August PMIs Confirm China’s V-Shaped Recovery

4 Min. Read Time

We are hosting two webinars in September, please join us!

1. China Macro Update: Digital Transformation & Structural Reforms Provide Catalysts For Post Covid-19 Growth

2. Covid:19: An Inflection Point For Emerging Markets Consumer Technology

Key News

Asian equities ended a strong month largely lower though Japan was an outlier to the upside as Warren Buffett bought several Japanese companies geared to commodities. Hat tip to the Hedgeye team who has been pounding the table on commodities for quite some time. Today, ETFs and index funds benchmarked to MSCI need to trade their portfolios at the market close due to the Quarterly Index Review. The rebalance may have had an effect on trading today as both Hong Kong and Mainland China gave up nice gains to close down for the day.

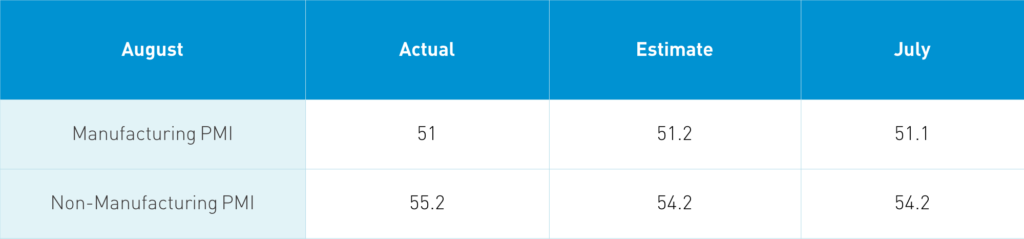

Last night the “official” PMIs were released by the National Bureau of Statistics.

Takeaway: The PMIs are a diffusion index. Levels over 50 mean growth month over month and under 50 indicate decline month over month. The “official” PMIs are a broad survey of large companies compared to the Caixin IHS Markit PMIs, which will be released later this week and surveys a smaller number of private, small and medium-sized companies. It is evident that China’s economy is continuing its V-shaped recovery post quarantine. Both PMIs showed output and new orders picking up month over month though employment remained weak and Manufacturing’s new export orders came in at 49.1, i.e. a slight decline. The economic consequence of global quarantines will have an effect on China though domestically geared companies should fare well. Investors should take note!

In addition to the MSCI rebalance, brokers noted that PMIs were largely positive, which led some to speculate there may be less stimulus in the future. I would argue that employment is job #1 for every government and the slight employment weakness will be noted by policy makers.

We also had a large number of corporate earnings today including Chinese banks showing revenue declines as non-performing loans grew as a consequence of the economic consequence of the quarantine. Remember this is backward looking and China’s economic recovery should reduce this issue.

Hong Kong volume leaders were Tencent, which rose -1.85%, Xiaomi, which rose +4.44%, Alibaba HK, which rose +2.09%, Meituan Dianping, which fell -3.62%, HK Exchanges, which rose, +2.79%, and Geely Auto, which rose +4.07%. Today was a fairly risk off day as recent outperformers were hit with profit taking. Alibaba HK and Xiaomi will be added to the Hang Seng Index September 7th. Mainland China also came off gains to close down as foreign investors net sold Mainland stocks via Northbound Stock Connect. The foreign sales may have been related to the MSCI rebalance, but it is hard to say. Ultimately, one needs to take a step back and look at the monthly and year to date returns.

I’ve written extensively on US investors’ home bias. I believe this is due to the focus on FAANG though few recognize that growth companies globally are outperforming as well. This is not a US-only phenomenon, but a global phenomenon. Overnight, it was released that Warren Buffett purchased shares in several Japanese companies. The world’s most famous investor is diversifying with non-US equities. Are you?

How did our US-China political indicator respond? CNH, China’s offshore currency that trades during US trading hours, appreciated versus the US $. This tells us that recent political news is likely just noise.

Yum China is looking to relist in Hong Kong, raising $2.5 billion by selling 41 million shares.

A research firm based in mainland China noted that ETF Connect will be launched. I’ve not seen this confirmed elsewhere but the implications would be strong as it would allow mainland investors to buy HK listed ETFs. This could lead inflows into Hong Kong stocks. I’ll dive in to get more details.

H-Share Update

The Hang Seng opened higher but came off a +1.67% gain to close -0.96%/-245 index points at 25,177. Volumes were nearly 10% higher, which is more than 1.5X higher than the 1-year average. Breadth was off with 16 advancers and 33 decliners led by Tencent, which fell -1.85%/-54 index points, China Construction Bank, which fell -2.83%/-50 index points, and HK Exchanges, which rose +2.79%/+39 index points. Hong Kong-domiciled stocks were +0.01% versus -1.88% for China-domiciled stocks using the HS HK 35 and China Enterprise Indexes as proxies. The 205 Chinese companies listed in Hong Kong within the MSCI China All Shares Index fell -1.85% with energy +1.25%, tech +0.72%, utilities -1.41%, health care -1.43%, industrials -1.46%, materials -1.92%, communication -1.95%, real estate -2.09%, financials -2.11%, discretionary -2.99%, and staples -3.05%.

Southbound Stock Connect trading was moderate as Mainland investors were net buyers of Hong Kong stocks today. Shanghai Connect volume leaders were Xiaomi, which was bought 9 to 5, Tencent, which was bought 3 to 1, and Meituan Dianping, which was sold 2 to 1. Mainland investors bought $631mm worth of Hong Kong stocks today as Southbound Connect trading accounted for 9.3% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen also came off intra-day gains of +1.14% and +1..02% to close -0.24% and -0.44%, respectively. Volume was up +9% from Friday though only 1/3 higher than the 1-year average. Breadth was mixed with 1,890 advancers and 1,750 decliners as mid and small caps underperformed large cap companies slightly. The 510 Mainland stocks within the MSCI China All Shares Index fell -0.22% with utilities +0.97%, staples +0.81%, materials +0.43%, energy +0.16%, health care -0.32%, tech -0.48% industrials -0.57%, financials -0.61%, real estate -0.64%, communication -0.67%, and discretionary -1.25%.

Northbound Stock Connect volumes were moderate as foreign investors were net sellers of Mainland stocks. Shanghai Connect volume leader was Inner Mongolia Yili Industrial, which was bought by 4 to 3. Kweichow Moutai was bought slightly and Ping An was sold by 10 to 7. Foreign investors sold a net $1.1 billion worth of Mainland stocks today as Northbound Connect trading accounted for 7.6% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.84 versus 6.87 Friday

- CNY/EUR 8.18 versus 8.17 Friday

- Yield on 1-Day Government Bond 1.45% versus 1.02% Friday

- Yield on 10-Year Government Bond 3.02% versus 3.07% Friday

- Yield on 10-Year China Development Bank Bond 3.59% versus 3.63% Friday