Ant Group Marches To Hong Kong/STAR Board Listing

4 Min. Read Time

Key News

Asian equities had a choppy day as COVID-19 cases increased in Hong Kong and in the US over the weekend. While cases are important, the number of hospital admissions may be more relevant, since government leaders would raise lockdowns depending on hospital capacity. If anyone has a good source for hospital admissions, please let me know. While social distancing measures were raised in Hong Kong, I haven’t heard anything on hospital admissions.

Growth names had a mixed day as Hong Kong volume leaders were Semiconductor Manufacturing -2.76%, Tencent +0.29%, Meituan Dianping -1.41%, Ping An +1.71%, Alibaba Hong Kong +0.34% and Xiaomi +2.06%, JD.com Hong Kong +0.5%, and NetEase +0.57%. Materials had a strong day up 7%. Mainland China had a strong day as news that insurance companies can raise their equity allocations was widely viewed from the market that a healthy bull market is a good thing.

The DND trade, drugs (pharma) and drinks (liquor), took a breather today, while the Old Economy stocks were strong along with brokers on news of potential consolidation in the space. Foreign investors made an interesting move via Southbound Connect as Shenzhen (growth/mid small cap/private companies) saw outflows and Shanghai Connect (value/large cap/State Owned Enterprises) saw inflows.

I’ve spoken on the home bias of US investors by citing flows out of the three largest emerging market US listed ETFs; having to explain every quarter an underperforming asset class for ten years has led to an erosion or elimination in the stakes. The more investors diversified, the worse they did because it detracted from the potential size of their US equity position. The market usually does what is least expected. If the consensus is for US equity outperformance, wouldn’t an EM rebound along with commodities, another asset class that has been kicked to the curb with an equally poor ten year track record, shock investors? My thesis is supported from two independent sources: technical analyst Michael Oliver of Momentum Structural Analysis, and Hedgeye, a tactical/market research firm. While I don’t want to speak on behalf of Hedgeye nor MSA, one may want to check out their works.

Ant Group will list shares both in Hong Kong and on the STAR Board according to multiple media outlets, with a NYC bell ringing conspicuously absent. Remember Alibaba owns 33% of Ant, which is known for its Alipay digital payments platform. Media outlets didn’t mention the $200mm in investment banking fees lost to Hong Kong that would have served as a great stimulus for the New York metropolitan area had the company decided to list here. It is estimated that the company will be valued around $200 billion.

The Hong Kong listing will continue to solidify Hong Kong as a financial hub. A Mainland media source noted that Standard Chartered plans to add 1,600 employees in the Greater Bay Area within the next three years. Wealth Connect would allow mainland money to be invested in Hong Kong financial products. What’s next? MSCI China A Index futures in Hong Kong would be amazing in my opinion.

Hang Seng Indexes announced after the close that the Hang Seng TECH Index will be launched on July 27th. In taking a look at the potential index holdings, it is really a basket of Hong Kong listed growth companies, as the Global Industry Classification was amended in September 2018. Real estate was broken out as a stand-alone sector, while the technology sector was altered. Consumer tech plays such as Alibaba and Amazon were moved from technology to consumer discretionary while social media companies such as Facebook and Tencent were moved from technology to the new communication sector. The technology sector today is really semiconductors, hardware and software.

The launch is interesting because in mid-August, Hang Seng will announce if Alibaba, Xiaomi and Meituan Dianping will be added to the widely followed Hang Seng Index. China’s long running underperformance was due to large sector weights in Old China economic sectors. MSCI added US listed Chinese companies to its indexes in 2015/2016 with FTSE following shortly after. All of sudden, China’s performance picked up. I think the addition of growth names to the Hang Seng Index is a much bigger deal than this new index; down the road, we could see JD.com Hong Kong and NetEase Hong Kong added as well. With the service sector now 50% of China’s GDP, indices are becoming more reflective of the reality. Of course, some folks realized this a long time ago!

