Political Rhetoric Clips Stocks, Week In Review

4 Min. Read Time

Week in Review

- It was confirmed on Monday that Ant Group will list shares both in Hong Kong and on the STAR Board, with a NYC bell ringing conspicuously absent.

- On Tuesday, Caixin, a Mainland media source, reported that Didi Chuxing is going to go public in Hong Kong. However, Didi denied this on Wednesday.

- On Wednesday, news that the US had ordered the closure of China’s Houston consulate sent stocks lower.

- CICC research noted on Thursday that June online retail sales grew nearly 30% year over year while offline retail contracted -10% YoY. The service sector is now more than 50% of China’s GDP. As investors, we should all take notice.

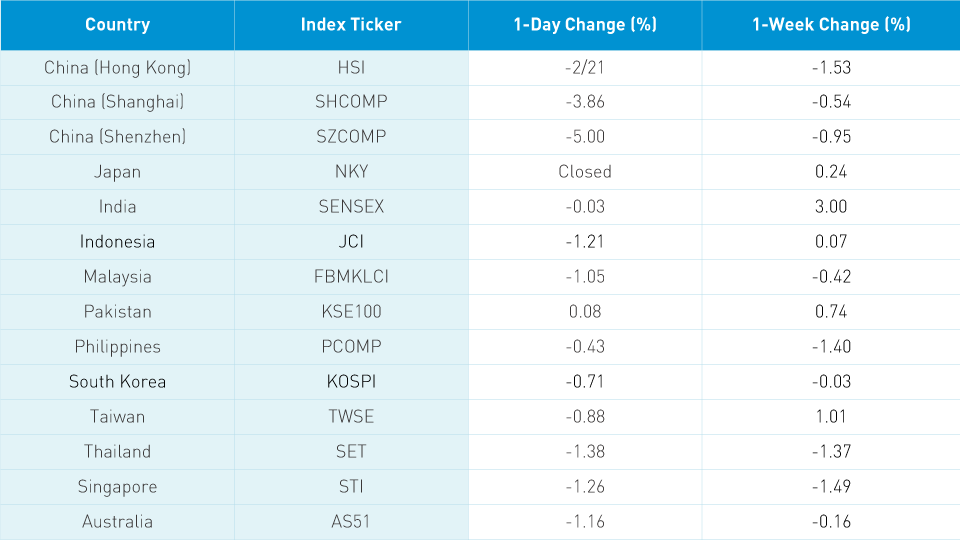

Friday's Key News

Asian equities were mostly lower as China retaliated by closing the US consulate in Chengdu. My one recommendation for if politicians want higher US equities: more Mnuchin/Kudlow and less Pompeo. Reuters reported in an article titled “U.S. diplomats head to China despite row over Houston consulate” that “a flight bound for Shanghai carrying U.S. diplomats has left the United States…”. There is little knowledge of who is on the flight nor their objectives, but maybe the Pompeo speech is another instance of bark over bite. Intel’s production delays that were reported after the US close didn’t help tech stocks regionally.

Hong Kong and Mainland China were off worse on the deteriorating rhetoric, which led to a sharp de-risking and profit taking. Hong Kong continues to battle a flare up in coronavirus cases by tightening social distancing measures. Hong Kong growth names took the brunt of the selling as volume leaders Tencent was down -5.21%, Alibaba Hong Kong -3.08%, Semiconductor Manufacturing -7.4%, Meituan Dianping -4.17% and Hong Kong Exchanges down -4.1%. JD.com Hong Kong was off -2.81% and NetEase Hong Kong was off -3.84%.

Mainland China was hit hard, as outperformers such as brokers and DnD stocks (drug/pharma and drinks/alcohol) fell. Out of 2,440 stocks within the Shanghai & Shenzhen Composite Indices, only 284 stocks were in the green today. Not helping is the expiration of the 1-year STAR Board lock ups, as investors took the STAR index down -7%. According to Mainland media source, it is estimated $1.3B could be sold as the first 25 companies’ lock up expires. Foreign investors took part in the profit taking, selling a healthy $2.3B of Mainland stocks via the Northbound Stock Connect program.

