Tencent’s IQ Buyout Rumor, Markets Climb The Wall of Worry

5 Min. Read Time

This week we will be hosting three webinars, please join us.

- The World's Second Largest Bond Market Is Now Open: A Discussion With KraneShares Europe and Sanjay Rao of Bloomberg

Today at 2 pm GMT - One Year Review: A Conversation with Nancy Davis of Quadratic Capital and Jonathan Krane, CEO of Krane Funds Advisors

Today at 11 am EST - A Larger Piece of the Pie: A Discussion With MSCI on Choosing the Right Mainland China Exposure,

June 18th at 10 am EST

Key News

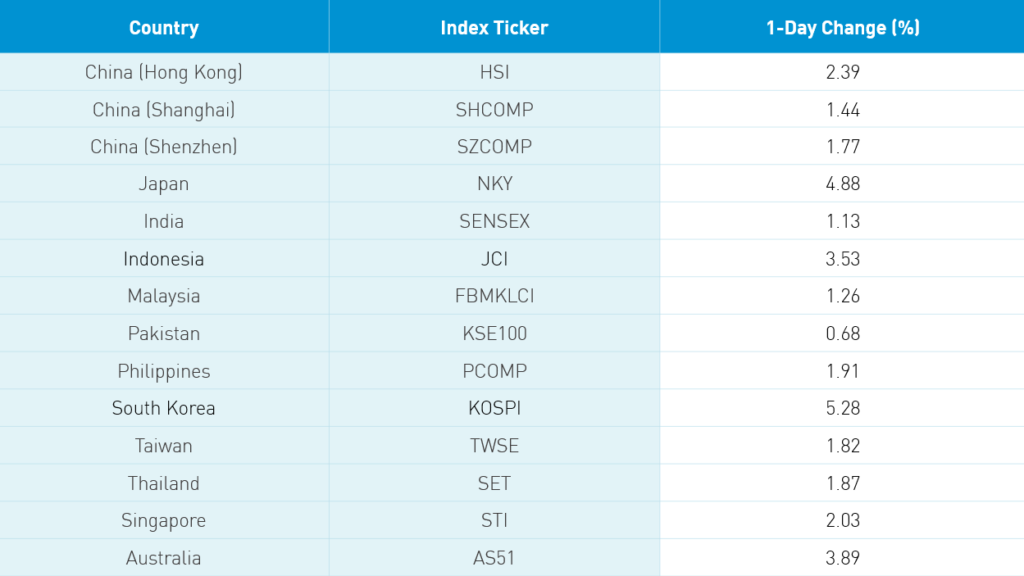

Asian equities ripped higher last night on news of President Trump’s infrastructure stimulus, confirmation of Secretary of State Pompeo’s Hawaii meeting tomorrow with his Chinese counterpart, continued Fed corporate bond buying, and the confirmation of a Reuters story that the Commerce Department will allow Huawei to participate in setting 5G global standards. Beijing’s recent coronavirus flare up led to nearly 80,000 residents being tested and several areas seeing new restrictions though day over day cases fell. The market overlooked a China/India border flare up, North Korea blowing up a meeting building near the DMZ, and the fact that the Huawei news does not change the US’ position towards the company, but helps the US set global standards.

It was a very strong and broad rally in Hong Kong though last night, but I was disappointed volumes weren’t stronger. They were off -10% from yesterday. Growth names led the way with volume leaders Tencent +3.51% on news the company won a government technology build out contract, Meituan Dianping +7.84% on a broker price target upgrade to HK $210 versus today’s close HK $172, and Alibaba HK +3.09%. Semiconductor Manufacturing ripped +11.9% higher as speculation its STAR Board listing is getting closer while NetEase jumped +3.68% on news it will release a Lord of the Rings mobile game with Warner Brothers. Tech had a strong day on the Huawei news with ZTE HK +15.2%. Mainland China also rose on the day on strong volume though a touch off from yesterday. Material stocks had a strong day on news Tesla will buy cobalt from Glenore for its Shanghai and planned Berlin plants. Healthcare had a strong day on the unfortunate news of an increase in US cases and Beijing’s flare up.

Private equity heavyweights Warburg Pincus and General Atlantic are taking 58.com (WUBA) private for $56 a share or a total valuation of $8.7B. The Craigslist of China is going private as investors failed to give the company a proper valuation (P/E of 7). The deal makes sense to me relative to deal Tencent is getting taking BITA US private. However, I suspect we may see WUBA go public again as a Mainland listing could be interesting.

