Markets Rebound Following Monday’s Political Rhetoric Driven Toll on Stocks

3 Min. Read Time

We have two webinars coming up in September. You can find the descriptions below.

EM Consumer Technology: Tuesday, September 15th, 11 am EST

COVID-19: An Inflection Point For Emerging Markets Consumer Technology

China Macro: Thursday, September 17th, 9 am EST

China Macro Economic Outlook: Digital Transformation and Structural Reforms Provide Catalysts for Post COVID-19 Growth

Key News

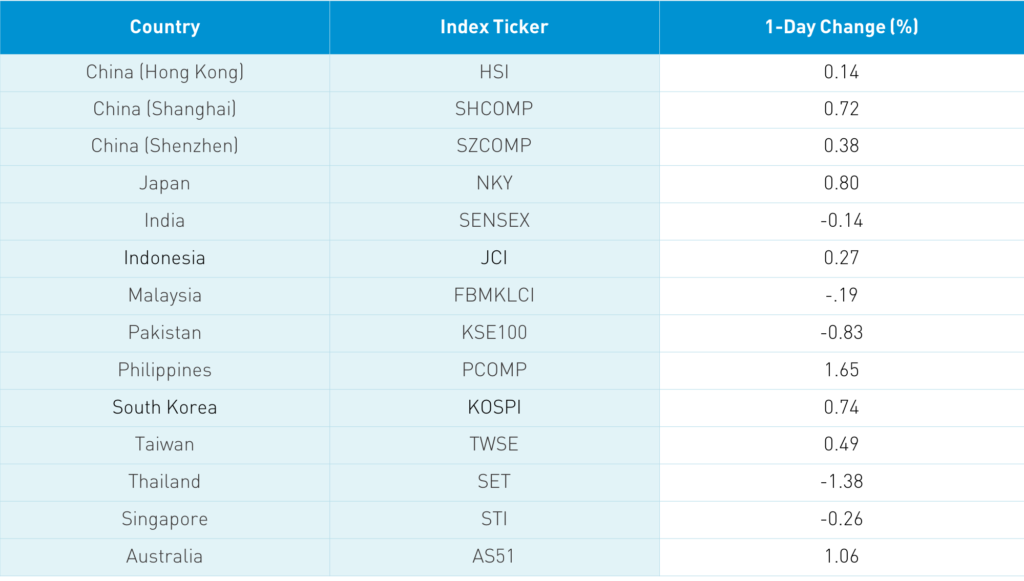

Asian equities rebounded after sharp declines on Monday following a selloff in US tech, reports of Softbank’s massive tech option trades, and increased US-China political rhetoric. On Monday, the Hang Seng was off -0.43%, with Shanghai off -1.7% and Shenzhen off -2.04%. Over the weekend there was talk that the US would add Semiconductor Manufacturing (981 Hong Kong) to the entity list, which would bar it from American and foreign suppliers, leading to a -22.88% fall on Monday. While the addition wouldn’t be too surprising, it could have an adverse effect on several US semiconductor equipment manufacturing companies.

Unfortunately, as we head into the election we can expect more of the same. CNH, China’s currency during US trading hours, didn’t react yesterday. However, with US markets open today, off-shore RMB (CNH), China's currency that trades during US hours, depreciated from 6.83/USD to nearly 6.85/USD in a sign that US political rhetoric had some bite. The US dollar looks extremely oversold to me and a counter-trend rally may be due. Defensive/value sectors reigned supreme today with financials posting a strong day in both Hong Kong and the Mainland on news that Stock Connect could be expanded.

Hong Kong volume leaders were Meituan Dianping, which was off -4.11% after being added to the Hang Seng Index Monday, Tencent, which was off -0.49%, Nongfu Spring which was up +53%, Xiaomi, which was off -7.25% and was also added to the Hang Seng Index, Alibaba Hong Kong, which was up +1.51%, Semiconductor Manufacturing, which was up +3.07%, and Ping An, which was up +1.24%. Recent winners experienced profit-taking in Hong Kong and the Mainland. Mainland Alchohol names Wuliangye Yibin was off -2.19% and Kweichow Moutai was off -0.7%. Mainland tech stocks were lower as Apple iPod maker GoerTek was off -3.69% on the political rhetoric. Foreign investors were active buyers of Mainland stocks today with nearly $1 billion of inflow.

