-China political tensions weighed on Hong Kong and the Mainland China. Technology stocks came especially under pressure. Hong Kong’s most heavily traded stocks were the three big growth names Tencent -1.27%, Alibaba HK -1.84% and Meituan Dianping -2.59%. Staples were off in Hong Kong as the passage of China’s new security law could lead to both increased demonstrations and the US voiding Hong Kong’s special export and import rules. Voiding the trade status, which the market believes is unlikely, reminds me of the famous quote from the Vietnam War: “It became necessary to destroy the town to save it”. Hong Kong is a beautiful city, one that I hope to return to in the not so distant future.

CSPC Pharmaceutical jumped +6.68% after announcing revenue growth of +20% YoY and a listing on the STAR Board, a new growth stock board on the Shanghai Stock Exchange. The Mainland market also ended lower with recent leaders such as tech and healthcare selling off. The Mainland market is waiting for Premier Li’s 4pm press conference following the conclusion of the Two Sessions policy meetings. The press conference will provide insights into the economic policies for the next year.

Yesterday I mentioned that MSCI’s Semi-Annual Index Rebalance takes place this Friday. I recommend watching Bilibili (BILI US) at the 4pm close on Friday. The company is being added to MSCI indices for the first time, requiring passive managers of ETFs and index funds to buy the stock. I caution on buying the stock because the passive managers arrange transactions with their brokers. However, I can predict it will trade significantly.

MSCI and Hong Kong Exchanges announced that 37 MSCI indices will become available for futures on the exchange. Absent was the MSCI China A Index, which has lead me to ask: “Where’s the beef?” Futures on A-shares is one of the conditions necessary for MSCI to increase their inclusion factor or weight in MSCI indexes. Presently, only 20% of the potential amount have been added to indexes such as MSCI Emerging Markets, which limits their weight to 4.7% in the index.

China released April Industrial Profits, which declined -4.3% year over year but improved from May’s -34.9%. At the very least, this is a step in the right direction.

Is anyone else feeling the US-China political rhetoric fatigue? I am! With everything happening in the US and globally it is truly shocking how much US political attention is on China. In a bizarre twist, China is finally getting the attention it has always wanted as the world’s second largest economy. I certainly understand the deflection/distraction campaign of pointing the finger over there versus looking in the mirror. I would have hoped for a 9/11 Commission to be formed to properly evaluate what could have been done better and put a game plan in place for the next inevitable pandemic. Unfortunately, it doesn’t appear that is going to happen. It takes two to tango, of course. Empathy and sympathy would go a long way. Most shocking to me is the apparent lack of communication between the two governments. Pick up a phone. Get on plane. Work it out.

MOMO reports before the US market open tomorrow while Trip.com (formerly C-Trip.com) reports after the US close.

Huawei’s CFO finds out if she will be extradited from Canada to the US today.

Discount online retailer Vipshop (VIPS US) released Q1 results before the US market open this morning. The results were off year over year due to the pandemic though management did a good job keeping the company profitable by cutting expenses.

- Revenue declined to $2.537B (RMB 17.964B) from RMB 20.459B YoY though above estimates of RMB 7.837B

- Gross profit was also off to $510mm (RMB 3.617B) from RMB 4.356B

- Total operating expenses fell to $421mm (RMB 2.983B) from RMB 3.594B

- Net income declined to $96mm (RMB 680mm) from RMB 876

- Non-GAAP net income +20% to $139mm (RMB 986mm) from RMB 816mm

- Diluted EPS $0.14 (RMB 1) from RMB 1.27

- Q2 forecast was for 0% to 5% revenue increase

H-Share Update

The Hang Seng’s early gain quickly evaporated as the index chopped its way to close -0.36%/-83 index points at 23,301. Volumes were up +3% from yesterday, which is just above the 1-year average. Breadth was off with 17 advancers and 32 decliners led by Tencent -1.27%/-35 index points, HSBC +1.22%/+22 index points and today’s best performer CSPC Pharmaceutical +6.68%/+16 index points. CK Infrastructure was the day’s worst performer -3.26%/-3 index points. China-domiciled companies outperformed Hong Kong-domiciled companies by a small margin -0.29% versus -0.61% using the HS China Enterprise and HS HK 35 indices as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index fell -0.75%. In sector moves, energy +0.56%, financials +0.11%, industrials -0.15%, utilities -0.24%, materials -0.74%, healthcare -0.93%, communication -1.09%, real estate -1.24%, discretionary -1.74%, tech -1.75%, and staples -2.27%.

Southbound Connect volumes were moderate to light in mixed trading. Volume leader Tencent was bought by a small margin while Meituan Dianping was sold 3 to 1.

A-Share Update

Shanghai & Shenzhen opened lower and stayed there to close -0.34% and -0.86% as volume picked up 8.5% from yesterday though remained below the 1-year average. Breadth was mixed with 1,478 advancers and 2,174 decliners as small and mid caps underperformed large caps. The mainland stocks within the MSCI China All Shares Index were off -1.13%. In sector moves, discretionary +0.05, real estate -0.12%, financials -0.32%, energy, -0.33%utilities, -0.35%, industrials -0.75%, communication -0.97%, materials -0.97%, staples -1.48%, healthcare -2.37%, tech -2.51%.

Northbound Connect volumes were light to moderate as foreign investors were buyers of Mainland stocks. Volume leader Kweichow Moutai had sellers outpace buyers by a small margin while Jiangsu Hengrui Medicine was also sold by a small margin. Foreign investors bought $180mm worth of Mainland stocks today.

Last Night’s Prices & Yields

- CNY/USD 7.17 versus 7.14 yesterday

- CNY/EUR 7.88 versus 7.83 yesterday

- Yield on 1-Day Government Bond 1.36% versus 1.21% yesterday

- Yield on 10-Year Government Bond 2.75% versus 2.74% yesterday

- Yield on 10-Year China Development Bank Bond 3.04% versus 3.04% yesterday