Mainland Market Correction, Semiconductor Manufacturing Wishes On A STAR (Market)

4 Min. Read Time

Key News

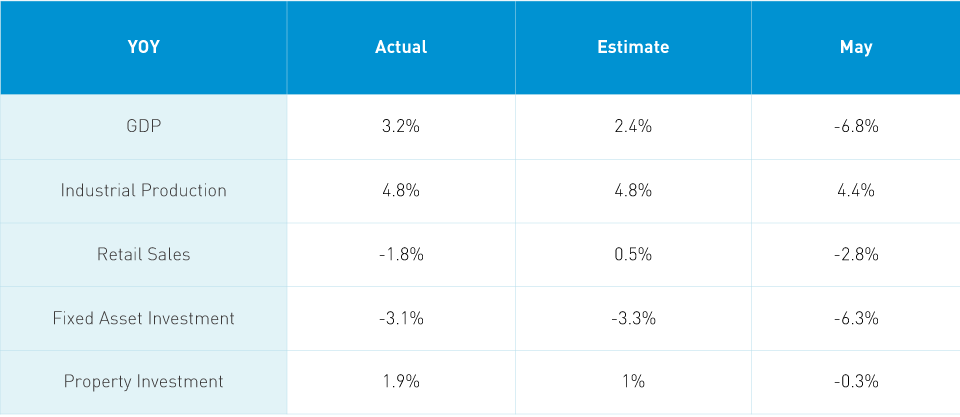

Asian equities had a mixed day as Hong Kong and Mainland China were off considerably. News going into the open looked positive as President Trump said he wouldn’t sanction Chinese officials, Mainland insurance companies were given the green light to invest in equities, and the Semiconductor Manufacturing International Corporation listed on the STAR Board, the Nasdaq of China. The economic data release came in better than expected, which led to some speculation that easing measures could be tempered. However, weaker than expected retail sales hit growth stocks and autos. If we look deeper, we can see that the retail sales picture was mixed by category and online retail sales were strong following June’s 618 sales event.

Takeaway: Industrial Production shows that China is experiencing a V-shaped rebound following a strong quarantine. This should give investors hope for our future. Retail sales were not as strong as I had hoped as restaurant dining fell -15.8%, jewelry -6.8%, furniture -1.4%, petroleum -13% and auto -8.2%. These losses offset gains in food +10.5%, beverages +19.2%, tobacco/alcohol +13.3%, cosmetics +20.5% and daily-used items +16.9%. It is worth noting that online retail sales +18.6% in June from May’s 14.7%. Foreign Direct Investment 7.1% versus May’s 7.5%.

The main catalyst for the correction was a WeChat post from Mainland media People’s Daily about bottles of Kweichow Moutai found to have been used in bribery cases. It wasn’t an accusation of the company, but it sparked a selloff as traders sold recent outperformers in Hong Kong and the Mainland. Since last week’s monumental rise, there have been rumors that the market had gone too far too fast as and officials began to talk it down. However, there is a lack of consensus among brokers. One noted the lack of panic while another felt the market has had a great few weeks and there is no such thing as a free lunch. Yet another broker felt that we could see another day or two of selling, but that investors are ready to use this weakness to establish positions after having missed the initial move in Hong Kong and the Mainland.

While the downturn is painful for people with portfolios like mine, the rationale for investing in China hasn’t changed at all. After all, the Mainland market has just broken out of a five-year basing period. We have been overdue for a correction, though today’s was a little strong. The Shanghai sliced through the 3,300 level sitting to near 3,200 while the Shenzhen is approaching 12,000. In Hong Kong, recent outperformers were all taken to the woodshed with Semiconductor Manufacturing -25%, Tencent -5.52%, Alibaba HK -4.19%, Meituan Dianping -7.73%, Xiaomi -7.82%, Geely Auto -11.98%, and HK Exchanges -5.72%. Why was Semiconductor Manufacturing’s Hong Kong stock off so much? Profit taking was cited along with investors gravitating to the Mainland share class, which pulled money out of many Hong Kong and Mainland tech stocks. In order to fund an IPO, you needed to get the cash from somewhere. Mainland China was a uniform drawdown as recent outperformers such as the DND trade, drugs (pharma) and drinks (alcohol), were hit along with brokers.

