Renminbi Rallies as Retail Sales Pick Up

3 Min. Read Time

Key News

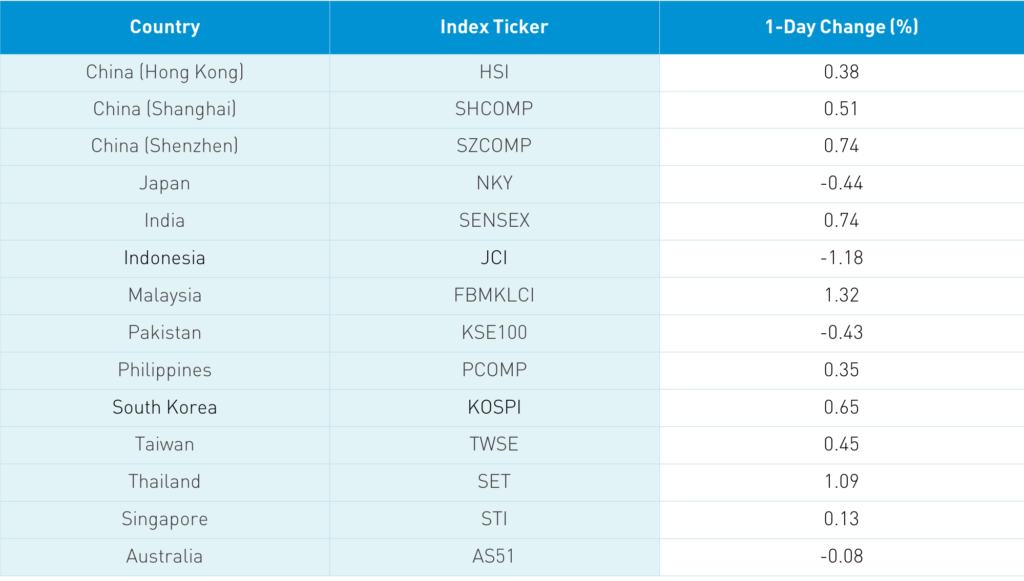

Asian equities posted modest gains overnight, while Japan was an outlier to the downside. Hong Kong and China rebounded from small declines as the August data release reconfirmed China’s V-shaped recovery with retail sales finally picking up. Hong Kong volume leaders were Xiaomi, which was off -5.1% after the founder/CEO sold $1 billion of stock, Tencent, which was flat at 0.0% after announcing Singapore will be its hub for efforts in Southeast Asia, Alibaba Hong Kong, which was down -0.3%, Ping An, which was up +1.35%, and EV bus maker BYD, which gained +12.62% as news supporting EV policies lifted autos. JD.com was up +2.72%, Meituan Dianping was off -0.41%, NetEase Hong Kong gained +1.25%, and Yum China Hong Kong gained +0.65%.

Hong Kong stocks benefited from relaxed social distancing measures, while real estate was lifted by property investment releases in Hong Kong and China. Healthcare names in both markets were lifted by reports that Chinese pharma companies should have a vaccine ready by December. Mainland China had a similar rebound post-data release, though you can see from breadth data that many small caps/micro caps with high valuations struggled today as large caps had a much better day with real estate, health care, and discretionary stocks leading the market higher. Foreign investors were net buyers of $489 million of Mainland stocks.

The offshore renminbi (ticker CNH) had a very strong move overnight, breaking the 6.80 level to 6.78! Hat tip to the HSBC team, which we noted last week put a target of 6.75. This rally is driven by US dollar weakness, though China’s economic rally explains some elements of the rebound.

This Friday will be a very high-volume day as we have Quad Witching and FTSE Russell indexes rebalance. Quad witching refers to the third Friday quarterly when stock options, stock futures, index options, and index futures expire. I am not an expert on FTSE’s index methodology, but it appears Chinese A-Shares will see an expanded coverage in FTSE indexes. More to come!

Two US-listed Chinese companies are apt to relist in Hong Kong this week. ZTO Express, an e-commerce delivery company, and Baozun, consiglieri to foreign brands selling in China, are rumored to be close to a re-listing in Hong Kong this week. This morning it was reported that Autohome is also planning to relist in Hong Kong.

Trading hours for Chinese bonds will be extended three hours beginning next Monday, September 21st. I assume this will allow more overlap with European trading hours.

Hong Kong and China equity markets were in the red prior to the 10 am data release, which provided a healthy positive pop.

Takeaway: We have discussed how online retail sales have been outperforming offline/traditional stores due to the habits formed during the quarantine. Traditional stores appear to be slowly rebounding as clothing had its first positive month year-to-date, while cosmetics and jewelry strength increased month-over-month. Restaurant sales were still off year-over-year, though the month-over-month increase to -7% from -11% is an improvement.

These are important lessons, as China is a full quarter ahead of other global economies. Industrial Production had a healthy month-over-month pick up in almost every category. It's worth noting that the broad Power Supply category saw a sharp uptick as China’s economy picks up, requiring more energy to power it. Auto manufacturing posted a 148% increase YoY, which is off month-over-month, but another sign that China’s auto industry has likely troughed. China has manufactured 5.287mm passenger vehicles year to date of which, 642,000 are electric vehicles.

What is Fixed Asset Investment (FAI)? The amount invested in “stuff” – buildings, machinery, land, etc. The FAI data shows private companies are coming back slower, which policymakers should recognize by continuing support to them. With global demand curtailed by the economic consequence of global quarantines, it isn’t that surprising to see it coming back slower. Where is investment going? Pharmaceuticals, telecom, computers, power generation, education, and healthcare.

H-Share Update

The Hang Seng gained +0.38%/+92 index points to close at 24,732 on volumes +16% from yesterday, though is still just above the 1-year average. Breadth was positive with 32 advancers and just 15 decliners. The broader Hang Seng Composite advanced gained +0.64% with 306 advancers and 141 decliners. The 204 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.54%, led by real estate +2.68%, health care +2.29%, staples +1.56%, and discretionary +1.08%, while tech lagged -0.81%, utilities-0.67%, and communication -0.11%. Southbound Connect volumes were light as Mainland investors bought $344 million of Hong Kong-listed stocks as Southbound Connect accounted for 9.1% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen gained +0.51% and +0.74% to close at 3,295 and 2,205 respectively as volume shrank -5.6%, which is below the 1-year average. Breadth was off with 1,444 advancers and 2,199 decliners micro caps underperformed. The 517 Mainland listed Chinese companies within the MSCI China All Shares Index gained +1.37%, led by discretionary +2.82%, materials +1.93%, industrials +1.92%, health care +1.84%, real estate +1.49% and financials +1.06%. Utilities lagged -0.32%. Foreign investors bought $489 million of Mainland stocks today as Northbound Stock Connect trading accounted for 5.6% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.78 versus 6.81 yesterday

- CNY/EUR 8.04 versus 8.09 yesterday

- Yield on 1-Day Government Bond 0.81% versus 0.56% yesterday

- Yield on 10-Year Government Bond 3.11% versus 3.15% yesterday

- Yield on 10-Year China Development Bank Bond 3.65% versus 3.69% yesterday