July Industrial Production Reaffirms V-Shaped Recovery, Hang Seng Index Inclusions Announced, Baidu & IQ Report Q2 Earnings, Week In Review

6 Min. Read Time

Week In Review

- Tencent fell -4.83% in Monday trading in Hong Kong following the White House executive order that may restrict US businesses from transacting with the company within US jurisdiction.

- Tencent Music Entertainment (TME US) reported strong results that were above analyst expectations for Q2 on Tuesday. Revenues increased +17.5% to $981mm (RMB 6.93B) versus estimate RMB 6.871B as the company announced a partnership with Universal Music Group.

- On Wednesday, Tencent (700 HK) reported strong Q2 results after the Hong Kong close and before the US open. Revenues grew +29% to $16.228B (RMB 114.883B) versus an estimated RMB 112B. It is very rare to see a company this large ($643 billion in market cap) grow this quickly.

- On Thursday there was speculation that the PBOC has been buying government debt. If true, stimulus is far from over.

Key News

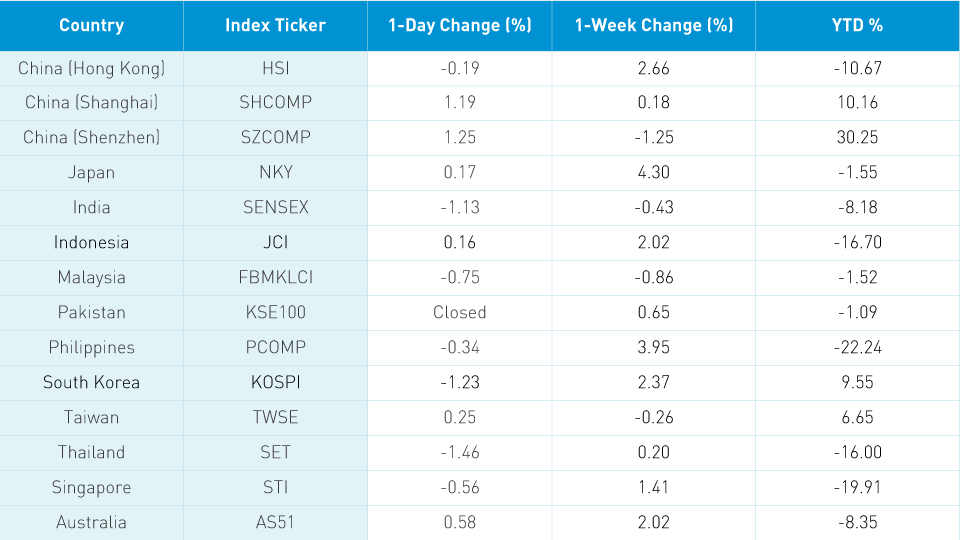

Asian equities ended a strong week mixed on Friday with light summer volumes. Considering all of the headlines, if you closed your eyes what do you imagine stock markets did? I would say that they were down, but the opposite is true! Check out our weekly returns chart below. This why I asked you to check out CHN (offshore renminbi) before making an emotional investment decision. CNH did not move on the economic data.

Hong Kong bounced around the room to post a modest loss on light volumes. Volume leaders were Tencent, which fell -0.69%, Meituan Dianping, which rose +3.97%, Alibaba HK -0.56%, Xiaomi +0.92%, China Tower +2.84%, and AIA +1.01%. Remember that Hong Kong stocks are foreign investors’ primary definition of China and therefore tend to reflect the overhang of US-China political rhetoric. In speaking with a Hong Kong reporter last night, he said the recent coronavirus outbreak appears to be coming under control. Mainland China rebounded in the afternoon session as investors speculate that the economic release will allow policy makers to support the economy. It was a broad rebound though several brokers noted more defensive plays such as financials, real estate, and liquor stocks outperformed. Foreign investors were net buyers of Mainland stocks today, buying nearly $1B worth of Mainland stocks, bringing the week to date total to $959mm.

