Xiaomi Earnings Power ATMX Higher, Bilibili Q2 Gets Jiggy Wit It

5 Min. Read Time

Please fill out this quick survey to help us improve China Last Night.

Key News

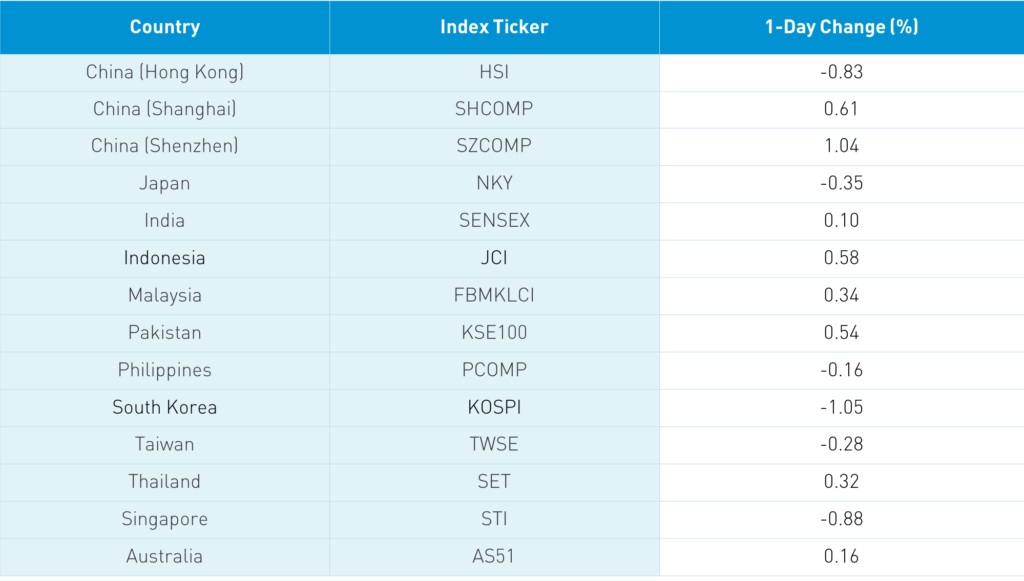

Asian equities were quiet ahead of today’s Fed Chair announcement. How quiet was it? An institutional broker’s morning note had no notes! It was literally blank while another broker’s Asia recap didn’t include Hong Kong. The Hang Seng Index was off today, but that was mainly due to China Mobile, which was off -5.09% post-earnings, and HSBC, which was off -1.91%.

Unfortunately, Xiaomi isn’t going to be added to the Hang Seng Index until the 2nd week of September, though it reported very strong earnings leading to a massive gain of +11.43%. Growth names had a great night as Xiaomi was the volume leader, followed by Tencent, which was up +1.18%, Alibaba Hong Kong, which pulled a James Bond gaining +0.07%, Meituan Dianping, which rose +4.71%, Semiconductor Manufacturing (SMIC), which rose +3.01%, JD.com Hong Kong, which rose +0.25%, and online insurance company ZhongAn Online P&C Insurance, which rose +22.86% on a strong earnings report. Value sectors were off today.

Mainland investors were in a better mood as both Shanghai and Shenzhen rebounded today. The CSRC interview, which is discussed below, appeared to have a positive effect as growth sectors outperformed value sectors. The National Bureau of Statistics reported Industrial Profits +19.6% year over year, though this economic release isn’t a market mover nor widely followed.

Below is a chart of our US-China political rhetoric indicator CNH, which is the ticker for China’s offshore currency that trades during US hours. Interesting, right? Is the US dollar going up or down? My money is on down.

Bloomberg News interviewed Fang Xinghai, Vice Chairman of the China Securities Regulatory Commission (China’s version of the SEC), on the long-standing issue of China not allowing US-listed Chinese companies’ auditor working papers. If there was ever an olive branch, this is it. Fang mentioned a willingness to share the audit papers for State-Owned Enterprises without state secrets included. I’ve long suspected that the issue is a small number of State-Owned Enterprises, despite the vast majority of US-listed Chinese companies being private companies.

The article wasn’t big news but did hit the screens of several brokers who trade US-listed Chinese companies. They appear to think that there is a real opportunity to put this to bed. By far the easiest solution is to just let the private companies present their audit papers and figure out the SOEs later. The article does mention that Fang called the PCAOB recently and that they haven’t called him back! He visited the US in November 2019 and the PCAOB head refused to meet him! This brings my "kabuki theater" thesis to a whole different level. Playing Russian roulette with over $1 trillion of US investors’ savings is absurd. Do US politicians know that the PCAOB head refused to meet with his Chinese counterpart? They are probably unaware as the House finance committee only interviewed SEC head, Jay Clayton. Wow. Let’s hope the US calls them back.

