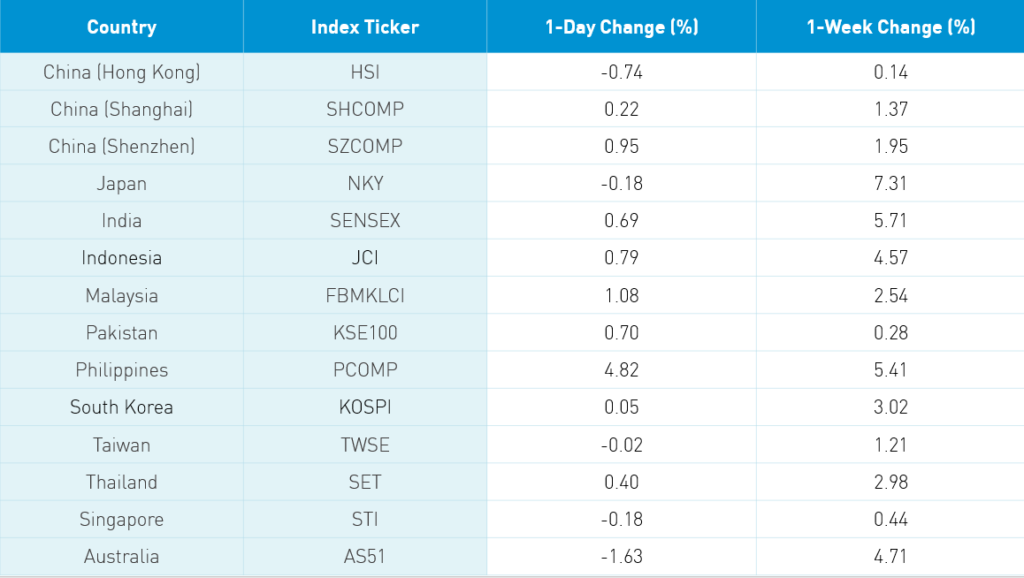

China & Hong Kong Equities Rise On The Week (Not A Typo), Week In Review

4 Min. Read Time

Week In Review

- Asian equities were mixed on Monday as China moves forward with national security legislation to be applied in Hong Kong and the US considers the removal of Hong Kong's special trade status.

- Asian equities rose on Tuesday and Meituan Dianping released Q1 earnings that beat analysts' estimates, which had been lowered due to poor sentiment surrounding food delivery during quarantine. Although growth was lower than previous quarters, the consensus was shown to have been too negative.

- Discount e-retailer Vipshop released its Q1 results on Wednesday. The release detailed how management was able to cut costs amid the pandemic and resulting slump in demand. CSPC Pharmaceutical joined the STAR board, a Nasdaq-style growth exchange, which contains mostly tech companies.

- Social network Momo released its Q1 results before the US market open on Thursday, beating lowered expectations. Asian equities were largely lower as tech suffered on US-China political rhetoric.

Friday’s Key News

Today’s Asian market action was heavily skewed by what brokers are calling the largest MSCI trading event ever. In the US, passive investors such index funds and ETFs need to trade at today’s close globally in order to have their portfolios aligned with MSCI’s Semi-Annual Index Review. Stepping back, the market did surprisingly well this week considering the doom and gloom headlines. Is this the wall of worry that stocks climb? Maybe, as it is hard not to notice the stampede out of the three biggest Emerging Market ETFs now totals $13.5 billion year to date.

Hong Kong was off today, but it is worth noting the large divergence between Hong Kong-domiciled stocks, which were down, and China-domiciled stocks, which were up. Both are listed in Hong Kong, but many of the former are geared toward the local economy while the latter do most of their business in China.

Yesterday, I referenced the Vietnam War quote: “we had to destroy it to save it”. The market seems to be saying that the US is willing to destroy Hong Kong’s economy to save it. With that being said, MSCI-driven trading should keep us from looking to deeply into any trends based on today’s market action. Meituan Dianping jumped +7.08% followed by Tenecent +0.54% and Ping An, which was flat. Geely Auto was crushed, falling -9.56% following a share sale well below yesterday’s close. Not necessarily a Hong Kong or China issue, but I believe share sales like this are an underestimated threat to equity markets. To the upside, Sino Biopharma jumped +7.39% following a broker upgrade. Mainland China’s interest in value stocks was fleeting as growth names were back in favor.

