Shanghai Clears 3K Level on Strong Volume, PBOC Lending Cuts, Positive June Manufacturing PMI

4 Min. Read Time

Key News

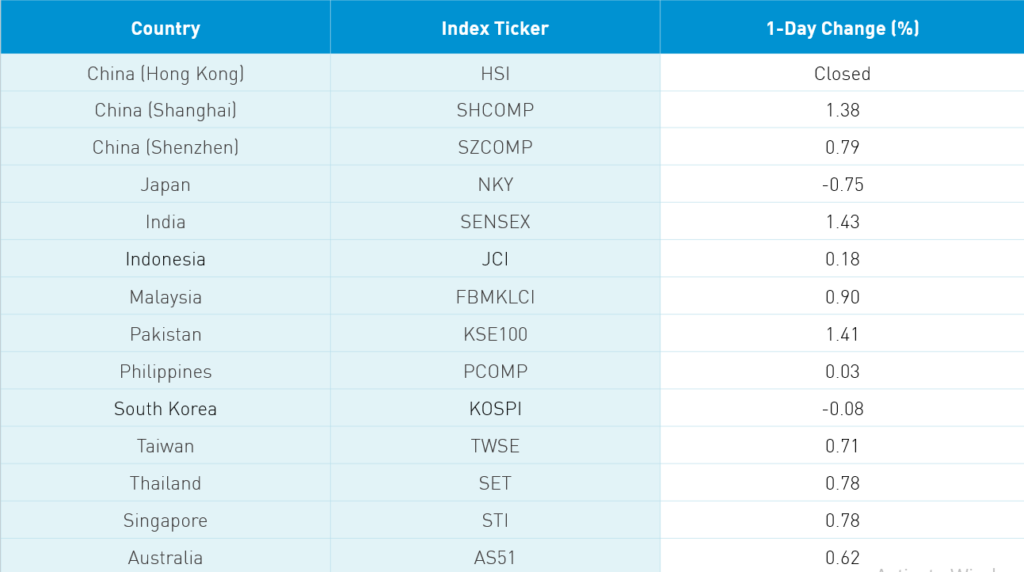

Asian equities had good day as a string of June Manufacturing PMIs have shown that strict adherence to quarantines has largely allowed Asia to go back to work. Hong Kong was closed today for the Special Administrative Region (SAR) Establishment Day marking the 23rd anniversary of the hand off of Hong Kong to China from the UK. As you may have guessed, the timing of the new security law just prior to the SAR holiday was not a coincidence. Our Hong Kong brokers were on vacation but we have several brokers based in the Mainland who provided color on today’s market action.

Last night the “private” PMI was released. I’ve heard that people are skeptical of Chinese data so I will point out the Caixin PMI survey is conducted by the London Stock Exchange-listed IHS Markit. The “private” PMI, unlike the “official” PMI, surveys medium and small companies. However, the survey size is smaller, which can lead to a more volatility. For the diffusion index, readings above 50 indicate a month-over-month expansion and readings over 50 indicate contraction. The reading improved from May led by an increase in output, new orders, and, not surprisingly, business confidence. Nonetheless, we should temper our enthusiasm as new export orders are still contracting and leading to a decline in employment. It appears Chinese manufacturers are increasingly focused on selling within China as other countries weather the economic consequence of quarantines.

In addition to the Caixin Manufacturing PMI, the PBOC cut lending and refinancing rates geared to small businesses and farmers by 0.25% to 1.95%, 2.15% and 2.25% for 3 month, 6 month and 1-year loans, while the rediscount rate was cut by 25bps to 2%. The targeted move highlights the fact that the PBOC hasn refrained from cutting broad interest rates and left plenty of dry powder for a rainy day. Getting credit to small businesses has been a significant policy effort. Property stocks in the mainland market absolutely ripped in response to the PBOC move.

Mainland volumes jumped +21% from yesterday despite the absence of foreign trading due to Northbound Stock Connect’s being closed for the Hong Kong holiday. The Shanghai Composite rose above the 3,000 level for the first time since the early March global meltdown. Technical analysts love a strong move on high volumes like today though confirmation of the breakout above a psychological level still needs to be confirmed in the coming days and weeks. We saw some profit-taking in healthcare while Mainland growth stocks lagged value stocks for the first time in ages. It is possible that growth investors are taking profits to fund participation in the upcoming Semiconductor Manufacturing (SMIC) STAR Board IPO, which is rumored to be scheduled for Friday. The SMIC IPO is going to be a monster as it will be like nothing we’ve ever seen candidly. Liquor stocks propelled staples higher with Kweichow Moutai +2.15% and Wuliangye Yibin +6.35%. Friday is a US holiday but getting CLN out will be fun.

The onslaught of negative Western media coverage on China has been something else. Uncle! Personally, I believe the emphasis on China is a distraction technique from domestic US issues. It is so as to say ook over there and not here. That being said, investors in China don’t seem to care. Overnight, we had a tweet saying that the FCC will be banning Huawei and ZTE from selling telecom gear to rural areas in the US, the unanimous passage of the controversial Hong Kong national security law, India’s ban on TikTok in China (I’m sure several hundred million Indian teenagers are not happy about this), etc. What was the Chinese investor’s response? Nada. Having studied the Chinese market for seven years now, it does behave differently than other equity markets. The lack of correlation may be the last free lunch this market has. For what it is worth, I’m enjoying my free lunch!

Pinduoduo (PDD US) announced its CEO and founder will become Chairman as the Chief Technology Officer and a founding member of the firm becomes CEO. I had noticed Mainland media coverage of the former CEO becoming the second richest person in China, which isn’t necessarily a good thing as it could lead to increased scrutiny of the firm. Remember that Jack Ma retired after garnering significant attention for being the richest person in China. As Chairman, the founder is apt to be very much hands-on though it could lead to PDD relisting in Hong Kong. The former CEO was very focused on growing revenue at the expense of net income. Hong Kong listing rules have profitability requirements. This is pure conjecture on my part, but I will be curious to see whether PDD reaches profitability in the next quarter or two, which would pave the way for a Hong Kong listing.

Did you know that SEC Chairman Jay Clayton served as counsel for Alibaba’s US IPO? Alibaba employed several law firms on the IPO including Mr. Clayton’s former employer Sullivan & Cromwell. Interpret this as you see fit though the phrase “do as I say not as I do” comes to mind for me.

H-Share Update

Hong Kong was closed in observance of the SAR holiday.

A-Share Update

Shanghai and Shenzhen overcame a mid-day swoon to close +1.38% and +0.79% at 3,025 and 1,991, respectively. Volume jumped 21.8% day over day! Breadth was off with 1,717 advancers and 1,906 decliners. Large caps outperformed mid and small caps by a significant margin today. The Mainland stocks within the MSCI China All Shares Index gained +1.66% with real estate +6.1%, staples +2.98%, discretionary +2.62%, materials +2.32%, financials +2.24%, utilities +1.83%, energy +1.17%, industrials +1.09%, tech +0.93%, communication +0.13%, and healthcare -1.45%.

Northbound Connect was closed due to the holiday in Hong Kong.

Last Night’s Exchange Rates & Yields

- CNY/USD 7.07 versus 7.06 yesterday

- CNY/EUR 7.94 versus 7.95 yesterday

- Yield on 1-Day Government Bond 1.33% versus 1.17% yesterday

- Yield on 10-Year Government Bond 2.85% versus 2.82% yesterday

- Yield on 10-Year China Development Bank Bond 3.15% versus 3.14% yesterday