Corrections are healthy and to be expected. The reality is that the Mainland market has broken out of a five-year base, as it is apt to consolidate here. The global growth versus value trade has become a bit extended. Political rhetoric is apt to worsen going into the election, though politicians may notice how they are tanking the market (at least we should hope so). China’s economy continues to rebound as we head into Q2 earnings season for US listed Chinese companies. For this week, the Shanghai & Shenzhen were off less than 1%. Doesn’t it feel worse though? The headlines are so bad, but the reality is that markets didn’t move much. At least that is what I’m telling myself today!

CNY was off slightly, depreciating versus the dollar and euro, while Chinese bonds rallied in a risk off day. Many traders watch CNY as indicator of market sentiment, so the move was very small. Chinese 10-Year Treasury Yield has fallen from a mid-July high of 3.05% to 2.85% as the recent risk off led to quick bond rally.

A Mainland media source reported that Alibaba’s international/non-China e-commerce saw a +80% increase in transactions in the 1st half of this year. Leading destinations were the US, UK and Germany followed by a number of Asian countires. According to Bloomberg, International Commerce accounted for 7.4% of Alibaba revenue.

How great is it to have baseball back?

H-Share Update

The Hang Seng went from upper left to lower right down -2.21%/-557 index points to close at 24,705. Volume jumped 18%, which is more than 1.5X the 1-year average. Breadth was awful with only 5 advancers and 43, led by Tencent -5.21%/-153 index points, Hong Kong Exchanges -4.1%/-53 index points, and HSBC -1.5%/-33 index points. Today’s worst performer was Sino Biopharma -8.64%, while PetroChina was the day’s best performer up +2.14%. Hong Kong domiciled stocks were off -2.04% versus -2.37% for Chinese domiciled stocks using the HS 35 and China Enterprise indexes as proxies. The 205 Chinese companies listed in Hong Kong within the MSCI China All Shares were off -3.53%, led by energy -0.67%, utilities –1.36%, financials -2.19%, industrials -2.25%, industrials -2.25%, real estate -2.66%, materials -2.82%, staples -3.24%, discretionary -3.49%, communication -4.49%, tech -5.11%, and health care -6.53%.

Southbound Stock Connect volumes were moderate in mixed trading. On Shanghai Southbound Connect, volume leader Tencent was sold 2 to 1, SMIC 2 to 1, and Meituan Dianping sold 3 to 1.

A-Share Update

Shanghai & Shenzhen collapsed -3.86% and -5% closing at 3,196 and 2,138, as volume increased +7% to nearly 2X the 1-year average. Breadth was beyond awful, with only 284 advancers and 3,454 decliners. Mid and small caps were off more than large caps. The 509 Mainland stocks within the MSCI China All Shares lost -4.88%, led by energy -2.4%, utilities -2.65%, real estate -3.15%, industrials -4.33%, financials -4.36%, staples -4.54%, materials -4.7%, communication -5.28%, tech -5.82%, health care -6.26%, and discretionary -6.39%.

Northbound Stock Connect volumes were high or the ‘new normal’, as foreign investors sold Mainland stocks. On the Shanghai, volume leader Kweichow Moutai was sold 2 to 1, Ping An sold 4 to 3, and China Tourism sold 3 to 2. On the Shenzhen, volume leader Wuliangye Yibin sold 3 to 2, Gree Electric Appliances sold 2 to 1, and CATL sold nearly 3 to 1. Foreign investors sold $2.331B of Mainland stocks today.

Last Night’s Exchange Rates & Yields

- CNY/USD 7.02 versus 7.00 yesterday

- CNY/EUR 8.15 versus 8.12 yesterday

- Yield on 1-Day Government Bond 1.32% versus 1.34% yesterday

- Yield on 10-Year Government Bond 2.86% versus 2.91% yesterday

- Yield on 10-Year China Development Bank Bond 3.33% versus 3.39% yesterday