Yesterday, there were a few headlines about Vanguard closing its Hong Kong office and Hong Kong-listed ETFs. What the headlines missed is that Vanguard is moving its Asia headquarters from Hong Kong to Shanghai. Like many US financial firms, Vanguard sees a massive opportunity in Mainland China. Hands down figuring out China will be the largest growth engine for US financial firms in the next decade. BlackRock announced last week a deal with China Construction Bank and Singapore sovereign wealth fund Temasek. JP Morgan Asset Management is in the process of buying out its Mainland partner.

When the going gets tough, the tough get going, right? TikTok CEO Kevin Mayer announced yesterday his resignation. I imagine a TikTok sale is coming very soon that potentially didn’t include Mr. Mayer.

Prepare to feel old... Bilibili, a US-listed Chinese online entertainment platform for “young generations in China”, reported Q2 results after the US close. Bilibili is hard to define. It is similar to YouTube in that users can post videos, though there is an emphasis on online gaming and anime/comic characters. Twitch is a western website that allows users to watch other people play video games. Yes, that’s a thing. Though I suppose it isn’t different than us watching the NFL on Sundays (hopefully!).

- Revenues +70% to $370mm (RMB 2.617B) versus analyst estimate of RMB 2.55B

- Monthly Active Users +55% to 171mm while mobile MAUs +59% to 152mm

- Average Paying Users +105% to 12.9mm

- Cost of Revenues +57% to $285mm (RMB 2.013B)

- Gross Profit +140% to $85mm (RMB 604mm)

- Total Operating Expenses +103% to $171mm (RMB 1.214B)

- Adjusted Net Loss -$67mm (RMB 475mm) versus analyst estimates RMB -477mm

- Adjusted EPS -$0.19 (RMB -1.35) versus analyst estimates RMB -1.50

- Q3 Revenue forecast between RMB 3.05B and RMB 3.1B

H-Share Update

The Hang Seng slumped out of the gate and stayed there all day closing at -0.83%/-210 index points at 25,281. Volume increased by +13% to almost 1.5X the 1-year average while breadth was off with only 8 advancers and 41 decliners led by China Mobile which was off -5.09%/-52 index points, HSBC -1.91%/-39 index points and Tencent +1.18%/+36 index points. Hong Kong domiciled companies were off -0.7% versus -0.96% for Chinese domiciled stocks using the HS Hong Kong 35 and China Enterprise Indexes as proxies. The 205 Chinese companies listed in Hong Kong within the MSCI China All Shares were up +0.64%, led by tech +5.7%, discretionary +3.01%, health care +1.9%, communication +0.71%, staples +0.02%, materials -0.37%, financials -0.7%, industrials -0.72%, utilities -1.17%, real estate -1.69%, and energy -2.57%.

Southbound Stock Connect volumes were moderate/light though Mainland investors were active buyers of Hong Kong stocks. Shanghai Connect volume leaders were Xiaomi bought almost 3 to 1, SMIC bought almost 6 to 5, and Tencent bought 2 to 1. Mainland investors bought $549mm of Hong Kong stocks today as Southbound Connect trading accounted for 11.1% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen overcame a morning dip to close up +0.61% and +1.04% at 3,350 and 2,261 as volume fell -14% to just above the 1-year average. Breadth was strong with 2,650 advancers and 1,109 decliners as mid and small caps outperformed large caps. The 510 Mainland stocks within the MSCI China All Shares were up +0.82%, led by tech +1.33%, discretionary +1.29%, health care +1.24%, industrials +1.12%, materials +0.6%, energy +0.49%, financials +0.21%, utilities -0.26%, communication -0.31%, and real estate -1.05%.

Northbound Stock Connect volumes were light in mixed trading as foreign investors preferred Shenzhen growth stocks over Shanghai value stocks Shanghai volume leaders were Kweichow Moutai sold 2 to 1, Inner Mongolia Yili Industrial sold 6 to 5, and Longi Green Energy Technology sold a touch. Shenzhen Connect volume leaders were CATL bought 3 to 1, Wuliangye Yibin sold 2 to 1, and Gree Electric Appliances bought 2 to 1. Foreign investors sold -$145mm of Mainland stocks today as Northbound Stock Connect trading accounted for 6.1% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.90 versus 6.89 yesterday

- CNY/EUR 8.13 versus 8.14 yesterday

- Yield on 1-Day Government Bond 1.15% versus 1.15% yesterday

- Yield on 10-Year Government Bond 3.06% versus 3.05% yesterday

- Yield on 10-Year China Development Bank Bond 3.61% versus 3.60% yesterday