HSBC Hit With One-Two Punch

3 Min. Read Time

Key News

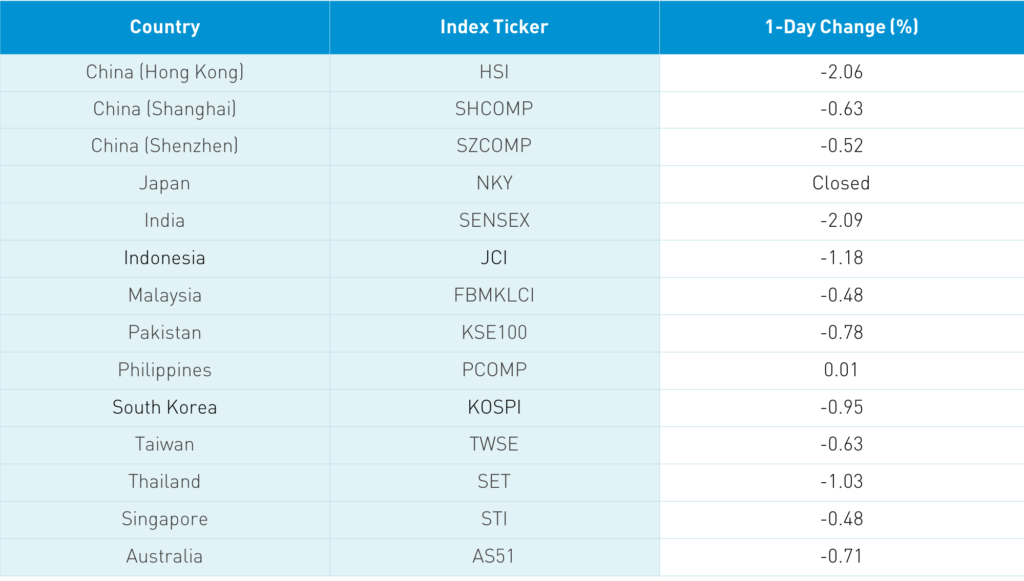

Asian equities started the week with a good, old fashioned risk-off day as everything that has been working recently such as growth beating value, a weak US dollar, and stronger commodities stopped working. Japan was spared the fun as the country celebrates Respect for the Aged Day (might need to teach my kids about this holiday…).

The TikTok deal with Oracle and Walmart was approved though I doubt this is the last episode of the saga. Meanwhile, a Federal judge blocked the White House’s WeChat ban not only on the grounds of free speech, but also because the app is often the sole means of communication between Americans and their relatives in China.

On Saturday, a Mainland media source provided an update on the Unreliable Entity List, which is China’s equivalent to US bans on Chinese companies though it hasn’t been implemented. US companies mentioned in the article to be included on the list include Apple, FedEx, Boeing, Qualcomm and Cisco in a not so subtle reminder that US shouldn’t go too far in throwing China under the bus. For the Hong Kong market, HSBC being included in the article led to a -5.33%/-88 index points drop, which accounted for almost 1/5th of the Hang Seng Index’s drop.

HSBC, which hit a 25-year low (not a typo), was also included in an article about several global banks that have been accused of ignoring internal money laundering controls for over a decade. Hong Kong volume leaders were Alibaba HK, which fell -2.82%, Tencent, which fell -1.62%, Xiaomi, which fell -6.58%, Meituan Dianping, which was flat on the day, and HSBC. NetEase HK fell -1.1%, JD.com HK fell -1.58% despite the announced spin off of JD Heath, and Yum China HK fell -3.5%.

Mainland China was off a touch as the PBOC kept the 1 and 5 year Loan Prime Rates unchanged at 3.85% and 4.65%, respectively, which had been expected as China’s V-shaped recovery has allowed the PBOC to keep its powder dry. It was a fairly uniform sell off today as volumes were light in both markets. The renminbi reversed as risk off is leading to a dollar rally. I had mentioned last week how well the renminbi was doing so of course it reverses from Wednesday’s low of 6.74 to 6.79 this morning.

Random Factoid: HSBC is neither part of the MSCI Emerging Markets Index nor is it part of the MSCI China Index due to its London headquarters, which classifies the bank as a British company.

iQIYI (IQ US) announced a partnership with the WWE to bring US wrestling to China.

Tencent is completing the takeover of streamer HUYA.

H-Share Update

The Hang Seng opened lower and continued on that path to close -2.06%/-504 index points at 23,950. Volume declined -20% from Friday to just above the 1-year average while breadth was off significantly with only 3 advancers and 47 decliners. The 204 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index fell -1.64% with every sector in the red: discretionary -1.23%, real estate -1.38%, and health care -1.4, while tech -3.73%, materials -2.38% and industrials -2.04%. Southbound Stock Connect volumes were light as Mainland investors bought a net $240 million worth of Hong Kong stocks as Southbound Connect trading accounted for 9.7% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen opened positive but slipped -0.63% and -0.52% to close at 3,316 and 2,208, respectively, as volume fell -9% from Friday, which is below the 1-year average. Breadth was off with 1,345 advancers and 2,310 decliners as large, mid and small companies were off uniformly. The 517 Mainland stocks within the MSCI China All Shares Index fell -1.26% with materials -0.58%, industrials -0.59%, energy -0.63%, discretionary -2.18%, staples -1.89%, and communication -1.85%. Northbound Stock Connect volumes were light as foreign investors sold a net -$957 million worth of Mainland stocks as Northbound Stock Connect trading accounted for 5.4% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.80 versus 6.77 Friday

- CNY/EUR 7.99 versus 8.03 Friday

- Yield on 1-Day Government Bond 1.27% versus 1.16% Friday

- Yield on 10-Year Government Bond 3.10% versus 3.12% Friday

- Yield on 10-Year China Development Bank Bond 3.65% versus 3.68% Friday