MSCI’s Semi-Annual Index Review included an increased float adjustment for Meituan Dianping (3690 HK) that led to a massive spike in trading today. The value of stock traded increased from yesterday’s $658mm and the 1-year average of $290mm to $2.714B! Volume increased from yesterday’s 37mm and the 1-year average of 24mm to 146mm! Wow! Watch BILI today at 3:59pm EST as it is being added to MSCI indices. I caution that I am not predicting it will go up or down, but it will trade like crazy.

It is equal parts shocking and saddening the number of coronavirus cases here in the US relative to any other country globally. I noticed a Hong Kong newspaper article on a man who was sentenced today to ten days of jail for violating quarantine orders.

We continue to monitor when the House will take up the Senate bill. My hope is that the House sends the bill to committee in order to allow experts such as the SEC to opine on the issue. Putting $1 trillion of US investors’ capital at risk seems illogical. I’ll be calling my local Congressman and telling the 22 year old staffer who answers the phone as much. I recommend that you do the same. At the same time, I’ve become completely fatigued by the US-China political rhetoric circus.

Trip.com (TCOM US), previously known as C-Trip.com, reported Q1 results after the US close yesterday. Expectations for an off quarter were fulfilled as global and domestic travel plummeted. While the company managed to cut sales and marketing expenses, general and administrative expense increased 136% YoY due to “bad debt provisions of RMB 1.2 billion for increased receivable mainly due to the refunds for reservation cancellations.” The company’s Q2 revenue forecast is equally depressing as the Chinese love for travel is curtailed.

- Revenue declined -42% to $669mm (RMB 4.7B) which beat analyst expectations

- Gross profit was halved to RMB 3.511B from 6.475 YoY

- Total operating expense RMB 5.020B versus RMB 5.590

- Diluted EPS loss -$1.27 (RMB -8.98) versus $3.23 (RMB 7.45) YoY

- Q2 Revenue forecast is a decline of 67% to 77% YoY

H-Share Update

The Hang Seng opened lower and stayed down for the count closing -0.74%/-171 index points at 22,961 as volume surged 34% from yesterday and nearly twice the 1-year average. Breadth was off with 19 decliners and 29 advancers led lower by AIA -2.86%/-62 index points, HSBC -3.11%/-55 index points and China Construction Bank -1.46%/-29 index points. Today’s best and worst performers were Sino Biopharma, which surged +7.39%/+20 index points, and Geely Auto, which dove -9.56%. China-domiciled companies outperformed Hong Kong-domiciled companies +0.1% versus -0.66%. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.56% with healthcare +3.39%, utilities +2.6%, staples +2.13%, tech +1.28%, discretionary +1.19%, materials +1.1%, real estate +0.65%, communication +0.45%, industrials +0.06%, financials -0.53%, and energy -0.65%.

Southbound Connect volume was light in mixed trading. Volume leader Tencent saw buyers outpace sellers by 3.5 to 2.7, Meituan Dianping saw sellers outpace buyers by 2 to 1, and Sino Biopharma saw buyers outpace sellers 3 to 1. Mainland investors bought $147mm worth of Hong Kong stocks today as Southbound Connect accounted for less than 4% of Hong Kong turnover

A-Share Update

Shanghai & Shenzhen gained +0.22% and +0.95%, respectively, on light volume and decent breadth with 2,142 advancers and 1,459 decliners. Mid and small caps returned to their winning ways. The Mainland stocks within the MSCI China All Shares Index gained +0.83% with communication +2.43%, health care +2.42%, staples +2.04%, discretionary +1.66%, industrials +0.75%, tech +0.65%, materials +0.59%, utilities -0.07%, energy -0.22%, financials -0.42%, and real estate -0.77%.

Northbound Stock Connect volumes were elevated as foreign investors were net buyers of Mainland stocks today. Volume leader Kweichow Moutai saw buyers outpace sellers by almost 2 to 1 today. Foreign investors bought another $715mm worth of Mainland stocks, bringing the weekly total to $2.132 billion. Today’s Northbound Connect trading jumped to over 7% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 7.14 versus 7.15 yesterday

- CNY/EUR 7.94 versus 7.90 yesterday

- Yield on 1-Day Government Bond 1.35% versus 1.35% yesterday

- Yield on 10-Year Government Bond 2.71% versus 2.72% yesterday

- Yield on 10-Year China Development Bank Bond 3.00% versus 3.00% yesterday