Working From Home or Cocooning?

3 Min. Read Time

Key News

Asian equities had a mixed day as Australia outperformed and Japan posted small losses after coming back from market holidays on Monday and Tuesday. It was a relatively quiet night on the news front. Volumes were generally light as things get eerily quiet prior to the coming early October holidays. Hong Kong and Mainland China managed small gains as growth stocks, which had been kicked to the curb, were back in vogue overnight. Hong Kong volume leaders were Tencent, which rose +0.49%, Alibaba HK, which rose +0.83%, Meituan Dianping, which rose +3.05%, HSBC, which rose +0.17% after having been down -4% intra-day, Xiaomi, which rose +1.96%, bottled water company Nongfu Spring, which rose +7.08%, and recent IPO Joy Spreader Interactive Technology, which soared +62%.

Healthcare stocks had a strong day in both Hong Kong and Mainland China on fears of a second wave and a recent rise in coronavirus cases globally. According to my friend William and his colleagues in Shanghai at Everbright Securities, there are three Chinese pharma companies conducting human trials on four vaccines. However, none of this makes a headline here, which seems odd to me. Growth sectors, which are mainly mid/small caps, had a strong day in the Mainland market as well. Alcohol stocks were off with Kweichow Moutai down by -0.94% and Wuliangye Yibin down by -1.61% after they were told not to raise prices going into Golden Week holiday. Firms continue to raise funds to participate in Ant Group’s coming IPO in both Hong Kong and on Shanghai’s STAR Board.

Goldman Sachs’ target on the renminbi versus the US dollar is 6.50 over the next twelve months. Goldman’s co-head of Asia macro and Chief Asia-Pacific strategist Timothy Moe stated that “Historical evidence is very, very clear that a strengthening currency is generally supportive for the equity market.”

Nike’s geographic revenue percent changes year over year: North America -2%, Europe/Middle East/Africa +5%, China +6%, Asia Pac/Latin America -18%.

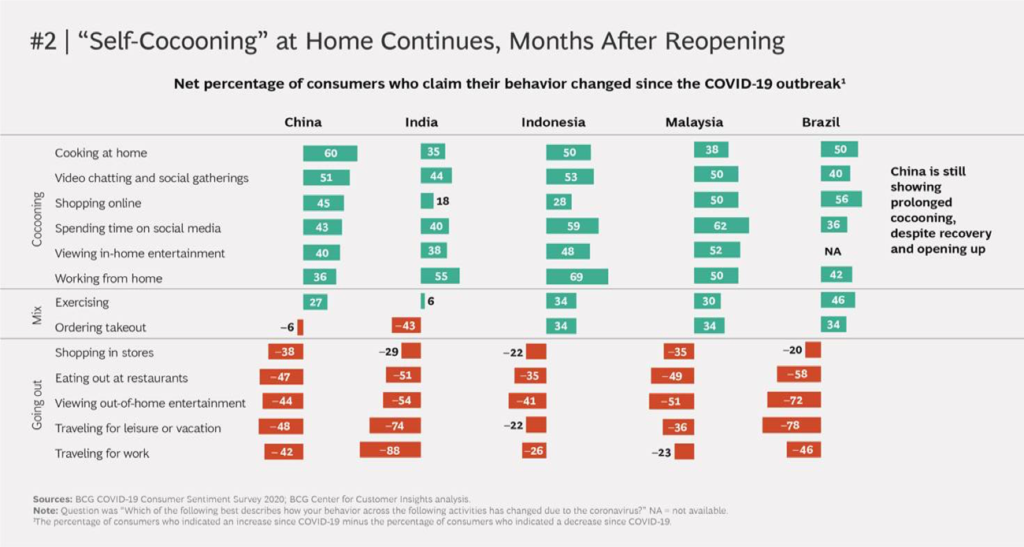

Boston Consulting Group recently released a very interesting survey of emerging markets consumers. A key takeaway across China, India, Indonesia, Malaysia and Brazil was that consumers currently prefer “cocooning,” i.e. staying at home, over “going out” activities. Emphasis has been on Work From Home, but it appears that there is more to it. Another insight was the pickup in first-time users of e-commerce, e-learning, on-demand video, and mobile payments. We have spoken to the divergence as China’s e-commerce sales have seen a nice rebound while brick-and-mortar stores have come back much slower. It is very clear from the BCG data that the divergence has continued as the habits formed in quarantine are sticking. While China was the first in and first out with regard to coronavirus, there is an interesting lesson for investors to take note of here. It appears that restaurants, stores and traveling may not come back fully until a cure or vaccine is available.

H-Share Update

The Hang Seng bounced around the room to close +0.11%/+25 index points at 23,742 as volume fell -7% and breadth was positive with 25 advancers to 24 decliners. The 204 Chinese stocks within the MSCI China All Shares Index gained +0.32% with discretionary +2.49%, health care +1.99%, and tech +1.41% while laggards included energy -1.33%, financials -1.16%, and utilities -0.75%. Southbound Stock Connect volumes were light as mainland investors bought $214 million worth of Hong Kong stocks today as Southbound Connect trading accounted for 9.8% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen had a choppy morning though managed to gain +0.17% and +0.83% to close at 3,279 and 2,202, respectively. Volume was off -6% while breadth was positive with 2,338 advancers and 1,236 decliners. The 517 Mainland stocks within the MSCI China All Shares Index gained +0.35% led by heath care +2.77%, discretionary +1.52%, communication +1.41%, and tech +1.03%, while real estate -0.93%, financials -0.72%, and materials -0.54%. Northbound Stock Connect volumes were light as foreign investors sold -$405 million worth of Mainland stocks and Northbound Connect accounted for 5.6% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.80 versus 6.78 yesterday

- CNY/EUR 7.95 versus 7.94 yesterday

- Yield on 1-Day Government Bond 0.95% versus 1.35% yesterday

- Yield on 10-Year Government Bond 3.09% versus 3.09% yesterday

- Yield on 10-Year China Development Bank Bond 3.68% versus 3.65% yesterday

- China's Copper Price Change -0.35%