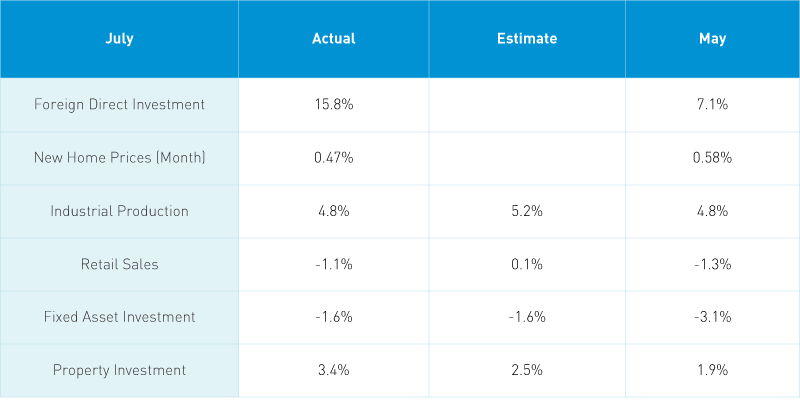

Takeaway: The economic data release was a touch light though continues to show a v-shaped recovery is underway. Industrial Production was largely in line with estimates, which highlights the fact that China is going back to work as Manufacturing rose +6%. China’s V-shaped recovery is occurring. Within Manufacturing, Auto Manufacturing +21.6% as China’s auto sales appear to be coming up out of a recent trough. Auto sales from the Retail Sales release show that while auto sales were weak in July, production is increasing in anticipation of future demand. Food production was weak falling -2.2% as heavy rains and flooding likely put a damper on the segment. The value of retail sales was off slightly month over month with JD.com and Alibaba’s June sales events potentially a factor. Catering, i.e. restaurant sales, fell -11%, which is actually an improvement from June. This is key for every investor: even with an effective quarantine, there is an apprehension about entering restaurants without a cure or a vaccine. What is also very important is that July online sales were not given but online sales Year-to-Date were. Online retail sales YTD rose +15.7% versus total retail sales, which fell -9.9% year to date. Habits formed during the quarantine are sticking, which is also a very important lesson for global investors. Mainland equities initially sold off on the data release, but had a steady comeback in the afternoon. The data was not that bad, but it does show that policy makers should not take their foot off the stimulus gas pedal. Remember to always look at China’s currency when you see a China headline. The currency market is much more important than the stock market for understanding what smart money thinks. China’s currency was flat overnight.

After the close in Hong Kong, Hang Seng Indexes announced that Alibaba HK, Xiaomi, and WuXi Biologics would be added to the Hang Seng Index on September 7th. Surprisingly, Meituan Dianping did not make the cut, but WuXi did. The Hang Seng Index not only has more than $20B worth of Asia ETF assets benchmarked to it, but also serves as a benchmark for a large futures contract as well as many structured products. Alibaba HK remains to be added to Southbound Connect. While there is no link between the Hang Seng Index and Southbound Connect, one has to assume it adds some pressure for Alibaba HK to be added to the program, thereby allowing Mainland investors to hold the stock.

Mainland search giant Baidu (BIDU US) reported Q2 results after the US close. While top line growth was minimal, the company beat analyst expectations significantly as it slashed expenses, which lead to a sharp rise in profitability. Baidu’s management delivered strong bottom line results despite a challenging business environment post-China’s quarantine. A hat tip to management for their fiscal prudence, which led to the strong results.

- Revenues -1% to $3.69B (RMB 26.034B) from RMB 26.326B though above analyst estimates of RMB 25.716B

- Cost of revenues -19% $1.86B (RMB 13.1B) from RMB 16.116B while Selling, General & Administrative Expense decreased -16% to $625mm (RMB 4.4B) from RMB 5.243B and R&D +2% to $685mm (RMB 4.8B) from RM 4.734B

- Adjusted Net Income $703mm (RMB 5B) versus analyst estimates of RMB 3.274B which is 55% higher

- Adjusted EBITA $993mm (RMB 7B) versus analyst estimates of RMB 5.14B which is 36% higher

- Adjusted EPS was $2.08 (RMB 14.73) versus analyst estimates of RMB 9.422 which is 56% higher

- Q3 Revenue forecast was -6% to +2%

- The Board raised the stock repurchase to $3B from $1B through December 31, 2022; the company has purchased $1.9B of shares in the last two years

Online entertainment company iQiyi (IQ) reported Q2 results after the US close. The results will be overshadowed by the company’s announcement that the SEC is reviewing the claims of a short selling firm that claims the company is inflating user numbers and revenue by 27% to 44%. IQ was spun off from Baidu, which has a solid reputation. The investment banks that brought IQ public are also global institutions with equally sold reputations. The company’s auditor is Ernest &Young’s Mainland subsidiary. As of the end of Q1, well-respected Chinese private equity firm Hillhouse Capital, the largest in Asia with ~$50B in AUM, is IQ’s second largest shareholder. I am skeptical that this many professionals of this caliber completely missed what is alleged to be deeply fraudulent activity. The company is sitting on RMB 4.28B/$620mm in cash. The company is being hurt by a slow pick up in offline retail sales, which hurts advertising revenue, despite high user numbers.

