Tencent Crushes Q2 Earnings, Weixin To Remain On Apple App Store

4 Min. Read Time

Key News

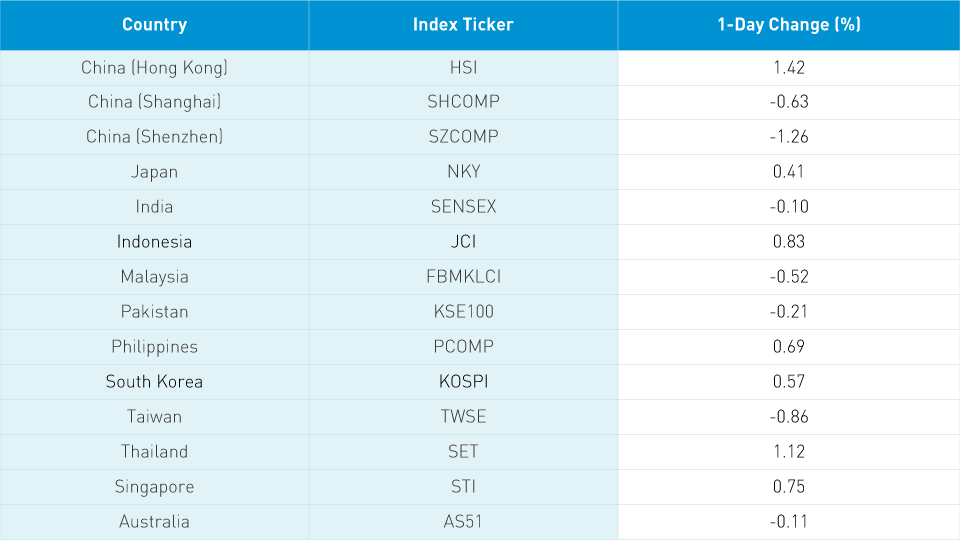

Asian equities were mixed as Hong Kong was up while mainland China was off. The US’ steepening yield curve, the yield difference between 1 year and 10-year bond, took the wind out of precious metals and momentum stocks. The disparity between growth and value stocks over the last decade has been massive and has been exacerbated by the coronavirus-induced advantage of internet companies. I simply believe value stocks are playing catch up after growth stocks have had a great run.

Tencent rose +1.36% in advance of their Q2 earnings release, which came out after the Hong Kong close today and is reviewed at length below, Meituan Dianping -2.11%, Alibaba HK -0.25%, HK Exchanges -1.12%, Semiconductor Manufacturing -3.07%, HSBC +4.84% and AIA +3.03%. Macau stocks had another nice day on loosening travel restrictions while China-domiciled stocks were weak. Remember that Macau gaming stocks AIA, HSBC and Hong Kong Exchanges are not considered Chinese companies and are not included in Chinese indices due to their Hong Kong domicile (HSBC is a British company).

Like the Chinese companies in Hong Kong, Mainland Chinese stocks were off due to not only weak sentiment driven by US China political rhetoric but also yesterday’s weak money supply and loan data. Investors are taking profits from recent winners until they get more guidance that liquidity, which drives every stock market, will not dry up as stimulus slows. We are seeing a value catch up in China as recent winners see profits being taken. Again, I do not think this is a major change, just a breather.

Trip.com (TCOM US), formerly known as C-trip, rebounded yesterday following rumors that the company wants to take itself private. The online travel company has obviously been adversely affected by global quarantines.

Shake Shack opened its first restaurant in Beijing following its first China restaurant last year in Shanghai. According to a Hong Kong newspaper, customers arrived hours before the opening as several hundred people waited in line. A Hong Kong newspaper quoted a man waiting in line for a burger as saying: “What we eat should not be politicized, as long as it is delicious.”

Remember that MSCI’s index pro-forma will released tonight followed by a release from Hang Seng Indexes on Friday.

