“ATMX” Gallops Again, August Economic Data Exceeds Expectations, Week In Review

4 Min. Read Time

We have two webinars coming up in September. You can find the descriptions below.

EM Consumer Technology: Tuesday, September 15th, 11 am EST

COVID-19: An Inflection Point For Emerging Markets Consumer Technology

China Macro: Thursday, September 17th, 9 am EST

China Macro Economic Outlook: Digital Transformation and Structural Reforms Provide Catalysts for Post COVID-19 Growth

9/11 will always be a day of reflection for many of us as we think about friends who had their lives tragically cut short. Their families should know that we keep them in our hearts and prayers. We will never forget!

Week In Review

- Bottled water company Nongfu Spring (9633 Hong Kong) went public in Hong Kong on Tuesday after being oversubscribed 1,100x by investors. The stock jumped +53% in trading today to HKD 33.10 from an offering price of HKD 21.50, valuing the company at HKD 47B.

- China pre-ordered on Wednesday 400,000 tons of US soybeans for delivery next season.

- The American Chamber of Commerce in Shanghai surveyed 346 US companies with operations in China. According to the Financial Times, less than 4% of the companies plan on relocating production back to the US.

- On Thursday, Hong Kong and Mainland China fell from intra-day gains going into the close. The selloff followed a report that trading in Mainland small caps would come under greater scrutiny after several stocks posted spectacular gains. It is important to recognize, however, that the focus is on small/micro-cap companies, which are not included in MSCI indexes.

Key News

Asian equities bucked the US market’s Thursday fall, rising nicely as China-India tensions eased following a meeting between the two sides. Hong Kong and China had a nice pop to offset a weak week, though I would have liked to see higher volumes. Bargain hunters scooped up shares after a rough week. "ATMX" led Hong Kong volumes. Tencent was up +1.98%, Alibaba HK was up +1.29%, Meituan Dianping was up +4.21%, and Xiaomi was up +3.56% while Semiconductor Manufacturing popped +6.8%. JD.com HK was flat at 0.0% while NetEase HK eased -0.42%.

Tencent has popped up in broker notes recently as the company is highlighting its new WePay mobile payment platform to compete with the publicity surrounding Ant Group’s IPO. Tencent and Ant Group have a duopoly in Chinese mobile payments, which means Tencent might see a higher valuation based on where Ant Group ends up being valued.

Healthcare stocks had a strong day as the Mexican government spoke to several Chinese pharma companies about their vaccines. The news lifted Mainland pharma stocks while the DnD trade (drugs i.e. pharma and drinks i.e. alcohol stocks) performed well, with alcohol stock Kweichow Moutai up +1.59% as the most heavily traded stock by value, and competitor Wulliangye Yibin up +2.1%. Mainland clean energy stocks had a strong day as well.

President Trump gave negotiators some motivation and likely ruined their weekend plans by stating that he wouldn’t extend TikTok’s sale deadline beyond Sept 15th. Investment bankers and those involved will be busy trying to get a deal done, though if negotiations are making progress, I expect the deadline to be extended.

Three economists from the University of Michigan, US Census Bureau, and the Federal Reserve Board published a piece titled “Beyond imports: The supply chain effects of trade protection on export growth”. In a nutshell, they show that US tariffs hurt US manufacturers and weaken US exports. Aren’t tariffs supposed to support US manufacturing? The problem is that inputs for US manufactured goods come from China. How about moving the input manufacturing back here? I don’t think anyone wants a coal smelter or an iron ore smelting furnace in their backyard. US manufacturers have to pay tariffs to get the inputs, which then raises the costs of their finished goods, making them less competitive on the global market.

Noah Smith of Bloomberg News wrote a piece titled “Trump’s Trade War Failed. Can Biden Do Better?”. Mr. Smith focused on import and export data to show that tariffs did not have a positive effect on US manufacturing. He comes to a similar conclusion as the economists, stating “…tariffs hurt the U.S. companies they were designed to help..they (tariffs) make inputs more expensive.” Mr. Smith references the economists’ work, which is how I found the piece that utilizes confidential data from US manufacturers. I’ve always felt making US manufacturers more competitive simply requires eliminating red tape. Eliminating tariffs would help.

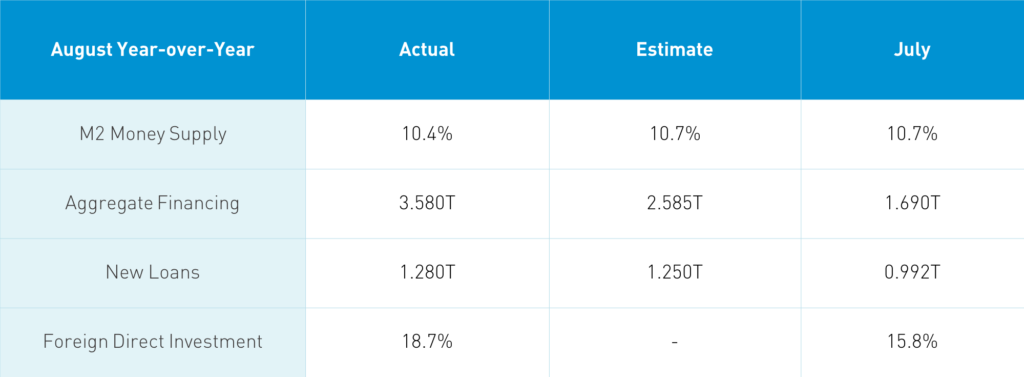

The August economic data was released after the market's close.

Takeaway: PR 101 states that Friday after the close is when you release bad news. The data release is very positive and should be well received by the local market next Monday. The aggregate financing data exceeded expectations by a wide margin, driven by government and corporate bond issuance. New loans also exceeded expectations as getting credit to private companies has been a strong policy mandate for a long time now, since they’ve historically had trouble getting loans from banks. Private companies gaining access to bank loans will crimp banks’ profits to some degree while providing support for the broader economy. This isn’t dissimilar to policy here in the US as the US government provides loans to help businesses.

H-Share Update

The Hang Seng Index went from lower left to upper right, closing near the day’s high up +0.78%/+189 index points at 24,503. Volume was off -7%, which is below the 1-year average while breadth was mixed with 26 advancers and 19 decliners. The broader Hang Seng Composite was up +1.08% with 253 advancers and 192 decliners. The 204 Chinese companies listed in HK within the MSCI China All Shares Index were up +1.29%, led by discretionary +3.37%, tech +3.08%, and health care +2.13%, while materials were off -0.51%, financials -0.16%, and real estate -0.14%. Mainland investors were net buyers of HK listed stocks in light trading via the Southbound Connect trading program. Mainland investors bought $305mm of HK listed stocks as Southbound Connect trading accounted for 10.4% of HK turnover.

A-Share Update

Shanghai & Shenzhen were flat until a late-day rally lifted +0.79% and +1.64% to 3,260 and 2,164, respectively. Volume was light, falling -22% to less than the 1-year average for the first time since late June. The 517 mainland stocks within the MSCI China All Shares were up +1.12%, led by tech +2.96%, communication +2.3%, and health care 2.08%, while real estate was off -0.86%, energy -0.53%, and financials -0.19%. Northbound Stock Connect volumes were light as foreign investors bought $188mm of mainland stocks today.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.83 versus 6.83 yesterday

- CNY/EUR 8.09 versus 8.11 yesterday

- Yield on 1-Day Government Bond 0.76% versus 0.91% yesterday

- Yield on 10-Year Government Bond 3.13% versus 3.08%

- Yield on 10-Year China Development Bank Bond 3.69% versus 3.64% yesterday