Hong Kong Investors Cash Out At The ATM (Alibaba, Tencent & Meituan Dianping), June Export Data Beats Estimates

5 Min. Read Time

Key News

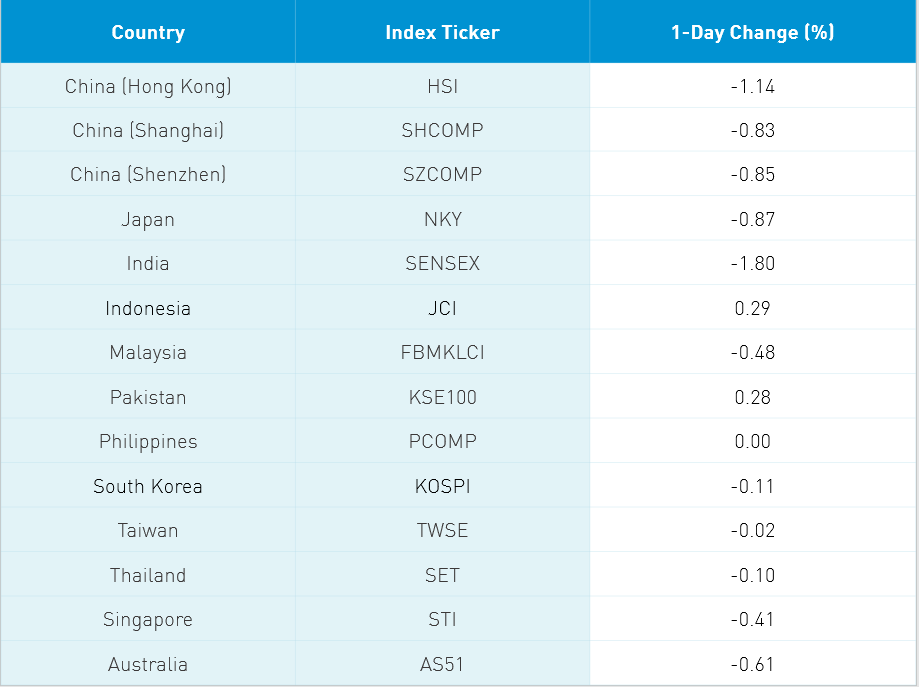

Asian equities succumbed to a raft of negative developments as the US rejected China’s claim to a bunch of rocks in the South China Sea, Hong Kong tightened social distancing rules, and US equities reversed initial gains yesterday. News that the UK will ban Huawei telecom gear by 2027 and that China has cut Lockheed Martin from selling in China (only 2% of revenue) due to Taiwan military gear sales also did little good for Asian equities. Hong Kong tightened social distancing measures to counteract a recent uptick in coronavirus cases by re-closing bars, karaoke parlors, schools, and indoor restaurant seating. My Hong Kong-based colleague Vincent is back to working from home.

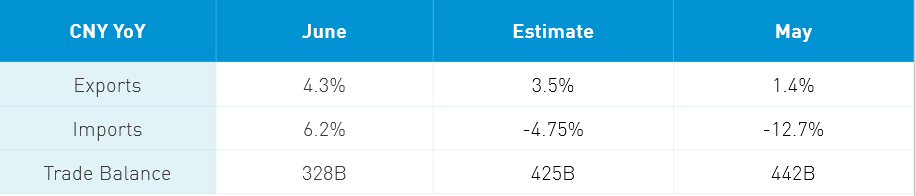

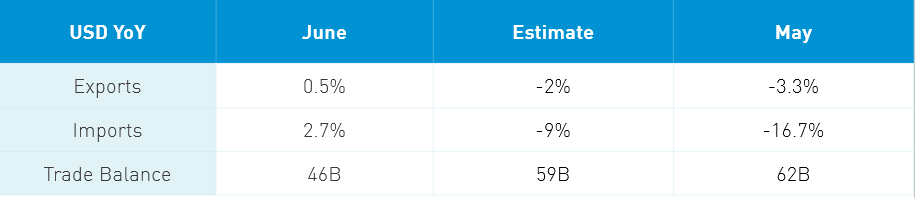

Takeaway: This data was released at 10am local time. Obviously, it came in just a touch stronger than anticipated (only thing stronger is my sarcasm!), which caused markets to reverse initial losses before gravity took effect. Exports to the US rose slightly to 18% of total exports while imports from the US declined slightly to 6.2%. Commodity import volumes were all quite strong month over month. Yesterday, I participated in CNBC’s ETF Edge hosted by Bob Pisani with fellow guest ETF Trends’ David Nadig. In our discussion, I pointed to copper’s rise as a verification of China’s rebound. Today’s commodity data reinforces that point as imports of coal rose +12% year to date, oil +9.9%, soybeans +17.9%, natural gas +3.3% etc. China is certainly not immune to the economic consequence of global quarantines though the strength of the domestic economy should help.

Growth names took the brunt of the selling as volume leader Tencent fell -2.96%, Alibaba HK -5.5%, Semiconductor Manufacturing -0.36%, Meituan Dianping -4.32% and Xiaomi -3.64%. JD.com HK was off -5.4% while NetEase was down by -2.46%. Autos were clipped with Geely Auto falling -5.04% after showing strength thanks evidence that China auto sales had troughed. Healthcare, another market leader, saw profit taking as well. The only bright spots in Hong Kong were Macau casino stocks, which rebounded on news that Guangdong Providence would lift its quarantine of Macau travelers, which led to speculation that gamblers will return. Galaxy Entertainment and Sands China gained +6.1% and +5.03%, respectively.

