Mainland Moves Higher on Positive Caixin PMI Manufacturing Release, HSBC Weighs on Hong Kong

5 Min. Read Time

Key News

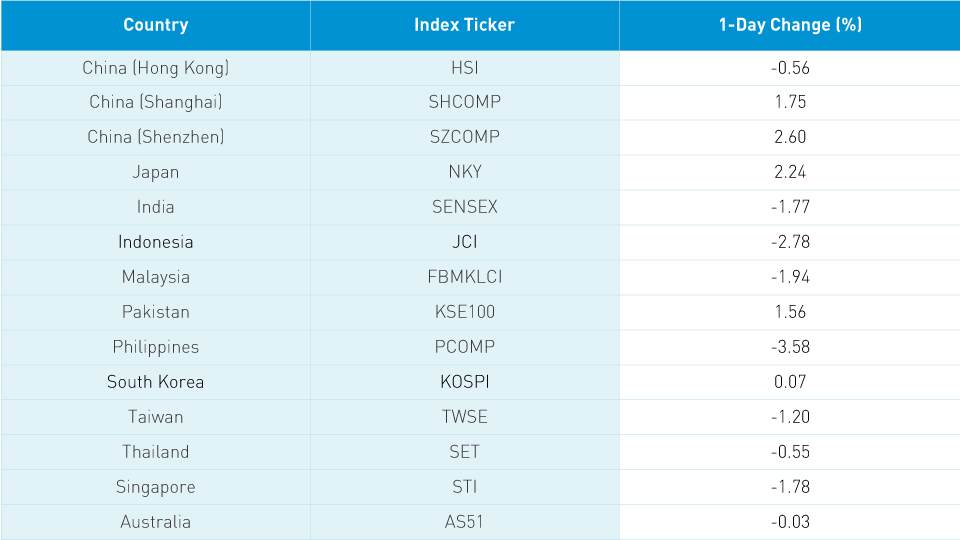

Asian equities had a poor start to the week as coronavirus flare ups in Hong Kong, Australia, and the Philippines along with US-China political rhetoric weighed on sentiment. However, growth names held up relatively well as evidenced by South Korea’s Kosdaq rising +1.5% versus the Kospi’s gain of only +0.07%. Hong Kong stocks, which historically have been foreign investors’ definition of China, were off on the above as well as HSBC’s noon earnings release, which came in well below conservative estimates as pre-tax profit slumped 65% in the first half of 2020. I’m not advocating for the stock, but I believe an activist investor will buy a piece of it and demand that the bank split its China/Hong Kong, Europe, and US businesses apart though this is pure speculation on my part. Growth stocks in Hong Kong were led by volume leaders Tencent, which gained +0.94%, Meituan Dianping +4.53%, Semiconducor Manufacturing +4.86%, and Alibaba HK -0.16%. Haier Electronics Group jumped +7.45% while JD.com HK rose +2.66% and NetEase HK +1.6%.

The big news over the weekend was talk that ByteDance will sell its US unit TikTok to Microsoft. My thoughts: 1) With all of the issues domestically, why are dancing teenagers our priority? This is a distraction technique: “look over there and not here.” 2) I can’t remember the government previously forcing a divestment of this scale. However, the AT&T break up in the 1980s comes to mind. 3) ByteDance’s private equity investors, which include KKR and General Atlantic, won’t be happy. China-based PE firm Primavera Capital Group head Fred Hu was recently quoted in a Reuters article as saying “Bytedance is an innocent victim of the mad politics and mad geopolitics. It is a sad outcome for Bytedance, for entrepreneurial capitalism, and for the future of global commerce”. I couldn’t have said it better myself. US pension funds, endowments, and foundations were large investors in PE in the early 2000s, some which went into China and yielded huge winners such as Alibaba and Tencent. Institutional investors’ views of China, which are largely informed by their success in the market through private investments, are mostly positive. Regardless, and as Mr. Hu notes in his statement, the PE firms will sue in US courts to stop the forced sale.

While negative sentiment weighed on Hong Kong, the Mainland was, as Sammy Haggar sang in the Van Halen song Dreams, “higher and higher.” The positive Caixin PMI release along with constructive comments on the economy from policy makers both helped lift stocks on the Mainland. Brokers were strong along with health care and space-related stocks as China’s Mars mission passed a critical juncture. A Mainland broker noted that Secretary of State Pompeo’s statement on targeting Chinese software stocks lifted the sector as investors believe that policy will support the sector if it falls further under US scrutiny.

