Markets’ Worry Over US Stimulus Goes Global

3 Min. Read Time

Key News

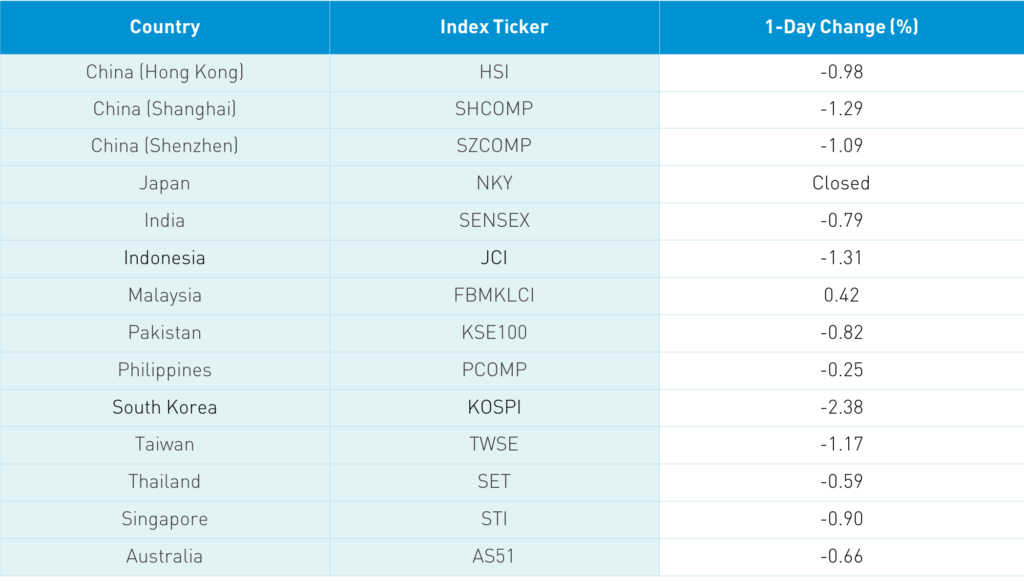

Asian equities followed US stocks south in another risk-off session, with South Korea underperforming. Concerns include that the Supreme Court nominee fight will prevent another round of fiscal stimulus pre-election, the possibility of a second wave of coronavirus wave in Europe, TikTok deal doubts/US-China political rhetoric, and the global bank money-laundering accusations. The number one issue is the lack of US stimulus due to the importance of the US economy to the global economy. Fed Chair Powell is apt to repeat the need for fiscal stimulus, though bipartisan bickering could make that difficult. Another issue is simply the lack of positive macro catalysts in the short term, though there have been several micro/individual stock catalysts.

The Hang Seng Index was off -0.98%, closing below 24,000, as HSBC was off -2.05% because of the money-laundering accusations and yesterday’s news that it could be added to China’s unreliable entity list. Standard Chartered was off -2.29% on the money-laundering accusations as well. Hong Kong volume leaders were Tencent, which was off -0.97%, and Alibaba Hong Kong, which was up +1.07%, Xiaomi, which was down -0.73%, and Meituan Dianping, which gained +0.41%. Bottled water company Nongfu Spring gained +1.94% after being added to Southbound Connect today. BYD jumped +3.91% on talk of an electric vehicle (EV) deal with Daimler, while NetEase rose +1.99% on new game approval and chatter that investors are rotating to gaming company from Tencent following the US’ inquiry on its Epic and Riot Games stakes. I don’t think that this will be an issue since the companies operate independently, and Tencent’s WePay mobile payment unit is a duopoly with Ant Group. Tencent has been highlighting the latter over the last week or two. JD.com also bucked the trend, gaining +0.97% as the IPO of JD Health will benefit the company. Macau casino stocks were off on concerns that Golden Week tourist reservations appear to be light. Macau casino stocks, such as HSBC and Standard Chartered, are not considered Chinese companies due to their headquarter domiciles.

Mainland China was risk-off as healthcare stocks were the only sector in the green. Material and energy stocks were hit especially hard as gold, copper, and oil prices declined. Liquidity is apt to tighten as we head towards Golden Week and tourists free up some spending cash. One factor on today’s weakness could be the Mainland’s robust IPO market. Three companies went public today and four Mainland ETFs benchmarked to the STAR Board started fundraising. Mainland media noted policymakers' comments on raising e-commerce. Shanghai and Shenzhen Composite Indexes are approaching key support levels of 3,200 and 2,100 respectively.

This Thursday, September 24th, FTSE will announce whether Chinese government bonds will be added to the World Government Bond Index (WGBI). There are several premier fixed income benchmarks, including the Bloomberg Barclays Global and US Aggregate indexes, the JP Morgan Emerging Market Bond Index, and the World Government Bond Index (WGBI). Overnight, regulators proposed loosening restrictions on foreign bond investors’ currency transactions and hedging abilities, while Hong Kong Exchange CEO Charles Li said that listing bond futures would happen. It's hard for me to imagine that FTSE wouldn’t add Chinese bonds as Bond Connect volumes continue to increase.

China’s currency appears to have regained its footing after slipping a touch in the recent dollar rally.

Great quote from an institutional broker yesterday: “When they’re cryin’ you should be buyin’. When they’re yellin’ you should be sellin’.”

H-Share Update

The Hang Seng opened lower and stayed there, off -0.98%/-233 index points to close at 23,716 as volume declined -7%, which is below the 1-year average. Breadth was awful with 3 advancers and 45 decliners. The 204 Chinese companies listed in Hong Kong were off -0.83%, with utilities +0.2%, staples +0.06% and tech +0.36%, while materials -2.32%, energy -1.85%, industrials -1.51%, health care -1.4% and communication -0.94%. Southbound Stock Connect volumes were light in mixed trading as Mainland investors sold $77mm of Hong Kong stocks. Southbound Stock Connect trading accounted for 11.2% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen were off all day at -1.29% and -1.09%, closing at 3,274 and 2,184. Volumes were off -7%, which is below the 1-year average. Breadth was awful with only 637 advancers and 3,087 decliners. The 517 Chinese stocks within the MSCI China All Shares Index were off -1.01%, led by healthcare +0.55%, staple -0.57%, and financials -0.92%. Laggards were materials -2.62%, energy -1.72%, industrials -1.72%, discretionary -1.36%, utilities -1.18%, communication -1.13%, tech -1.08% and real estate -1.07%. Northbound Stock Connect volumes were light. Shanghai activity was net outflow while Shenzhen activity was net inflow. Foreign investors sold -$295mm of Mainland stocks today as Northbound Stock Connect trading accounted for 5.6% of Mainland trading.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.77 versus 6.81 yesterday

- CNY/EUR 7.97 versus 7.99 yesterday

- Yield on 1-Day Government Bond 1.35% versus 1.27% yesterday

- Yield on 10-Year Government Bond 3.09% versus 3.10% yesterday

- Yield on 10-Year China Development Bank Bond 3.65% versus 3.65% yesterday