Markets Recover Post US-China Political Rhetoric Turns from Bark to Nibble

5 Min. Read Time

Key News

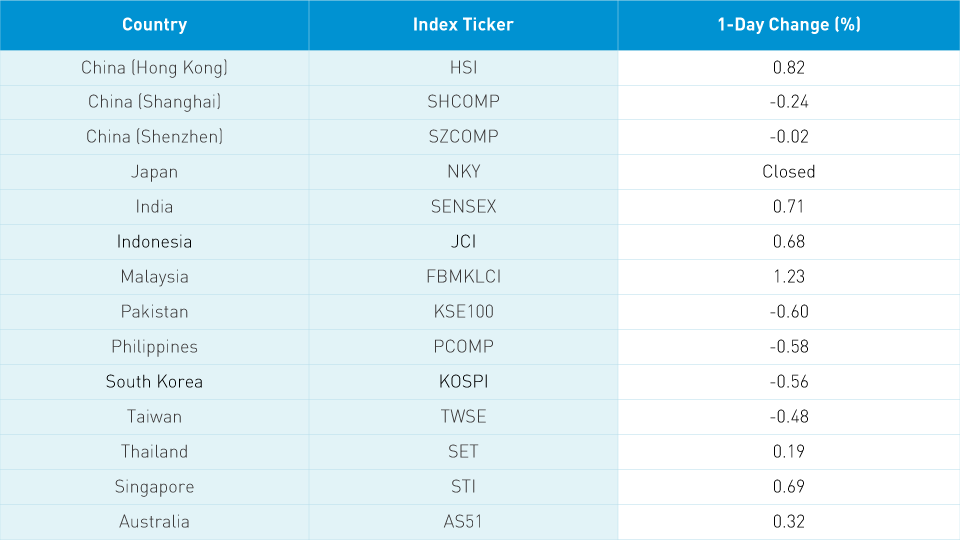

Asian equities were largely higher despite rising US-China political tensions, as China would retaliate by closing the US consulate in Chengdu. There was chatter that China chose Chengdu over Wuhan, which is China’s Detroit (i.e. auto manufacturing hub). Closing the Wuhan consulate would have been a big blow to US auto manufacturers such as GM, which manufactured and sold 462,000 vehicles in China in Q1 through joint ventures with SAIC versus 618,000 in the US.

Hong Kong managed to gain as investors scooped up growth stocks following yesterday’s carnage. Volume leader Tencent gained +3.34%, Alibaba Hong Kong -0.56%, Semiconductor Manufacturing (SMIC) +2.59%, Meituan Dianping +3.54%, Hong Kong Exchanges +4.04% and AAC Technologies gained +12.92%, following an analyst upgrade and an investment from investors, including mobile phone manufacturers Xiaomi and Oppo. JD.com Hong Kong was off -0.25%, while NetEase Hong Kong was up +0.48%.

Healthcare stocks were strong as a government official noted the strong progress from Chinese pharma companies, as a vaccine is expected by year end. Let’s hope so! Ping An was off -0.29%, despite news online that wealth manager Lufax, which Ping An invested in, is seeking a US IPO this year. The Mainland overcame morning lows of -2.26% and -2.69% on the Shanghai and Shenzhen to close basically flat. Healthcare stocks had a strong day as did brokers, despite weakness in banks. A Mainland news source noted that Tesla’s wait period in China is down to two weeks as production ramps up.

Last week I participated in a panel with Mark Mobius, who is rightfully credited with putting emerging market investing on the map. Mr. Mobius and I had a great conversation on China and EM guided by a great moderator from Latin America’s largest Investment Bank. It was an incredible validation to have my views agreed upon by the investing legend who is now running an EM ESG investing firm. In speaking about ESG investing, I noted that many companies that have a founder who is a CEO can have low governance scores because they own more shares than investors or because they retain voting rights. This is true for US and China tech/internet/e-commerce companies. I believe owning the same shares as the founder/CEO is a good thing as our interests are aligned. Mr. Mobius noted that he had just read a white paper which proved that out. In using Google, I believe I found the referenced paper by Rudiger Fahlenbrach of Ecole Polytechnique Federale de Lausanne from the Journal of Financial and Quantitative Analysis. In looking at US publicly traded companies founder/CEO companies, the paper, which you have to pay to read, seems to insinuate that these companies do indeed outperform. Hat tip to Mr. Mobius!

