Late Night Comedy

3 Min. Read Time

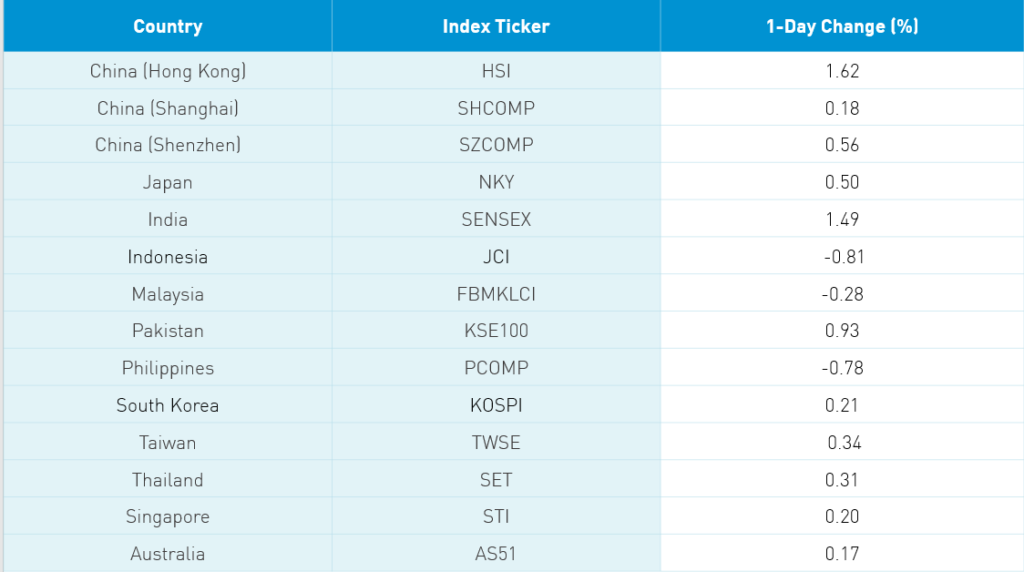

East Asian equity indexes showed a V-shaped rebound in the morning after President Trump used Twitter to confirm the US-China trade deal is intact, after White House advisor Peter Navarro said the deal was over in a Fox News TV interview last night. I’m a little surprised markets took the comments literally, as Mr. Navarro is a widely known China hawk and we had US Trade Representative Lighthizer’s Congressional testimony that the trade deal was on last week.

We know throwing China under the bus will be a key election strategy to placate the base, though it is apt to be more bark than bite. The US economy is in a fragile state that a trade war would only exacerbate and would jeopardize a Q3 rebound.

Hong Kong had a strong day led by volume leader Tencent +4.89%, Alibaba HK +3.29% and HKeX +2.7% after Hong Kong head, Carrie Lam, mentioned that ETF Connect could be coming, which would allow Mainland investors access to HK listed ETFs. Names worth noting include Meituan Dianping +3.7%, NetEase +2.55%, and Semiconductor Manufacturing +9.3% pre-STAR board listing for the semi company. One broker noted that Tencent is benefiting from a catch up/rotation after strong performance of e-commerce names. A Mainland broker noted that Tencent’s PUBG Mobile game earned over $220mm in May +40% YoY as gamers globally are attracted to the game.

My brother in law, Matt, shared an institutional broker’s survey on where investors expect the Hang Seng to close year-end. Just over half of the respondents predicted a flat/down, though I am more optimistic due to the index changes coming. Today, the index is 49% financials while consumer discretionary is just 1.32%. In August, Hang Seng will likely announce Alibaba HK and Meituan Dianping which will raise discretionary to around 15% while cutting financials to under 40%.

The Mainland market was led higher by DnD, drugs and drinks, as healthcare and alcohol stocks in staples had a strong day. A Mainland healthcare company announced it has been given permission to begin testing a coronavirus vaccine on humans. Kweichow Moutai +2.47% overtaking ICBC as the biggest stock by market cap in China. ZTE was off -5.59% after a controlling shareholder sold 69mm shares cutting its stake to 23.4%. A Mainland media source noted there were 22 new coronavirus cases, though nine were travelers coming into China.

Tencent filed a stake in Chinese EV maker NIO.

21Vianet (VNET US) announced a $150mm investment from Blackstone, leading to a jump of +17.4% yesterday.

MSCI’s market classification review will be announced today after the US market close. The release is highly unlikely to include China A, as MSCI’s issues with raising the inclusion remain (trade settlement, lack of a China A futures and HK/China holiday schedule).

H-Share Update

The Hang Seng opened lower but quickly snapped back, gaining +1.62%/+396 index points to close at 24,907. Volumes were flat from yesterday while breadth was positive with 39 advancers and 9 decliners. Today’s best performer was Tencent +4.89%/+135 index points, AIA +2.46%/+64 index points and HSBC +2.0.4%/+47 index points. Link REIT was the day’s worst performer -1.39%/-5 index points. HK domiciled companies outperformed Chinese domiciled companies +1.46% versus +1.16% using the HS HK 35 and China Enterprise as proxies. The Chinese companies listed in HK within the MSCI China All Shares gained +2.05% with communication 4.35%, healthcare +2.73%, tech +2.61%, discretionary +2.33% staples +1.16%, financials +0.58%, energy +0.21%, industrials +0.14%, real estate +0.07%, utilities -0.02%, and materials -0.56%.

Southbound Connect is closed the remainder of the week.

A-Share Update

The Shanghai & Shenzhen also opened lower but quickly rebounded gaining +0.18% and +0.56% to close at 2,970 and 1,947. Volumes were off -8% from yesterday though well above the 1 year average. Breath was off with 1,189 advancers and 2,485 decliners. The Mainland stocks within the MSCI China All Shares gained +0.89% with communication +2.72% healthcare +2.41%, staples +2.16%, utilities +1.58%, tech +0.96%, industrials +0.29%, discretionary +0.18%, financials +0.04%, materials -0.21%, real estate -0.61%, and energy -0.61%.

Northbound Connect volumes were moderate in mixed trading as Shanghai had more buying than Shenzhen. Volume leader Kweichow Moutai and Ping An had a high two-way volume. East Money Information had buyers outpace sellers. Foreign investors bought $106mm of Mainland stocks today as Northbound Connect trading accounted for 5.2% of mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 7.06 versus 7.07 yesterday

- CNY/EUR 7.98 versus 7.94 yesterday

- Yield on 1-Day Government Bond 1.38% versus 1.45% yesterday

- Yield on 10-Year Government Bond 2.91% versus 2.92% yesterday

- Yield on 10-Year China Development Bank Bond 3.23% versus 3.2% yesterday

- China's Copper Price Change: 0.21%