- Revenues +4% to $1B (RMB7.4B) versus analyst estimates of 7.319B

- Membership services revenue +19% to $527mm (RMB 4B)

- Online advertising revenue -28% to $224mm (RMB 1.6B)

- Cost of revenues decreased -2% to $967mm (RMB 6.8B) while Selling, General & Administrative expenses-11% to $169mm (RMB 1.2B) and R&D was flat to $94mm

- Operating loss was -$181mm (RMB 1.3B) which is down from RMB 1.9B

- Net loss was $204mm (RMB 1.4B) versus analyst estimates of RMB -2.331B

- Adjusted EPS was -$0.28 (RMB 1.96B) versus analyst estimates of RMB -3.025

- Q3 revenue forecast is -6% to 0%

Earnings season continues for US-listed Chinese companies next week with JD.com releasing Q2 earnings on Monday, Sina/Vipshop/Weibo on Wednesday, Alibaba on Thursday, and Meituan Dianping/Baozun/Pinduoduo on Friday. (subject to change of course)

H-Share Update

The Hang Sang had a volatile day closing -0.19%/-47 index points at 25,183 on light volumes, which fell -11% from yesterday, dipping below the 1-year average. Breadth was off with 19 advancers and 26 decliners led by HSBC -1.98%/-42 index points, AIA +1.01%/+26 index points, and Tencent -0.69%/-19 index points. China-domiciled companies outperformed Hong Kong-domiciled companies +0.21% versus -0.31% using the HS China Enterprise and HK 35 Indexes as proxies. The 205 Chinese companies listed in Hong Kong returned a total of +0.34% led by discretionary +2.57%, real estate +0.95%, industrials +0.86%, financials +0.52%, staples +0.42%, materials +0.41%, tech +0.14%, energy -0.23%, communication -0.48%, health care -0.58%, and utilities -1.21%.

Southbound Stock Connect volume was light though Mainland investors were net buyers of Hong Kong stocks. Shanghai Connect volume leaders were Tencent, which was sold 5 to 4, Meituan Dianping, which was bought 2 to 1, and China Unicom, which was bought 4 to 1. Mainland investors bought $342mm worth of Hong Kong stocks today as Southbound Stock Connect trading accounted for 10.2% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen had a volatile day though rallied to close +1.19% and +1.25% at 3,360 and 2,244, respectively. Volume was off -2.75% from yesterday, which is just above the 1-year average while breadth was positive with 1,984 advancers and 1,606 decliners. Mid and small caps outperformed by a modest amount. The 510 Mainland companies within the MSCI China All Shares Index gained +1.38% with real estate +1.86%, financials +1.71%, staples +1.7%, tech +1.55%, industrials +1..49%, communication +1.47%, discretionary +1.19%, health care +0.69%, materials +0.65%, utilities +0.57%, and energy +0.2%.

Northbound Stock Connect volumes were light though foreign investors were active buyers of Mainland stocks. Shanghai Stock Connect volume leaders were Kweichow Moutai, which was bought slightly, China Tourism Group, which was sold by a tiny amount, and Ping An Insurance, which was bought by nearly 3 to 1. Shenzhen Stock Connect volume leaders were Luxshare, which was bought 2.5 to 1, Wuliangye Yibin, which was bought by 7 to 4, and BOE Technology, which was sold by 6 to 5. Foreign investors bought $925mm worth of Mainland stocks today as Northbound Stock Connect trading accounted for 5.6% of Mainland turnover.

Last Night's Exchange Rates, Prices, & Yields

- CNY/USD 6.95 versus 6.95 yesterday

- CNY/EUR 8.22 versus 8.22 yesterday

- Yield on 1-Day Government Bond 1.38% versus 1.38% yesterday

- Yield on 10-Year Government Bond 2.94% versus 2.96% yesterday

- Yield on 10-Year China Development Bank Bond 3.45% versus 3.47%

- China Copper Price -1.17%