Nick Wadhams and Peter Martin of Bloomberg News wrote an exceptional article titled “China Consulate Fight Shows Trump’s Hardliners Are in Charge”. The article provides insight into the rise of China hardliners led by Secretary of State Mike Pompeo and Deputy National Security Advisor Matthew Pottinger, who view China’s rise as a threat to the US. The article reminded me of the great book “Team of Rivals: The Political Genius of Abraham Lincoln” by Doris Kearns Goodwin. President Lincoln hired his primary rivals in his cabinet in order to bring diverse opinions and debate to policy. The lack of China bulls in DC worries me, as we may learn a very harsh lesson from Economics 101. Tariffs are inflationary as China doesn’t write a check, but US consumers pay more for goods. More worrisome is the reality that US multi-nationals are doing very well in China, as we noted yesterday at length. There are 4 billion potential buyers of US goods in Asia. Where would you put a factory? We have had a lot of bark but little bite to US-China political rhetoric, but the US closing China’s Houston consulate is a nibble. If US business interests don’t step up to counter or at a minimum balance this new trend, their operations, investments and China opportunity will be at risk. That would be very bad news for the S&P 500 and a Q3 economic rebound. More worrisome to me is the world that my kids will grow up in.

UBS Global Research upgraded China’s 2nd half 2020 GDP to 5.5% - 6% year-over-year (YoY). UBS has great China research, having attended their China conference in Shanghai in early January. The rebound will be driven as “domestic consumption recovers to positive territory and property and infrastructure investment remains strong.” A CICC research noted that June online retail sales grew nearly 30% year over year while offline retails contracted -10% YoY. The service sector is now more than 50% of China’s GDP. As investors, we should all take notice.

H-Share Update

The Hang Seng traded in a tight range up +0.82%/+205 index points to close at 25,263. Volume was off -9%, which is still above the 1-year average though not by much, while breadth was off with 22 advancers and 27 decliners. Heavyweights pulled the index higher, led by Tencent up +3.35%/+103 index points, Hong Kong Exchanges +4.04%/+55 index points and AIA Group +1.25%/+32 index points. Today’s best performer was AAC +12.9%/+15 index points, while Wharf Real Estate was off -3.41%/-3 index points. Chinese domiciled companies listed in Hong Kong were up +0.8%, while Hong Kong domiciled companies were up +0.65%. The 205 Chinese companies listed in Hong Kong within the MSCI China All Shares were up +1.71%, led by healthcare +3.26%, discretionary +3.19%, tech +3.15%, Staples +3.12%, communication +2.82%, real estate +0.69%, materials +0.13%, industrials +0.1%, utilities -0.14%, financials -0.26%, and energy -0.71%

Southbound Connect volumes declined again, though Mainland investors’ appetite for Hong Kong listed stocks continues. SMIC was sold again, while Tencent and Xiaomi were bought. Mainland investors bought $467mm of Hong Kong stocks today as Southbound Connect accounted for 11% of Hong Kong’s turnover

A-Share Update

Shanghai & Shenzhen overcame a morning fall of -2.26% and -2.69% to close -0.24% and -0.02% at 3,325 and 2,250 respectively. Volume was up +5% from yesterday, which is nearly 2X the 1-year average, while breadth was off with 1,071 advancer and 1,653 decliners. Large caps underperformed mid and small caps. The 509 Mainland stocks within the MSCI China All Shares were down -0.01%, led by healthcare +2.21%, discretionary +1.55%, industrials +0.55%, staples +0.21%, materials -0.2%, utilities -0.4%, tech -0.73%, financials -0.85%, energy -1.33%, communication -1.6%, and real estate -1.84%.

Northbound Stock Connect volumes were elevated again, similar to yesterday when Shenzhen Connect was bought while Shanghai Connect was sold. On Shanghai Connect, China tourism was sold 11 to 8, Kweichow Moutai sold 11 to 7, and Jiangsu Hengrui Medicine sold 5 to 4. On the Shenzhen, Luxshare Precision was bought slightly, Wuliangye Yibin sold nearly 2 to 1, and East Money Information bought 3 to 2. Foreign investors sold -$521mm of Mainland stocks today while Southbound Stock Connect accounted for nearly 7% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 7.01 versus 7.00 yesterday

- CNY/EUR 8.12 versus 8.11 yesterday

- Yield on 1-Day Government Bond 1.34% versus 1.32% yesterday

- Yield on 10-Year Government Bond 2.91% versus 2.89% yesterday

- Yield on 10-Year China Development Bank Bond 3.39% versus 3.36% yesterday