Breakout Week Wraps With Profit-Taking, Week In Review

3 Min. Read Time

Week In Review

- US-listed online media company SINA (SINA US) announced on Monday it had received a privatization proposal from an entity controlled by Chairman and CEO Charles Cao for $41 a share versus Thursday’s close of $36.67. The entity already owns 12% of SINA’s shares currently, which lends credibility to the offer.

- The rally in Mainland Chinese equities continued on Tuesday while Hong Kong stocks saw some profit taking

- Reuters reported on Wednesday that Alibaba’s Ant Financial would go public this year in Hong Kong. The company will likely aim for a $200 billion valuation after selling between 5% to 10% of its stock. However, the company denied considering an IPO on Thursday.

- The rally in China stocks remained unbroken on Thursday despite negative headlines. Who is buying? We suspect buyers include active managers who have been tragically underweight to China of late.

Friday's Key News

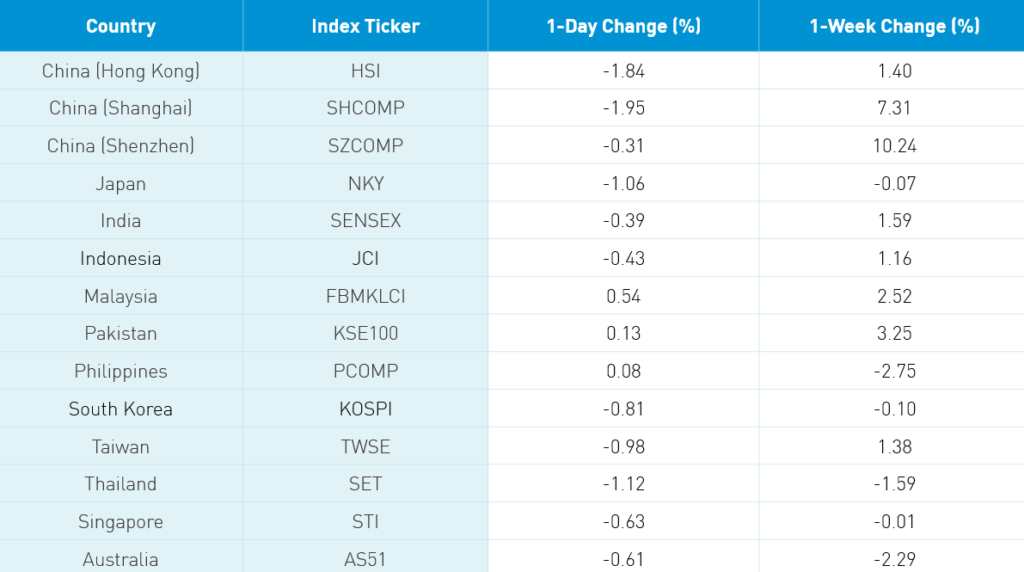

Asian equities slumped into the weekend on rising cases in the US, Japan and, to a lesser degree, Hong Kong. Both the Mainland and Hong had a pullback today after posting gains for the week.

Hong Kong volume leaders Tencent and Alibaba HK were down -2.93% and -2.37%, respectively. Meanwhile, everything came down fairly uniformly with Meituan Dianping -0.76%, Netease HK -1.29%, and JD.com HK -2.11%. There was shockingly little single stock news for Hong Kong. The Mainland market finished a great week with some profit taking.

Western media is focused on China’s pension plan reducing its position in insurance company People’s Insurance Company of China (PICC). One broker believes that up to ten stocks could see selling from the pension plan, which is being heralded as a sign that the regulators believe the market has gone too far too fast. Pension plans tend to rebalance at month end or around high-volume events such as futures rolling in order to limit their impact. We’ve seen massive volume in the Mainland of late, which makes trimming a position make perfect sense. One Mainland broker simply called today a correction driven by profit taking.

DND, drinks and drugs, were up on the day as Kweichow Moutai and Wuliangye Yibin rose +0.46% and+1.61%, respectively, while healthcare was broadly higher. Northbound Stock had outflow of $627mm though for the week +$4.023B of net buying by foreign investors.

The SEC held their Emerging Markets Roundtable yesterday. According to the notes from our SEC law firm, the first panel comprised solely of short sellers was negative on China! Shocking. I find it a little ironic that without frauds there would be no short sellers. It is amazing only one mutual fund family of significance participated in the day long panel. One! I find it absolutely shocking that the largest mutual fund families have done nothing to defend their shareholders on this issue. The mutual fund lobby Investment Company Institute (ICI) did not participate either.

The World Artificial Intelligence Conference (WAIC) has been this week. I will gather notes from CEO speeches etc. for Monday delivery!

H-Share Update

The Hang Seng went from upper left to lower right -1.84%/-482 index points to close at 25,727. Volume was off almost -6% from yesterday but still 2X the 1-year average. Breadth was awful with only 6 advancers and 43 decliners led by Tencent -2.93%/-89 index points, AIA -1.83%/-48 index points and HSBC -1.89%/-42 index points. Geely Auto was the day’s best performer +3.9%/+12 index points while China Life -6.7%/-29 index points. China-domiciled companies -2.23% versus Hong Kong-domiciled companies -1.19%. The Chinese companies listed in Hong Kong and within the MSCI China All Shares -2.09% with tech -0.46%, staples -0.79%, health care -0.84%, discretionary -0.94%, real estate -1.56%, industrials -1.91%, utilities -2.13%, materials -2.22%, energy -2.4%, financials -2.69%, and communication -2.9%.

Southbound Stock volumes have come off a bit but remain at 2X the 1-year average. Volume leader Semiconductor Manufacturing was sold slightly, Tencent was bought heavily, and Xiaomi saw net buying as well.

A-Share Update

Shanghai and Shenzhen bounced around the room but fell toward the close to end the day -1.95% and -0.31% at 3,383 and 2,251, respectively. Volumes were off -6.4% from yesterday but remained 2.5X the 1-year average while 1,358 stocks advanced and 2,398 stocks declined. Large cap stocks fell more than mid and small caps. The Mainland stocks within the MSCI China All Shares Index fell -1.36% with health care +0.94%, communication +0.69%, discretionary +0.41%, staples +0.26%, tech -1.18%, utilities -1.31%, industrials -1.59%, real estate -1.95%, materials -2.76%, financials -3.61%, and energy -3.7%.

Northbound Stock Connect volumes were elevated again as foreign investors became net sellers overnight. Shanghai Connect volume leaders Kweichow Moutai and Ping An were both bought by small margins. Shenzhen connect volume leader Gree Electric Appliances was bought 2 to 1, liquor stock Wuliangye Yibin was sold 7 to 5, and East Money Information was sold by a small margin. Foreign investors sold -$627mm worth of Mainland stocks today. For the week, foreign investors bought $4.023B worth of Mainland stocks.

Last Night’s Exchange Rates & Yields

- CNY/USD 7.00 versus 6.99 yesterday

- CNY/EUR 7.92 versus 7.91 yesterday

- Yield on 1-Day Government Bond 1.45% versus 1.45% yesterday

- Yield on 10-Year Government Bond 3.03% versus 3.08% yesterday

- Yield on 10-Year China Development Bank Bond 3.43% versus 3.47% yesterday