Fundraising Begins For JD.com’s and NetEase’s Hong Kong Listings

2 Min. Read Time

Key News

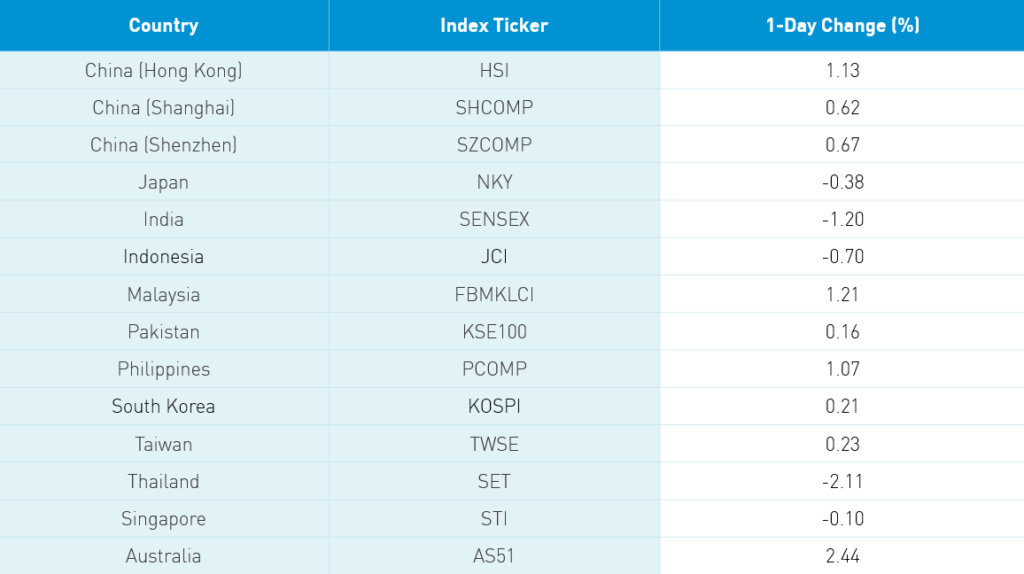

Asian equities enjoyed another day of following US equities higher. The big news in Hong Kong was the $5B bailout of Cathay Pacific from the Hong Kong government and Air China. US-listed TAL Education and New Orient Education are rumored to be following in the footsteps of Alibaba, NetEase, JD.com, Trip.com (formerly C-Trip.com), Baidu, and Pinduoduo with Hong Kong listings. JD’s pending Hong Kong listing is reportedly 26X oversubscribed. Volume leaders i.e. the Growth Trio Tencent +0.88%, Alibaba HK 0.0% and Meituan Dianping -2.13%.

With NetEase’s Hong Kong listing taking place, investors are likely taking money from the growth stocks to fund the listing. This should be a short-term issue as NetEase’s Hong Kong IPO was reportedly already 44X times oversubscribed. Many value companies, autos, and Macau casinos had a strong day as Hong Kong’s bull run extended to 7 consecutive days. Autos such as Geely +3.85% gained on stronger China auto sales, which rose +1.9% in May from a year ago while mainland listed Changan Auto registered May sales growth of +54% YoY according to a broker.

Mainland China posted modest gains in a broad rally across sectors. Healthcare rebounded as the news that an antibody vaccine entered a clinical trial with human testing. I’m surprised markets didn’t notice the news from the WHO that asymptomatic carriers of coronavirus weren’t contagious. I have appreciated the opportunity in quarantine to bond with the family. However, the economic consequences have been disastrous.

H-Share Update

The Hang Seng opened higher and kept heading higher until a late afternoon swoon capped gains at +1.13%/+280 index points to close at 25,057. Volume was off -3.9% from yesterday though remained above the 1-year average while breadth was strong with 43 advancers and 6 decliners. Index heavyweights led the way with AIA +2.7%/+70 index points, HSBC -1.59%/-39 index points and China Mobile +3.61%/+37 index points. Wharf Real Estate was the best performer +5.74%/+6 index points while AAC Tech was the worst -2.04%/-1 index point. Hong Kong-domiciled stocks continued their outperformance versus China-domiciled stocks +1.27% versus +1.12% using the HS HK 35 and HS China Enterprise indexes as proxies. The Chinese companies within the MSCI China All Shares Index gained +0.77% with utilities +1.8%, staples +1.61%, healthcare +1.35%, materials +1.25%, communication +1.15%, energy +1.14%, real estate +1.112%, financials +0.89%, industrials +0.54%, tech +0.33%, and discretionary -1.59%.

Southbound Connect volumes were moderate in mixed trading as the most heavily traded names Tencent, Meituan Dianping and Seminconductor Manufacturing all saw sellers outpace buyers by small margins. Mainland investors bought $92mm worth of Hong Kong-listed stocks today as Southbound Connect accounted for 7.5% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen moved from the lower left to the upper right closing near the day’s high +0.62% and +0.67%, respectively, as volume declined nearly -10% from yesterday. Breadth was positive with 2,027 advancers and 1,534 decliners. Large, mid and small caps were in-line with one another. The Mainland stocks within the MSCI China All Shares Index gained +0.58% with communication +1.9%, healthcare +1.89%, energy +0.8%, discretionary +0.65%, staples +0.6%, utilities +0.56%, industrials +0.49%, tech +0.37%, materials +0.27%, financials +0.18%, and real estate -0.27%.

Northbound Connect volumes were moderate to light though foreign investors continue to buy Mainland stocks. Volume was mixed between buyers and sellers with the former managing to outpace the latter by a small margin. Volume leader Kweichow Moutai had buyers outpace sellers by a small amount while BOE Technology had sellers take profits after yesterday’s monster move. Foreign investors bought $653mm worth of Mainland stocks today as Northbound Connect accounted for nearly 5% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 7.08 versus 7.07 yesterday

- CNY/EUR 8.03 versus 7.99 yesterday

- Yield on 1-Day Government Bond 1.35% versus 1.90% yesterday

- Yield on 10-Year Government Bond 2.80% versus 2.81% yesterday

- Yield on 10-Year China Development Bank Bond 3.14% versus 3.13% yesterday