Indian Teenagers’ Worst Quarantine Nightmare: No TikTok, and now no PUBG

4 Min. Read Time

We have two webinars coming up in September. You can find the descriptions below.

China Macro: Thursday, September 17th, 9 am EST

China Macro Economic Outlook: Digital Transformation and Structural Reforms Provide Catalysts for Post COVID-19 Growth

EM Consumer Technology: Tuesday, September 15th, 11 am EST

COVID-19: An Inflection Point For Emerging Markets Consumer Technology

Key News

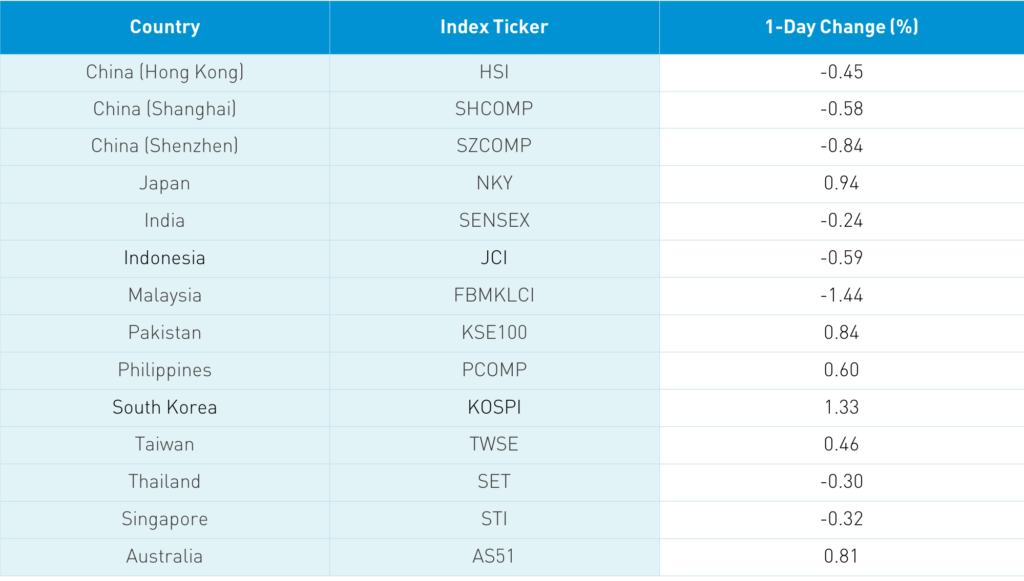

Asian equities were largely off on light volumes, with Japan as a positive outlier. Hong Kong and Mainland China were off as Secretary State Pompeo’s comments on banning Chinese diplomats occurred after China’s close yesterday. More front and center was India broadening its ban on Chinese apps, including AliPay and Tencent’s exceedingly popular video games series, PlayUnknown’s Battlegrounds (PUBG). Can you imagine Indian teenagers in quarantine? No TikTok, and now no PUBG? It does make me wonder if Prime Minister Modi has picked up on the distraction of ‘look over there’ as India’s coronavirus cases are overtaking Brazil’s.

Populist presidents don’t appear to be doing well in crisis management. In Hong Kong, a period of profit-taking took place in growth names, despite the chatter of policy coming to support the local semiconductor companies. Volume leaders were Xiaomi, which was off -7%, Tencent, which was off -2.02%, Alibaba Hong Kong, which was off -2.4%, Meituan Dianping, which was off -3.74%, and Semiconductor Manufacturing, which was off -1.4%. The profit-taking was across the board as Hong Kong Exchanges was off -1.88%, Geely Auto was off -6.46%, and CSPC Pharma was off -2.34%. India-China tensions were noted as catalysts in Mainland China for profit-taking in outperforming sectors like tech, communication, brokers, and our DnD trade (drugs ie. pharma stocks and drinks ie. alcohol companies).

Perhaps it is a good thing that we can’t travel overseas because traveling would be expensive! Actually, I loved discovering with my family some new spots such as Maine. Wow, a beautiful state. Highly recommended! Visiting the UK and Europe is going to be expensive as the US dollar has fallen, though the move looks a bit extended. We got a bounce yesterday in the US dollar leading to a slight weakness in CNH, China’s currency that trades during US hours. CNH is also our US-China political indicator for when big headlines hit. Did you notice the slight pullback in US-listed Chinese equities yesterday as CNH weakened? Yes– other factors are involved, but still a remarkable tandem movement. I expect that the dollar will get a bit of a rally here as it is oversold, but this could provide a great entry point for investors in non-US equities.