Takeaway: The release occurred at 9:45am locally sending mainland Chinese stocks higher in the strongest monthly reading since 2011. I recognize there can be some skepticism regarding Chinese economic data, but the Caixin survey is conducted by the London-listed IHS Markit. The Caixin survey differs from the “official” PMIs in that it focuses on private medium and small companies while the “official” PMI focuses on large companies, many which are government affiliated. The Caixin survey is a much smaller survey of approximately 500 firms versus 5,000 for the “official” PMI survey, making it more volatile. PMIs are diffusion indexes. Readings above 50 show growth month over month and readings below 50 show declines. Today’s Manufacturing PMI showed a robust rebound in China’s economic activity as domestic demand exceeded foreign demand, which led to a drop in inventories and a rise in new orders. The reading highlights the rebound in China domestically. However, China is decidedly not immune to the economic consequence of global quarantines. Employment has been weak as many export-driven manufacturers’ customers are experiencing Q2 economic slumps. Ultimately, the employment data proves we are a global economy.

Asian investors reacted to an article on increased institutional investor interest in China. The statistic that jumped out to me was a quote from Adrian Chan of institutional consultant Willis Towers Watson, who feels that foreign ownership of Chinese A Shares would rise from 3% today to 10% within the decade based on MSCI’s inclusion of Chinese A Shares in their leading indexes. I agree. However, I would point out that MSCI has a very specific definition of Chinese A Shares comprised of 473 stocks. Do your homework on index construction as MSCI’s definition of A Shares has outperformed the CSI 300 by 5% year to date.

Bilibili (BILI US) announced last night that it will become the exclusive broadcaster of the League of Legends tournaments in China in a deal with Riot Games, a Tencent subsidiary. Finding my kids playing video games on a beautiful day still sets me off. But, finding my kids watching someone else play video games really blows my top. Yes, watching someone else play video games is a thing and E-Sports, the term used for the burgeoning spectator sport, is big business. League of Legends is, by far, the most popular video game in China with an estimated +100mm active players globally and tournaments drawing arena-sized crowds and millions of dollars in prize money. We wrote about this in a piece titled “China’s Digital Athletes: Q3 China Internet Sector Earnings Report” if you want to explore the trend further and feel old.

H-Share Update

The Hang Seng traded in a narrow range closing -0.56%/-137 index points at 24,458. Volume was up +9.5% from Friday, which is above the 1-year average. Meanwhile, breadth was off with 13 advancers and 36 decliners. The index was led south by HSBC -4.43%/-91 index points, Tencent +0.94%/+28 index points, and AIA -1%/-24 index points. China-domiciled companies were off -0.07% versus -0.64% for Hong Kong-domiciled companies using the HS China Enterprise and HK 35 indexes as proxies. The 205 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index rose +0.81% with discretionary +2.81%, materials +2.62%, tech +2.03%, industrials +1.52%, communication +0.96%, health care +0.86%, staples +0.04%, financials -0.21%, real estate -0.52%, utilities -0.56% and energy -0.56%.

Southbound Stock Connect, the trading platform that allows Mainland investors to buy Hong Kong-listed stocks, saw decent volumes as Mainland investors were net buyers of Hong Kong stocks. We can take the buy volume and subtract the sell volume to tell whether investors were net buyers or sellers not only for the broad market, but also for individual stocks. Shanghai Southbound Connect volume leader SMIC saw buyers outpace sellers by a small margin, Tencent was bought 2 to 1, and Meituan Dianping was bought 4 to 1. Mainland investors bought a healthy $607mm worth of Hong Kong stocks today as Southbound Connect trading accounted for 11% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen opened higher and kept rising to close +1.75% and +2.6% at 3,367 and 2,315, respectively. Volume jumped +16.9% from Friday to nearly 2X the 1-year average while breath was an unbelievable 3,383 advancers and 342. Mid and small caps outperformed large caps by ~1%. The 510 Mainland Chinese stocks within the MSCI China All Shares Index gained +1.66% with tech +3.01%, industrials +2.46%, health care +1.79%, communication +1.78%, real estate +1.77%, discretionary +1.73%, materials +1.5%, energy +1.37, financials +1.33%, utilities +0.39%, and staples +0.37%.

Northbound Stock Connect, the trading platform that provides foreign investors with access to Mainland stocks, had decent volumes as Shanghai Connect had selling pressure while Shenzhen Connect had buying pressure. Volume leaders on Shanghai Connect was China Tourism were sold a little more than 2 to 1, Kweichow Moutai had buyers outpace sellers by a small amount, and Ping An was sold by 5 to 4. Shenzhen Connect volume leaders were Luxshare, which was sold 2 to 1, Walvax Biotechnology, which was bought 8 to 5, and Gree Electric Appliances was also bought 8 to 5. Selling in Shanghai stocks outpaced the buying in Shenzhen stocks today by a small amount, which led to a net sale of -$27mm. Northbound Connect trading accounted for nearly 6% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 6.98 versus 6.98 Friday

- CNY/EUR 8.25 versus 8.19 Friday

- Yield on 1-Day Government Bond 1.47% versus 1.40% Friday

- Yield on 10-Year Government Bond 2.95% versus 2.97% Friday

- Yield on 10-Year China Development Bank Bond 3.48% versus 3.48% Friday