“ATMX” (Alibaba, Tencent, Meituan Dianping, and Xiaomi) Shine in Hong Kong Despite TikTok “Smash and Grab”

6 Min. Read Time

Key News

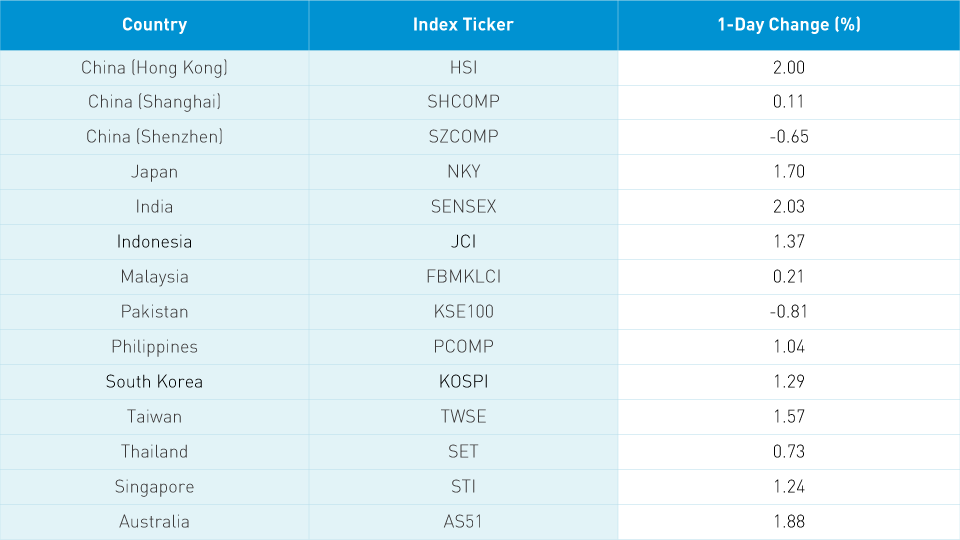

Asian equities rebounded overnight as Nasdaq reached a new high yesterday in the US. Hong Kong rebounded 2% as new coronavirus cases fell locally day over day, as growth stocks led the volume leader board with Tencent up +2.04%, Meituan-Dianping +8.67%, Alibaba Hong Kong +3.34%, followed by Ping An +2.03%, Semiconductor Manufacturing (SMIC) -2.56%, HSBC +0.75% and Xiaomi +3.2%. JD.com Hong Kong was up +1.94% while NetEase Hong Kong +2.23%. One local broker reported that Ant Group’s Hong Kong and STAR Board IPO could come as early as September in explaining Alibaba Hong Kong’s strength, as Alibaba owns 1/3 of the largest fintech unicorn globally.

Overnight, the 2020 Hurun Global Unicorn List was released in the Mainland, marking Ant Group as the highest valued unicorn, globally valued at $150B, followed by ByteDance at $80B and Didi Chuxing at $55B. 6 of the 10 largest unicorns are Chinese companies according to the report, with four companies from the US making list. It is worth noting that financials and real estate names had a strong day in Hong Kong, as China Construction Bank was up +2.64% as its dividend yield hit 6%. The Mainland diverged with growth stocks taking a breather on profit taking, as financials rose despite brokerages’ weakness. The DnD trade (drugs ie. pharma and drinks ie. alcohol stocks) were off as profit taking hit health care, tech and communication sectors, though fiery liquor provider Kweichow Moutai managed a small gain +0.12%.

Northbound Stock Connect, the trading venue for foreign investors to access Mainland stocks, saw inflow into Shanghai listed stocks (large cap, value oriented stocks) while Shenzhen listed stocks (mid/small cap, growth oriented stocks) saw net selling. One day doesn’t make a trend nor a change in trend. The Caixin China PMI Services is expected to be released today with expectations very high for a 58 print.

President Trump’s continued effort to force a sale of ByteDance’s non-China business unit TikTok went from strange to bizarre, as he said that the US Treasury should get a cut of the company. There was little coverage of TikTok in Mainland media sources, other than an editorial in China Daily, which is garnering a lot of attention here as it called the tactic a “smash and grab”. Cnet.com has a good article questioning the legality of the move, quoting Electronic Frontier Foundation general counsel Kurt Opsahl “there is no law that would authorize the federal government to ban ordinary Americans from using an app.” The article notes that the US could put TikTok on the entity list, which is around technology purchases but that move wouldn’t hold up in US court, since ByteDance developed its technology independently. The article quotes a New York Times article published on July 15th 9updated August 3rd) that a ban could be done under the International Emergency Economic Powers Act which is usually used during war time. If that doesn’t give you pause I don’t know what well.

My colleague Fernando highlighted an article written by Google Ventures’ General Partner M.G. Siegler on 500ish.com in which he speaks to the issue of TikTok’s technology comes from ByteDance, raising doubts on what Microsoft would actually be buying. Ultimately, we are in uncharted territory with a multitude of unintended consequences. We know that the distraction technique such as last week’s absentee ballot announcement completely removed the US GDP print from the headlines. Maybe it’s simply retribution for TikTok users messing with the Tulsa rally. I think this is all bark and no bite, as the lawyers will have a field day as US PE firms go to bat on behalf of their investors to protect their investments. Ultimately TikTok, which has a solid management team of Westerners, will get spun off from ByteDance. The whole thing is a waste of time, especially in light with what is happening in the world today.

