JD Delivers On Q2, Revenge Of The Value Nerds

3 Min. Read Time

Key news

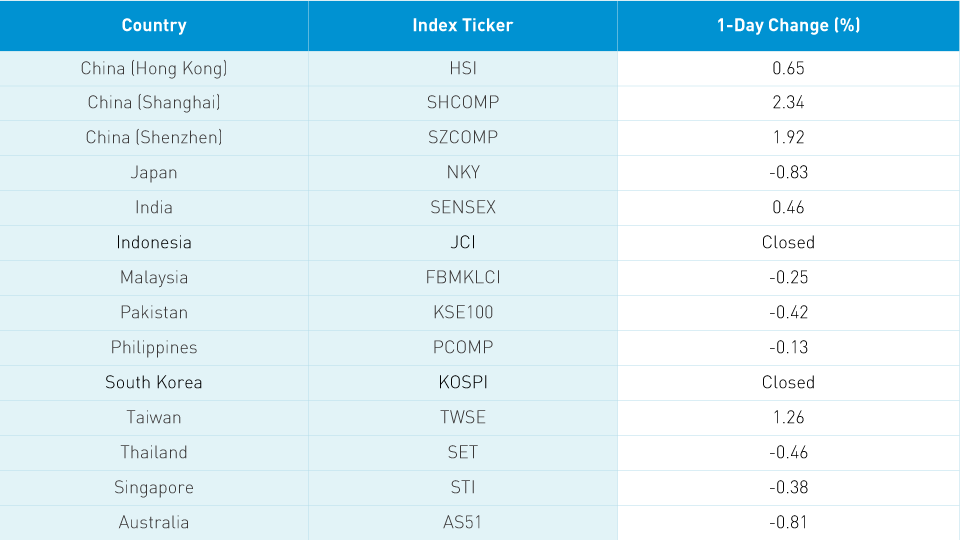

Asian equities were largely off on weak US economic data both Friday and today as well as Japan's dismal GDP data, which was released today. Slowing US retail sales were missing in today’s headlines due to another US Postal Service ballot Tweet, which the US media fell for, hook, line, and sinker. Concerns mounted over the postponement of the US-China virtual trade meeting. No reason was given for postponing the call, but China is busy with policy meetings. Either that or good news on Chinese agriculture purchases doesn’t fit with the campaign narrative.

Hong Kong and China bucked the trend after the PBOC added significant liquidity to the financial system through the 1-year medium-term lending facility (MLF). Remember that on Friday we commented on the Mainland’s rally having been due to expectations of such a move. We also had Trump extending the TikTok review period to 90 days. Hong Kong volume leaders were Tencent, which fell -0.39%, Ping An Insurance, which rose +2.83%, Alibaba HK, which fell -1.62%, Xiaomi, rising +5.61%, Meituan Dianping, which fell -0.73%, and China Life, which rose +5.17%.

Remember after the Hong Kong close Friday Hang Seng announced that Xiaomi, Alibaba HK and Wuxi Biologics would be added to the index while, surprisingly, Meituan will not. One broker speculated that the reason is that Meituan and Alibaba are in the same sub-sector. Therefore, Meituan was left out in favor of Wuxi, which is in the healthcare sector, in favor of a more diversified inclusion.

JD.com HK was off -0.16% and NetEase fell -0.83%. Growth names took a breather while value sectors played catch up on the day. Mainland China was up strongly led by financials on chatter of numerous reforms such as the easing of both IPO rules and financial advisor rules on client prospecting. It was a very broad and impressive rally on the Mainland today with strong foreign investor participation.

Remember to always check the offshore renminbi (CNH) to gauge US-China political headline risk. Our institutional traders are buying US-listed Chinese stocks when investors are scared off by headlines. They always check CNH to tell if there is any bark to a headline. Thus far, despite the headlines, CNH has appreciated versus the US dollar.

JD.com (JD US) reported solid Q2 results before the US market open today. The company grew both the top line, i.e. revenue, and bottom line, net income and EPS, while trouncing analyst expectations.

- Revenues +33% to $28.5B (RMB 201B) and above analyst expectations of RMB 190B

- Cost of revenues +34% to $24.4B (RMB 172B)

- Non GAAP Net Income $800mm (RMB 5.9B) up from RMB 3.6B and above analyst expectations of RMB 3.967B

- Adjusted EPS $0.50 (RMB 3.51) up from RMB 2.30 and analyst estimates RMB 2.71.

H-Share Update

The Hang Seng opened higher and slid off the day’s high but closed up +0.65%/+164 index points at 25,347. Volume jumped 24% and was just above the 1-year average as breadth was positive with 33 advancers and 16 decliners. Index heavyweights led the way with Ping An Insurance gaining +2.83%/+43 index points, HK Exchanges +2.23%/+30 index points, and today’s best performer China Life +5.17%/+23 index points. Geely Auto was the day’s worst performer after falling -6.35%/-17 index points. China-domiciled companies outperformed Hong Kong-domiciled companies +1.16% versus +0.7% using the HS China Enterprise and HK 35 indexes as proxies. The 205 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index rose +0.71% with materials +3.04%, financials +2.34%, tech +2.05%, energy +1.4%, health care +1.19%, industrials +0.72%, utilities +0.4%, real estate +0.28%, staples +0.14%, communication -0.35%, and discretionary -0.47%.

Southbound Stock Connect trading was light in mixed trading. Shanghai Connect volume leader SMIC was sold 7 to 4. Tencent was bought 2 to 1 and Meituan Dianping was bought 4 to 1. Mainland investors bought $341mm worth of Hong Kong stocks today as Southbound Connect trading accounted for 12% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen ripped higher gaining +2.34% and +1.92% to close at 3,438 and 2,287, respectively, on volumes that were +35% higher than Friday, placing volume at 1.5X the 1-year average. Breadth was exceedingly strong with 3,230 advancers and only 448 decliners. Large caps outperformed mid and small caps modestly. The 510 Mainland stocks within the MSCI China All Shares Index gained +2.2% with financials +4.07%, materials +2.39%, energy +2.3%, real estate +2.11%, discretionary +2.07%, tech +1.66%, staples +1.62%, industrials +1.52%, health care +1.26%, and utilities +1.02%.

Northbound Stock Connect trading volume was moderate in mixed trading as Shanghai stocks were net sold while Shenzhen stocks were net bought. Shanghai volume leader Ping An was sold 2 to 1, Kweichow Moutai had sellers just outpace buyers, and Jiangsu Hengrui Medicine was sold slightly. Shenzhen volume leaders were East Money, which was bought 7 to 5 , Luxshare, which was bought 6 to 5, and Wuliangye Yibin, which was bought 3 to 2. Foreign investors bought $823mm worth of Mainland stocks today as Northbound Stock Connect trading accounted for 7.7% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.94 versus 6.95 Friday

- CNY/EUR 8.23 versus 8.22 Friday

- Yield on 1-Day Government Bond 1.33% versus 1.38% Friday

- Yield on 10-Year Government Bond 2.94% versus 2.94% Friday

- Yield on 10-Year China Development Bank Bond 3.44% versus 3.45% Friday