The South China Morning Post is reporting that Tencent wants to buy Baidu’s stake in video streamer iQiyi (IQ US) which it had previously spun off. The article points out Tencent’s Tencent Video has lagged versus IQ, which increased revenue 11% in Q1 though both lag Bilibili (BILI US)’s exceptional 69% Q1 revenue growth. BILI is focused on the younger generation with an emphasis on video gaming and cartoon graphics. The article makes a good point that selling IQ could help Baidu as it looks to relist in Hong Kong.

With the extreme volatility in US equity and fixed income markets, US equities are taking center stage with US investors for good reason as core assets should receive the majority of attention. At the same time, I can’t help but notice the continued outperformance of China and select sectors within Emerging Markets. If China was the “First In First Out” of the coronavirus, South Korea, Taiwan and Asia are next. India and Latin America are in the thick of fighting coronavirus at the moment. The purge of US-listed China equity ETFs amounts to -$1B year to date and -$1.5B over the last year and broad Emerging Markets hasn’t fared much better -$10B YTD and -$10.9B over the last year. While broad Emerging Markets has lagged the US YTD, China has outperformed despite the political rhetoric. The deeper story the outperformance of growth stocks in Emerging Markets. Look at South Korea where the broad Kospi Index (over 750 stocks) is -2.7% YTD while the Kosdaq (over 1,200 stocks) is up +9.7%. This scenario of growth is even more true in China. Against the backdrop of US Fed balance sheet expansion and a growing budget deficit, the dollar has weakened over the last month. I wish more investors would notice!

I live outside of NYC in CT along the flight path from Newark airport and JFK for flights to Asia and Europe. As a previous frequent traveler, I have love flight apps such as FlightAware. This app is cool as you can track where a plane is going. I often ask my kids when we spy a plane to try to guess where it is going. There aren’t many flights to notice these days, but when we look up a flight many are air freight planes. Air freight rates, according to something called the Drewry Air Freight Average, have doubled since February. The recent easing of passenger flight restrictions to/from China should only increase air freight as the cargo holds are often loaded with air freight. I would love to know how much air freight has gone between the US and China this year. Kudos to Ken in Hong Kong with ICBC. He noted a pick up US truck freight along similar lines.

H-Share Update

The Hang Seng gapped higher at the open and stayed there to close +2.39%/+565 index points at 24,344. Volumes were off -10% from yesterday, which is disappointing as I would have liked to have seen more conviction on the strong move. Breadth was great with 50 advancers and 0 decliners as index heavyweights Tencent +3.51%/+87 index points, HSBC +2.47%/+56 index points, and AIA +2.1%/+52 index points. Today’s best performer was food and beverage company Want Want China Holdings +8.66%/+8 index points after releasing earnings while Ping An Insurance was the “worst” performer +0.5%/+7 index points. Hong Kong and China-domiciled companies moved +2.3% and +2.19% using the HS HK 35 and China Enterprise Indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index rose +2.96% with tech 6.18%, discretionary +5.13%, energy +3.71%, healthcare +3.34%, communication +3.29%, utilities +2.59%, real estate +2.53%, industrials +2.48%, materials +1.99%, staples +1.69%, and financials +1.26%.

Southbound Connect volumes were moderate as Mainland investors were net buyers of Hong Kong stocks. Trading in Tencent was fairly balanced while Meituan Dianping saw net selling. Semiconductor Manufacturing had a strong day.

A-Share Update

Shanghai and Shenzhen opened higher and traveled higher over the course of the trading day to close +1.44% and +1.77% at 2,931 and 1,898, respectively. Volumes were off -7% but remained elevated while breadth was strong with 3,069 advancers and 639 decliners. Mid and small caps outperformed large caps by a small amount on a strong day. The Mainland stocks within the MSCI China All Shares Index gained +1.79% with materials +2.56%, discretionary +2.49%, tech +2.45%, healthcare +2.36%, utilities +1.94%, real estate +1.63%, industrials +1.48%, staples +1.39%, energy +1.31%, financials +1.25%, and communication +0.95%.

Northbound Connect volumes diverged as Shanghai volumes were moderate/light while Shenzhen volumes were high as foreign investors were net buyers of Mainland stocks today. Liquor stock Wuliangye Yibin was sold 2 to 1 while peer Kweichow Moutai was bought nearly 2 to 1 along with Ping An Insurance, which was also bought 2 to 1. Gree Home Appliances was sold by nearly 3 to 1. Foreign investors bought $560mm worth of Mainland stocks today after selling $570mm yesterday

Last Night’s Exchange Rates & Yields

- CNY/USD 7.08 versus 7.09 yesterday

- CNY/EUR 7.99 versus 7.99 yesterday

- Yield on 1-Day Government Bond 1.47% versus 1.47% yesterday

- Yield on 10-Year Government Bond 2.84% versus 2.79% yesterday

- Yield on 10-Year China Development Bank Bond 3.16% versus 3.12% yesterday