My colleague Leo shared a Mainland article on new security accounts openings in China. According to the article, the number of new brokerage accounts in China grew +8.72% to 167mm with 1.5mm new accounts in June, which is 46% year over year. China’s population is 1.4B with a labor force of approximately 800mm. 167 divided by 800 means that only 20% of Chinese adults have a brokerage account. According FINRA, 33% of US households own a taxable brokerage account (another 29% hold a retirement account such as 401k, IRA or pension). Is China’s number going higher or lower over the next decade? My guess is up. Only 4% of Chinese household wealth is in stocks and mutual funds versus 23% in stocks and 6% in mutual funds in the US according to CICC data. Two thirds of Chinese wealth are in housing which the government has repeatedly said over the last year is for living in and not speculating. If housing prices flatten, even a small increased allocation into stocks will have a real effect. There is evidence to suggests it is occurring.

Bond Connect is the fixed income trading platform that allows foreign investors access into China’s Mainland bond market. In July, foreign investors bought $10.8B (RMB 75.5B) of Mainland bonds. There are just over 2,000 Bond Connect customers from 33 countries, including 72 of the top 100 global asset managers. Virtually all of the trading is in Chinese Treasuries and policy banks at 89%. A 10-Year Chinese Treasury currently yields 2.94% versus 0.56% for a US 10-Year Treasury. China’s yields look great relative to developed markets with Iceland the only developed market with a 10-Year government bond above 1% at 2.52%. Compared to EM local bonds, China isn’t as high, but the currency is one of the most stable, with a volatility of just 4.15 over the last year versus the Euro’s 7.0, Japanese Yen’s 9.18, and British Pound’s 10.9. I’m not advocating anyone plow their retirement into Chinese bonds, but real capital is going into the world’s second largest bond market.

Yesterday, the Hong Kong Exchanges listed eight more MSCI benchmarked futures. MSCI and Hong Kong Exchanges signed an agreement to list 37 MSCI benchmarked futures in May which was a significant blow to the Singapore Exchange. Not included in the 37 was a MSCI China A Index futures though the market anticipates the 38th futures will be it. Fingers crossed that it would eliminate one of the hurdles for MSCI to up their definition of Chinese A Shares in broader indexes such as Emerging Markets.

Earnings season for Chinese internet and e-commerce companies kick off in earnest next Monday.

H-Share Update

The Hang Seng opened traded slightly higher in the morning session before powering higher in the afternoon +2%/+488 index points to 24,946. Volume was up +11.9% from yesterday to +1.5X the 1-year average while breadth was strong with 44 advancers and just 4 decliners. Index heavyweights led the way AIA +4.11%/+104 index points, Tencent +2.04%/+62 index points and China Construction Bank +2.64%/+50 index points. Hong Kong domiciled stocks outperformed Chinese domiciled stocks +2.07% versus +1.7% using the HS Hong Kong 35 and China Enterprise Indexes as proxies. The 205 Chinese companies listed in Hong Kong within the MSCI China All Shares were up +2.05 %, led by discretionary +5.64 %, financials +2.46 %, communication +1.87 %,, energy +1.83 %,, real estate +1.17 %, tech +0.96 %, industrials +0.78 %, health care +0.71 %, utilities +0.64 %, staples +0.1 %, and materials -0.26 %.

Southbound Stock Connect, the trading for Mainland investors to buy Hong Kong listed stocks, had modest volumes, with buyers’ volume exceeding sellers’ volume by a small amount. Shanghai Connect volume leaders were SMIC sold slightly. Tencent sold 1.5 to 1 and Meituan Dianping bought 2 to 1. Mainland investors bought $442mm of Hong Kong stocks today as Southbound Connect trading accounted for 9% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen diverged in a choppy session up +0.11% and down -0.65% to close at 3,371 and 2,300 respectively. Volumes +3.6% to nearly 2X the 1-year average, while breadth was mixed with 1,353 advancers and 2,308 decliners as large caps outperformed mid and small caps. The 510 Chinese stocks listed in the Mainland within the MSCI China All Shares -0.13%, led by financials +1.67%, real estate +0.88%, materials +0.8%, utilities +0.15%, energy -0.12%, staples -0.27%, industrials -0.58%, discretionary -0.64%, health care -0.65%, tech -1.79%, and communication -1.98%.

Northbound Stock Connect, the trading platform for foreign investors to buy Mainland stocks, had an interesting day as Shanghai saw buying and the Shenzhen selling in a reversal of recent trends. Shanghai Connect volume leader Kweichow Moutai was bought 2 to 1, Ping An Insurance was sold 11 to 8, and China Tourism sold 9 to 8. Shenzhen Connect volume leader Luxshare was sold by a small amount, CATL bought by a small amount, and Walvax Biotech bought by a small amount. Foreign investors bought $305mm of Mainland stocks today as Northbound Connect trading accounted for just over 5% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 6.98 versus 6.98 yesterday

- CNY/EUR 8.20 versus 8.20 yesterday

- Yield on 1-Day Government Bond 1.23% versus 1.47% yesterday

- Yield on 10-Year Government Bond 2.94% versus 2.95% yesterday

- Yield on 10-Year China Development Bank Bond 3.48% versus 3.48% yesterday