US Action on China’s Houston Consulate Gives Asian Investors Pause

4 Min. Read Time

Key News

Asian equities were having a mixed day as Senator McConnell’s comments on further stimulus led to mixed sentiment. Then news that the US had ordered the closure of China’s Houston consulate sent stocks on a Thelma & Louise (off a cliff). The US had accused two Chinese individuals of trying to steal coronavirus research, so I suppose it is simply retaliation. I would certainly hope that the accusation is false as corporate espionage under the current political environment would be a big mistake. Several Chinese pharma names are very far along in clinical trials for a vaccine. Targeting the Houston consulate is very strange to me, as US energy companies have done very well in China with significant upside for US Liquified Natural Gas (LNG) producers.

In April of this year, Exxon Mobile began to build a $10 billion chemical plant in Huizhou, China. According to a Bloomberg article from April 22nd, “the ethylene cracker and down-stream production equipment” will generate $5.5B of operating income for the Irving Texas based company. While US farmers benefit from corn and soybean purchases, US LNG producers have significant opportunity in China due to China’s energy mix away from coal to LNG. As the NY Federal Reserve’s Liberty Street Economics research blog noted in a post titled “The Investment Cost of the U.S.-China Trade War”, sales by U.S. multinationals in China amounted to $376 billion in 2017 versus $130B of exports to China, while total sales from US firms in China were $505 billion. “46 percent of the 3,000 U.S. listed firms in our sample (which encompasses virtually all of U.S. market capitalization) were exposed to China through importing, exporting, or selling through subsidiaries, and the average firm obtained 2.3% of its revenue from China.” US equities can only ignore this for so long.

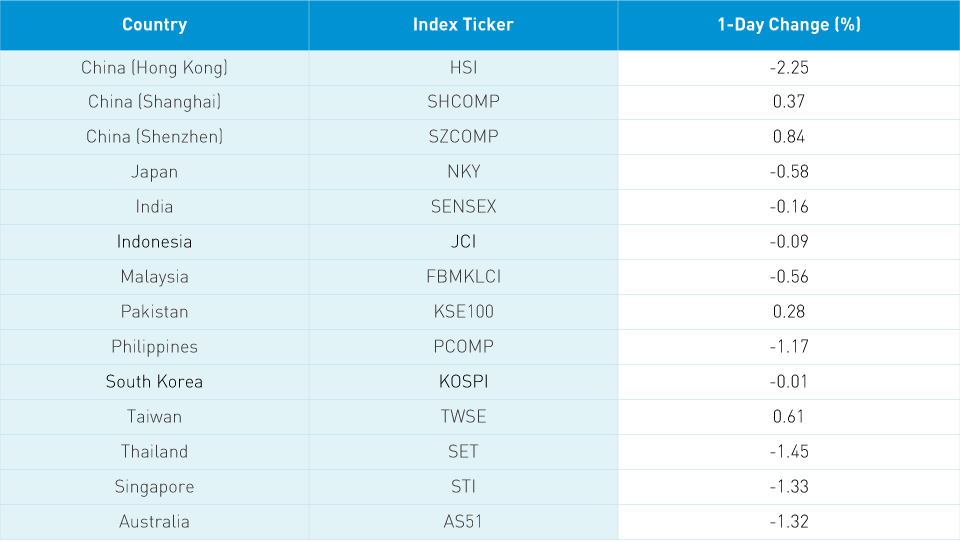

In Hong Kong, volume leaders were the growth names that have been performing well as Tencent -4.43%, Alibaba Hong Kong -3.5%, Meituan Dianping -6.24%, Semiconductor Manufacturing (SMIC) -8.01%, and Hong Kong Exchanges -4.95%. JD.com Hong Kong and NetEase were off -4.72% and -2.75%. iPhone suppliers were hit hard with Sunny Optical -3.5% and AAC Technologies -7.02%. Teledoc stocks Alibaba Health was down -4.42% and Ping An Healthcare -3.67%, despite recent government policies supporting the space. These growth names have performed well so the higher volatility is not surprising. Mainland Chinese markets had closed when the consulate news was released with Shanghai +0.37% and Shenzhen +0.84%. Growth names and the DnD trade fared well today.