Semiconductor Manufacturing (688981 CH) listed on the Shanghai Stock Exchanges’ STAR Board last night. The stock gained +201% which was nowhere near my 1,000% prediction. I was “Just a bit outside” on that call. Volume was an incredible 552mm shares worth $6.856 billion. For comparison, US volume leader American Airlines traded 135mm in shares yesterday while the value of shares traded in Tesla was $24B.

Last night, I participated on a panel for the Shanghai Stock Exchange STAR Board conference. The panel was moderated by our friend Leon of China Securities Index Company. Leon and I have worked together to create an index based on Jon Krane’s vision of an ETF based on Chinese internet stocks that were benefitting from domestic consumption occurring online over seven years ago. It was great to “see” Leon and hear that his son is now eight years old. When we met in Shanghai, he was suffering from sleep deprivation as his then baby son kept him up at night. I’m feeling some sleep deprivation myself at the moment!

H-Share Update

The Hang Seng slumped -2%/-510 index points to close at 24,970, as volume jumped +21% from yesterday to nearly 2X the 1-year average. Breadth was terrible, with only 5 advancers and 43 decliners led by Tencent -5.5%/-157 index points, Hong Kong Exchanges -5.72%/-70 index points, and today’s worst performer Geely Auto, at -11.9%/-33 index points. Subway operator MTR Corp was the day’s best performer at +0.9%/+1 index point. Chinese domiciled companies were off -2.47% versus Hong Kong domiciled companies -1.72% using the HS China Enterprise and Hong Kong 35 indices as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares lost 4.2%, led by utilities -1.45%, financials -1.52%, energy -1.71%, real estate -2.38%, industrials -2.67%, materials -3.12%, staples -3.66%, communication -4.93%, health care -5.92%, discretionary -6.82%, and tech -10.01%.

Southbound Stock Southbound Stock Volumes were elevated in mixed trading as Shanghai Southbound had net selling and Shenzhen Southbound had net buying. Volume leader SMIC was sold on both, as was Meituan Dianping, while Tencent and Xiaomi were sold on one and bought on the other. Mainland investors bought $52mm of Hong Kong stocks today as Southbound Connect trading, which accounted for 12% of the Hong Kong stocks’ turnover.

A-Share Update

Shanghai & Shenzhen moved from upper left to lower right over the course of the trading day, down 4.5% and down 5.2% to close at 3,210 and 2,144, respectively. Mainland volume was off -6%, which is still more than 2X the 1-year average, while breadth was awful with 512 advancers and 3,274 decliners. Large, mid and small cap were off uniformly. The Mainland stocks within the MSCI China All Shares Index were down -5.15%, led by real estate -2.63%, financials -2.95%, energy -3.19%, utilities -3.28%, materials -3.78%, industrials -3.85%, communication -4.02%, discretionary -5.99%, health care -6.5%, tech -6.62%, and staples -8.02%.

Northbound Stock Connect volumes were very high as foreign investors sold Mainland stocks. Shanghai Connect volume leaders Kweichow Moutai and Ping An were sold by a small margin. Shenzhen Connect volume leader Wuliangye Yibin was sold 2.7 to 1.6, while Gree Electric Appliances was sold 3 to 1. Foreign investors sold -$989mm of Mainland stocks today as Northbound Connect trading accounted for 6% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 7.00 versus 6.99 yesterday

- CNY/EUR 7.99 versus 7.98 yesterday

- Yield on 1-Day Government Bond 1.59% versus 1.37% yesterday

- Yield on 10-Year Government Bond 2.95% versus 2.96% yesterday

- Yield on 10-Year China Development Bank Bond 3.46% versus 3.46% yesterday