Mainland investors added to these growth stocks on weakness via Southbound Connect. One broker noted they saw some nibbling on the growth names on the weakness as well. Mainland China also succumbed to profit taking on the negative news though the decline was less severe than in Hong Kong. Volume leaders Kweichow Moutai and Ping An fell -1.12% and -1.29%, respectively. The big news overnight was that foreign investors took profits on growth stocks as Shenzhen Connect (mid/small cap growth stocks) volume was very high on both an absolute and a relative basis compared to Shanghai Connect (large cap value stocks). Foreign investors sold $2.477B worth of Mainland stocks, lowering the YTD inflow to $23.537B.

My Australian friend Drew taught me the saying “The tall poppy gets cut.” Meaning: Get a big ego or get ahead of yourself and you are asking to get your head lopped off. Corrections are healthy and are to be expected. If we step back, I don’t see the fundamental drivers of the rebound being jeopardized though I can’t predict the depth of a potential correction. As we saw last night, the dip was bought. EM is under allocated to due to a massive US home bias. Bloomberg noted that Asian hedge funds have only $68B in assets versus $739B in Europe and $2.298 trillion in the US. I believe investors will nibble on the downdraft. Hong Kong and China will have more not less IPOs in the coming weeks. We also have Hang Seng potentially announcing in August the inclusion of Alibaba, Meituan and Xiaomi in the Hang Seng Index.

Last night I did a video call, on Cisco’s Webex, for what it’s worth, with the Shanghai Stock Exchange in advance of their STAR Board conference this Thursday. It should be a great event if you want to stay up all night! Thankfully, I am on a morning panel. My question to them was where is the Semiconductor Manufacturing (SMIC) IPO? I’m told registration is complete so maybe an IPO on the day of the conference would make sense. My guess is the IPO will gain +1,000% if you are lucky enough to get an allocation, which is hard. It is going to be unlike anything you’ve ever seen. Ever……

Several media outlets are announcing that the PCAOB may exit an agreement that allowed Chinese companies to list in the US without allowing the PCAOB to review the auditors books. The irony of course is the agreement is what allowed the companies to list here to begin with. The US signed the agreement in hopes that China would amend the audit review but that hasn’t happened. The agreement is unlikely to affect the companies currently listed here though it provides China with the opportunity to address the issue. Interestingly, the South China Morning Post had an article today stating that the Financial Stability and Development Committee, which is led by the Vice Premier Li Keqiang and Trade eEnvoy Liu He would implement new rules to combat financial fraud. Liu He’s involvement is a positive sign as an agreement would likely be discussed with the US. This follows news overnight that Luckin Coffee canned their Chairman/founder because he knew about and turned a blind eye to the fraud. Let’s hope the US and China side can use Cisco’s WebEx or Zoom (not playing favorites) to get in touch with one another.

H-Share Update

The Hang Seng opened lower and stayed down for the count to close -1.14%/-294 index points at 25,477. Volume increased +4.4% to nearly 2X the 1-year average while breadth skewed lower with 12 advancers and 37 decliners. Index heavyweights were lower as Tencent fell -2.96%/-86 index points, AIA -1.67%/-43 index points and HSBC -1.07%/-24 index points. Macau’s Galaxy Entertainment was the best performer rising +6.1%/+21 index points and Geely Auto was the day’s worst after falling -5.04%/-16 index points. Hong Kong-domiciled companies were only off -0.22% versus China-domiciled companies -1.61% using the HS HK 35 and China Enterprise indexes as proxies. The Chinese companies listed in Hong Kong and within the MSCI China All Shares Index were down -2.28% with staples -0.29%, industrials -1.37%, financials -1.38%, utilities -1.5%, energy -1.75%, real estate -1.8%, materials -1.9% communication -2.73%, tech-2.84%, health care -3.02%, and discretionary -3.79%.

Southbound Stock Connect volumes were high but slowly came back to earth though Mainland investors bought the dip today. Volume leader Semiconductor Manufacturing had buyers outpace sellers slightly while Tencent, Xiaomi and Meituan Dianping saw buyers outpace sellers by a higher margin. Mainland investors bought $847mm worth of Hong Kong stocks today as Southbound Connect trading accounted for 10% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen limited losses with a late afternoon rally to close -0.83% and -0.85% at 3,414 and 2,309, respectively. Volume edged higher +1.4% from yesterday to 2.5X the 1-year average while breadth was mediocre with 991 advancers and 2,784 decliners. Large, mid, and small caps were all off uniformly in a broad market correction. The Mainland stocks within the MSCI China All Shares Index were off -1.1% with communication +0.3%, utilities +0.16%, staples -0.22%, health care -0.49%, energy -0.8%, discretionary -1.05%, financials -1.13%, industrials -1.38%, materials -1.88%, real estate -1.94%, and tech -2.15%.

Northbound Stock Connect volume was high as foreign investors were net sellers of Mainland stocks. Growth stocks took the brunt of the selloff. Shanghai Connect volume leader Kweichow Moutai was sold 2.5X, China Tourism Group was sold by nearly 2 to 1, and Ping an was bought 1.5X. Shenzhen Connect volume leader Wuliangye Yibin saw sellers outpace buyers by more than 2 to 1, CATL 2 to 1, and East Money Information 8 to 7. Foreign investors sold $2.477B worth of Mainland stocks today as Northbound Stock Connect trading accounted for 5% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 7.01 versus 6.99 yesterday

- CNY/EUR 7.99 versus 7.95 yesterday

- Yield on 1-Day Government Bond 1.37% versus 1.27% yesterday

- Yield on 10-Year Government Bond 3.01% versus 3.06% yesterday

- Yield on 10-Year China Development Bank Bond 3.47% versus 3.54% yesterday