Broker chatter included an interesting fact from Gallup. In double-checking the chatter, I was very impressed by Gallup’s website. Of 10,000 Americans surveyed, less than 40% believe that COVID fatalities are concentrated in those over the age of 65 versus the reality that 79.3% are. Fatalities under age 25 account for 0.2%, though those surveyed believe that the percentage is more than 8%.

I stumbled upon this quote which is the motto of Thunderbird School of Global Management from founding faculty member Dr. William Lytle Schurz: "Borders frequented by trade seldom need soldiers".

Live streamer and dating app provider Momo reported weak Q2 financial results despite showing fiscal discipline by cutting costs. The company is spending money to grow its Tantan dating app (China’s version of Tinder). The core live streaming business did well, but the costs associated with the dating business dragged down overall results. I found management to be surprisingly upbeat on the conference call this morning. Investors likely won’t take such an optimistic view of the company’s results, nor will they like the revenue forecast.

- Revenues -6.8% to $547mm (RMB 3.868B) though that beat analyst expectation of RMB 3.837B

- Monthly active users declined to 111mm from 113mm

- Cost & Expenses declined -7.1% to $445mm (RMB 3.146B)

- Adjusted Net Income declined to $94mm (RMB 668mm) from RMB 1.241B though slightly ahead of analyst expectations of RMB 661mm

- Adjusted EPS $0.43 (RMB 3.05) down from RMB 5.60 though slightly ahead of analyst expectations of RMB 3.04

- Q3 Revenue forecast RMB 3.7B to 3.8B which is a decline of 16.9% and -14.6% (ouch!)

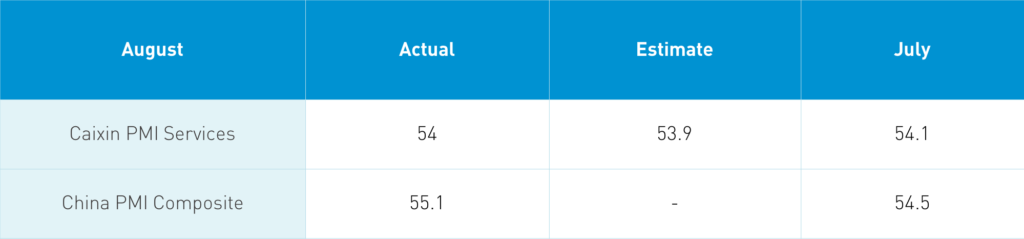

The PMI release occurred at 9:45 am, which lifted markets out of the red and into the green though the rally ran out of steam later in the day.

Takeaway: The release received surprisingly little attention from our institutional brokers, considering that the service sector accounts for 60% of China’s GDP. I assume China’s V-shaped recovery is well accepted at this point. Service sector employment finally picked in a good sign as half of the urban employment is in the service sector. This is a good confirmation that China’s consumers are alive and well, which is a great thing for US multinationals doing business in China today.

H-Share Update

The Hang Seng had a choppy session, closing -0.45%/-112 index points at 25,007 as volumes declined -8%, which is just above the 1-year average. Breadth was off with 20 advancers and 28 decliners. The broader Hang Seng Composite was off -0.95%. The 204 Chinese companies listed in HK within the MSCI China All Shares were off -1.3%, with materials and utilities outperforming, tech off -3.69%, discretionary -3.13%, staples -1.76%, and communication -1.72%. Southbound Stock Connect volumes were light/moderate as foreign investors bought $200mm of HK listed stocks as Connect trading accounted for nearly 10% of HK turnover.

A-Share Update

Shanghai & Shenzhen gave up morning gains, closing -0.58% and -0.84% to close at 3,384 and 2,301. Volumes were off -3%, which is just above the 1-year average. Breadth was off with 1,063 advancers and 2,626 decliners as mid and small caps underperformed large caps. The 517 mainland stocks with the MSCI China All Shares were off-0.76%, with only utilities closing positive. Tech was off -1.42%, communications were off -0.92% and financials were off -0.87%. Foreign investors sold -$146mm of mainland stocks today as Northbound Stock Connect trading accounted for 7.4% of mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.84 versus 6.84 yesterday

- CNY/EUR 8.10 versus 8.09 yesterday

- Yield on 1-Day Government Bond 1.10% versus 1.12% yesterday

- Yield on 10-Year Government Bond 3.11% versus 3.10% yesterday

- Yield on 10-Year China Development Bank Bond 3.68% versus 3.68% yesterday