Chinese Equities Climb The Great Wall of Worry

3 Min. Read Time

Key News

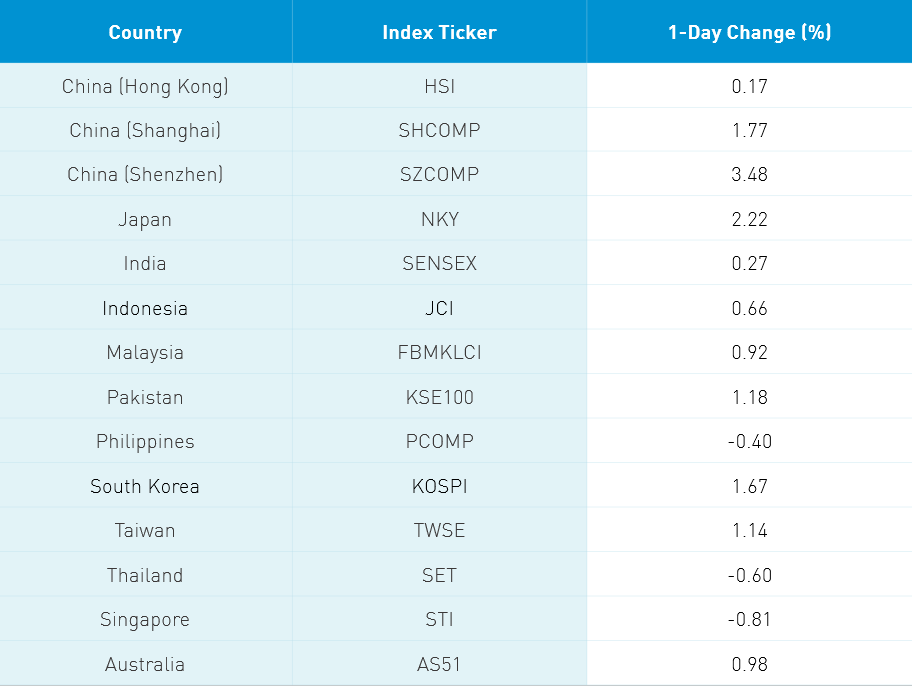

Asian equities started the week off higher despite initial concerns over President Trump’s Friday announcement that a Phase Two deal isn’t likely. The US and China continue to shadow box with tit for tat responses though neither is going to draw blood by doing anything that would jeopardize a hoped-for US Q3 recovery. Hong Kong eased off an intra-day high of +1.46% to close +0.17% on chatter that daily new cases in Hong Kong have reached 50. After the close, Hong Kong announced tighter restrictions for bars and restaurants after having closed school this week.

Growth leaders dominated the volume leaderboard of late. However, they took a day off on Monday as Tencent fell -1.01%, Alibaba HK -0.39% on news Jack Ma’s stake fell below 5% after selling shares, and Meituan Dianping -1.06%. However, Semiconductor Manufacturing rose +1.7% in anticipation of the company’s STAR Board IPO. Geely Auto rose +8.3% after Chinese auto sales data jumped 11% in June and last week’s news they would list on the STAR Board as well. Healthcare had a strong day as the highly respected investment firm Hillhouse bought 8% of Mainland-listed Joincare Pharma (600380 CH), which jumped +10% on the news. It is worth noting that Joincare was up by over 60% YTD before today’s move. I mention this as obviously Chinese equities have done very well though it is only in the last few days that we have seen inflows into US-listed Chinese equity ETFs. It is worth noting that Hillhouse was only willing to buy the stake after Joincare’s stock had risen by a certain amount.

Mainland China had a strong day as gold stocks joined DND, drinks and drugs, in a rally as the market shook off regulatory jawboning, which had threatened to stifle the market’s rise. Battery maker CATL rose +9.91% after announcing a deal with Honda. Recent gains in Mainland equities have meant a selloff in bonds. One Mainland bond broker said, “Bonds are under non-stop selling pressure,” as the 10-Year Treasury yield is now 3.06% versus a low of 2.48% on April 8, 2020. FTSE Russell received a lot of press for noting that the STAR Board will be included in their indices at some point and the firm would consider raising it’s A Shares inclusion later this year.

China Agricultural Supply and Demand Estimates were released overnight. Estimated soybean imports from the US is being raised to 94mm tons from 91mm. The USDA released export data for the week ended July 2nd and highlighted that China was the largest buyer of both soybeans and corn.

H-Share Update

The Hang Seng bounced around the room to close +0.17%/+44 index points at 25,772. Volumes were off nearly -12% from Friday though remained at nearly 2X the 1-year average. Breath was split with 24 advancers and 24 decliners with HSBC +2.34%/+53 index points, Tencent -1.01%/-30 index points, and today’s best performer Geely Auto +8.3%/+28 index points. New World Development Co. was the day’s worst performer -1.84%/-3 index points. Hong Kong-domiciled companies +0.56% versus China-domiciled companies +0.33% using the HS HK 35 and China Enterprise indices as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index rose +0.38% with materials +3.67%, staples +3.18%, health care +2.82%, industrials +1.77%, tech +1.71%, energy +1.23%, utilities +1.23%, discretionary +0.79%, real estate -0.16%, financials -0.22%, and communication -0.85%.

Southbound Stock Connect volumes came back to earth at only 2X the usual though Mainland investors continue to buy Hong Kong stocks. Volume leader Semiconductor Manufacturing was flat while Tencent and Meituan Dianping were bought. Mainland investors bought $798mm worth of Hong Kong stocks today as Southbound Connect trading accounted for nearly 13% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen went from the lower left to the upper right +1.77% and +3.48% to close at 3,443 and 2,329, respectively. Volume rose +3.7%, which is nearly 3X the 1-year average while breadth was amazingly low with 3,495 advancers and 268 decliners. Mid and small caps outperformed large caps by 2%. The Mainland stocks within the MSCI China All Shares Index +2.66% with staples +4.22%, health care +3.8%, materials 3.8%, tech +3.3%, industrials +3.1%, energy +2.27%, utilities +2.25%, discretionary +2.11%, communication +1.51%, real estate +0.7%, and financials +0.63%.

Northbound Stock Connect volumes were high as foreign investors bought Mainland stocks. Shanghai Connect’s volume leaders were Kweichow Moutai, which was bought 2.5 to 2, and Ping An Insurance, which was bought 1.4 to 1.1. Shenzhen Connect volume leaders were liquor stock Wuliangye Yibin, which was sold slightly 1.2 to 1.7 and Contemporary Amperex Technology, which was sold slightly 1.1 to 1.3, and Gree Electric Appliances, which was sold 1.0 to 1.1. Foreign investors bought $978mm worth of Mainland stocks today as Northbound Connect accounted for nearly 5% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 6.99 versus 7.00 Friday

- CNY/EUR 7.95 versus 7.92 Friday

- Yield on 1-Day Government Bond 1.27% versus 1.45% Friday

- Yield on 10-Year Government Bond 3.06% versus 3.03% Friday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.43% Friday