Tencent (700 HK) reported strong Q2 results after the Hong Kong close and before the US open. It is very rare to see a company this large ($643 billion in market cap) grow this quickly. At the end of the conference call, Tencent CFO John Lo said the White House's Executive Order only applied to WeChat and not to Weixin, the Mainland Chinese version with separate servers from the international WeChat. Why make this differentiation? Because that way Apple won’t have to pull the app off their phones in China, which would be the end of Apple in China as the company derived 15% of its revenue in China in Q2. As my friends in Boston would say “wicked smaht!”. Due to their stake in the company, Tencent included online gaming streamer Huya (HUYA US) in its results.

- Revenues +29% to $16.228B (RMB 114.883B) versus analysts estimate RMB 112B

- Value Added Services Revenue (Online Gaming, video, music) +35% to RMB 65.002B from 48.080B

- FinTech Revenue (mobile payment, wealth management) increased to RMB 29.862B from 22.888B

- Online Advertising Revenue RMB 18.552B from 16.409B

- Other Revenue (Cloud computing) RMB 1.467B from 1.444B

- WeChat/Weixin Users +6.5% to 1.206B

- Operating profit +38% to $5.315B (RMB 37.629B) versus estimate RMB 34.962B

- Operating margin 33%, up from last year’s 31%

- Profit $4.410B (RMB 31.220B)

- Adjusted EPS RMB 3.18 versus estimate RMB 3

H-Share Update

The Hang Seng rebounded +1.42%/+353 index points to 25,244 as volume rose +1.9%, placing it at almost 1.5X the 1-year average. Breadth was strong with 39 advancers and 9 decliners led by HSBC +4.84%, AIA +3.03%, and Tencent +1.36%. Hong Kong-domiciled companies returned +1.39% versus +0.62% using the HS HK 35 and China Enterprise indexes as proxies. The 205 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index fell -0.02% with utilities +2.43%, communication +1.1%, energy +0.99%, financials +0.75%, real estate +0.18%, industrials -0.02%, tech -1.34%, staples -1.56%, discretionary -1.63%, materials -3.13%, and health care -3.42%.

Southbound Stock Connect volumes were light in mixed trading. Shanghai Connect volume leaders were SMIC, which was bought very slightly, Tencent, which was bought not quite 2 to 1, and Meituan Dianping, which was bought 3 to 1. Mainland investors bought $34mm worth of Hong Kong stocks as Southbound Stock Connect trading accounted for 11% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen were off -0.63% and -1.26% to close at 3,319 and 2,215, respectively, as volumes declined -4.9%, which is 1.2X the 1-year average. Breadth was off with 910 advancers and 2,764 decliners as large caps fell less than mid and small caps. The 510 Mainland Chinese companies within the MSCI China All Shares Index fell -0.71% with real estate +1.49%, utilities +0.49%, energy +0.47%, financials +0.38%, tech +0.28%, communication -0.43%, industrials -0.98%, staples -1.33%, discretionary -1.36%, materials -1.62%, and health care -3.03%.

Northbound Stock Connect volumes were moderate as foreign investors net bought Shanghai-listed stocks and sold Shenzhen-listed stocks. Shanghai Connect volume leaders were China Tourism, which was sold slightly, Kweichow Moutai, which was bought slightly, and Jiangsu Hengrui Medicine, which was sold 3 to 1. Shenzhen Connect volume leaders were Luxshare, which was sold 4 to 3, East Money Informatiom, which was bought nearly 2 to 1, and Walvax Biotech, which was sold slightly. Foreign investors sold -$235mm worth of Mainland stocks as Northbound Connect trading accounted trading for 5.8% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.94 versus 6.95 yesterday

- CNY/EUR 8.19 versus 8.18 yesterday

- Yield on 1-Day Government Bond 1.43% versus 1.43% yesterday

- Yield on 10-Year Government Bond 2.96% versus 2.95% yesterday

- Yield on 10-Year China Development Bank Bond 3.49% versus 3.47% yesterday