H-Share Update

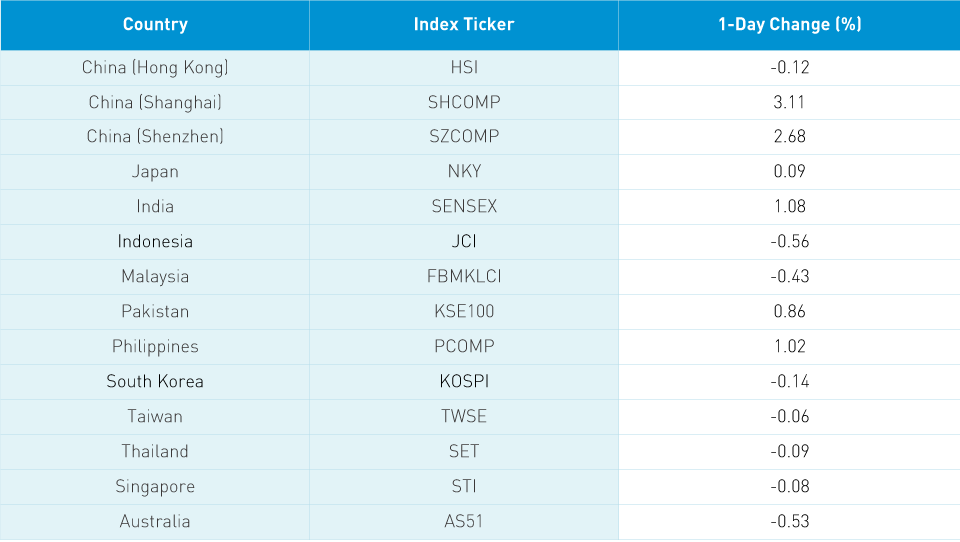

The Hang Seng fell out of the gate down -1.29%, but managed to climb back closing -0.12%/31 index points at 25,057. Volume was up +4.7% from Friday, which is 2X the 1 year average, while breadth was off with 16 advancers and 31 decliners. Today’s top performer was also the biggest index mover China Life gaining +8.32%/+36 index points, followed by Ping An +1.71%/+26 index points and HSBC -0.95%/-21 index points. Today’s worst performer was Wharf Real Estate Investment Company down -5.86%/-5 index points with several Macao gaming stocks nipping at its heels. Chinese domiciled companies outperformed Hong Kong domiciled companies +0.9% versus -0.9%. The 205 Chinese companies trading in Hong Kong within the MSCI China All Shares +0.95%, led by materials +7.63%, real estate +2.98%, industrials +2.77%, financials +1.67%, tech+0.96%, utilities +0.48%, energy +0.45%, communication +0.18%, health care +0.18%, discretionary -0.17%, and staples -1.17%.

Southbound Connect volumes have come down to pre-break out levels. Shanghai Stock Connect volume leader Semiconductor Manufacturing was sold, while Tencent was bought 2 to 1 and Xiaomi bought almost 5 to 1. Mainland investors bought $583mm of Hong Kong stocks today as Southbound Connect trading accounted for 12% of Hong Kong’s turnover.

A-Share Update

Shanghai & Shenzhen moved from lower left to upper right up +3.11% and +2.68% to close at 3,314 and 2,216, respectively. Volume was up +7% from Friday, which is just below 2X the 1 year average. Breadth was strong with 3,421 advancers and just 372 decliners. Large caps outperformed mid and small caps by a small amount. The 509 mainland listed stocks within the MSCI China All Shares were up +2.84%, led by materials +6.06%, industrials +5.05%, financials +4.39%, energy +3.94%, discretionary +3.62%, real estate +3.51%, tech +2.61%, communication +2.21%, utilities +2.15%, staples -0.05%, and health care -0.22%.

Shanghai & Shenzhen volumes are still above average as foreign investors pivoted away from the Shenzhen to Shanghai. In Shenzhen, foreign investors sold Wulliangye Yibin 3 to 2, Luxshare Precision sold 8 to 5, and CATL 2 to 1. On the Shanghai exchange, foreign investors sold Kweichow Moutai 3 to 2, Ping An 6 to 5, and China Tourism 3 to 2. Foreign investors sold -$844mm of mainland stocks today as Northbound Connect trading accounted for 7% of mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.99 versus 6.99 Friday

- CNY/EUR 7.98 versus 7.99 Friday

- Yield on 1-Day Government Bond 1.52% versus 1.57% Friday

- Yield on 10-Year Government Bond 2.93% versus 2.95% Friday

- Yield on 10-Year Government Bond 3.43% versus 3.45% Friday