Bottled water company Nongfu Spring (9633 Hong Kong) went public in Hong Kong today after being oversubscribed 1,100x by investors. The stock jumped +53% in trading today to HKD 33.10 from an offering price of HKD 21.50, valuing the company at HKD 47B.

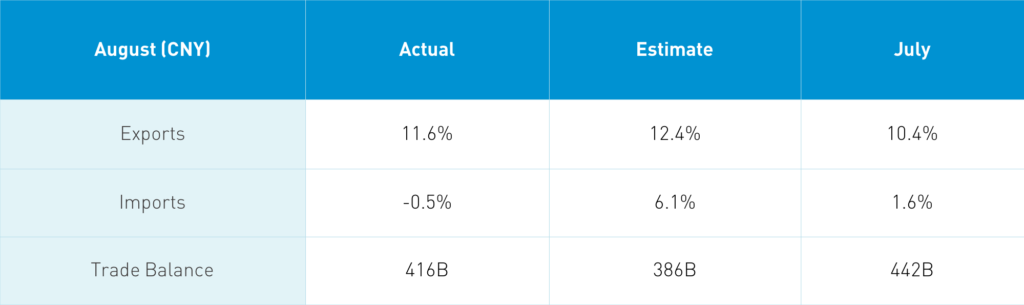

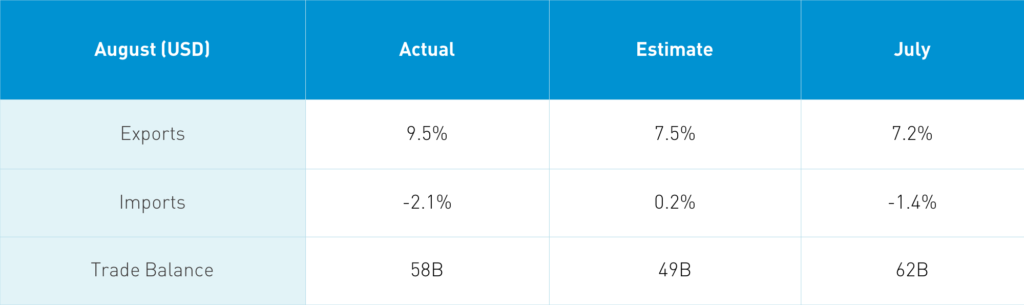

China released August trade data on Monday. The mid-morning release gave the market a short pause, as import weakness could insinuate that China’s V-shaped recovery is slowing.

Takeaway: While the market focused on the year-over-year data comparison, on a month-to-month view China’s exports increased to its two biggest customers, which are the ASEAN countries (Southeast Asia) and the EU, while US exports were off a touch. China’s imports on a month-over-month basis were slightly off. China’s commodity appetite did relax a bit in August as imported tonnage was off month-over-month.

H-Share Update

The Hang Seng rebounded from a mid-day swoon to close +0.14%/+34 index points at 24,624. Volumes were off -11% from Monday, which is just above the 1-year average. Breadth was off with 21 advancers and 25 decliners. Chinese companies outperformed Hong Kong companies by nearly 1%. The 517 Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -0.11%, led by financials +2.66%, utilities +0.68%, and energy +0.36%, while tech -3.11%, discretionary -2.73%, and health care -0.34%. Southbound Stock Connect volumes were light/moderate, accounting for nearly 12% of Hong Kong turnover with Mainland investors net sellers of -$238mm of Hong Kong stocks.

A-Share Update

Shanghai & Shenzhen were off all day until the close +0.72% and +0.38% closing at 3,316 and 2,248 respectively. Turnover was off -9% from Monday, which is just above the 1-year average. Breadth was positive with 2,472 advancers and 1,152 decliners as large caps outperformed mid and small caps. The 517 Mainland stocks within the MSCI China All Shares Index were up +0.11%, led by financials +1.86%, energy +1.55%. and utilities +0.51%, with staples off -1.31%, tech -0.86% and discretionary -0.24%. Northbound Stock Connect volumes were light/moderate accounting for nearly 5% of Mainland turnover as foreign investors bought a net $927mm of Mainland stocks today.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.85 versus 6.83 yesterday

- CNY/EUR 8.07 versus 8.07 yesterday

- Yield on 1-Day Government Bond 0.95% versus 1.00% yesterday

- Yield on 10-Year Government Bond 3.12% versus 3.14% yesterday

- Yield on 10-Year China Development Bank Bond 3.67% versus 3.70% yesterday