Politico.com had a Tweet with comments from Senator John Kennedy, his effort to delist US listed Chinese companies was stalling because “Wall Street has unleashed hell lobbying against in the House, and that makes no sense to me”. Want to know what makes no sense to me? Jeopardizing $1.2 trillion of US savings during a recession! The action doesn’t hurt China but rather US investors, as evidenced by the SEC filings on who owns the stocks. You aren’t going to see Chinese names, but the largest US asset managers. Already the effort has led to US listed Chinese companies’ relisting in Hong Kong.

There are reports that Didi is denying its Hong Kong IPO though it is hard to deny the language used in the Caixin article referenced yesterday.

H-Share Update

The Hang Seng had a choppy session until the consulate news hit, when the index dived -2.25%, closing at 25,057. Volume was off -3.79%, though still 1.5X the 1 year average. Breadth was off with 4 advancers and 46 decliners led by Tencent -4.43%/-133 index points, Hong Kong Exchanges -4.95%/-65 index points and HSBC -2.4%/-65 index points. Apple supplier AAC Technology was the worst performer, down 7.02%/-7 index points, while China Petroleum & Chemical was the day’s best performer up +4.52%/+11 index points. Chinese domiciled companies were off -1.93% versus -2.21% for Hong Kong domiciled companies using the HS China Enterprise and Hong Kong 35 indexes as proxies. The 205 Chinese companies listed in Hong Kong within the MSCI China All Shares were down -2.78%, led by energy +2.18%, utilities +0.26%, materials -0.97%, staples -0.99%, industrials -1.13%, health care -1.26%, financials -1.64%, real estate -2.96%, communication -4.09%, discretionary -4.61%, and technology -5.08%.

Southbound Stock Connect volumes continue to moderate though the buying continued. Volume leader SMIC saw more sell trades than buys, but not by much, while Tencent was bought 4 to 4 on Shanghai and 5 to 1 on Shenzhen. Mainland investors can choose via Shenzhen or Shanghai Connect with each venue posting their own trade data. Unfortunately, it is aggregated into one line item. Exchanges make a lot of money selling data. Mainland investors bought $436mm of Mainland stocks today as Southbound Connect trading accounted for 9% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen had a choppy session, coming off the day’s high closing +0.37% and +0.84% closing at 3,333 and 22,51, respectively. Volume was up +7%, which is a touch below 2X the 1-year average. Breadth was positive with 1,901 advancers and 1,704 decliners as mid and small cap outperformed large caps. The 509 Mainland stocks within the MSCI China All Shares gained +0.63%, led by tech +1.25%, health care +1.25%, materials +1.12%, discretionary +1.02%, staples +0.94%, energy +0.93%, communication +0.49%, industrials +0.01%, financials -0.02%, real estate -0.22%, and utilities -0.3%

Northbound Stock Connect had high volumes which is the new normal, though we saw a reversal of yesterday when Shanghai had net buying and Shenzhen net selling. Today, Shenzhen had robust buying while Shanghai was sold slightly. On the Shanghai, volume leader China Tourism was sold 15 to 9, Kweichow Moutai sold 4 to 3, and Ping An sold 13 to 8. On the Shenzhen, volume leader Gree Appliances was bought 17 to 4, Luxshare bought 5 to 4, and Wuliangye Yibin sold 10 to 7. Foreign investors bought $596mm of Mainland stocks today as Northbound Connect trading accounted for nearly 7% of Mainland turnover. Week to date foreign investors have sold -$679mm of Mainland stocks. YTD foreign investors have bought $21.63B of Mainland stocks.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.99 versus 6.98 yesterday

- CNY/EUR 8.11 versus 8.02 yesterday

- Yield on 1-Day Government Bond 1.32% versus 1.27% yesterday

- Yield on 10-Year Government Bond 2.89% versus 2.90% yesterday

- Yield on 10-Year China Development Bank Bond 3.36% versus 3.38% yesterday