ZTO Express and Baozun Relist in Hong Kong

4 Min. Read Time

We will host a webinar next Tuesday, October 6th at 11:00am EST with NASDAQ Dorsey Wright on Positioning your China Allocation for Strategic Risk Management.

Click here to register.

Key News

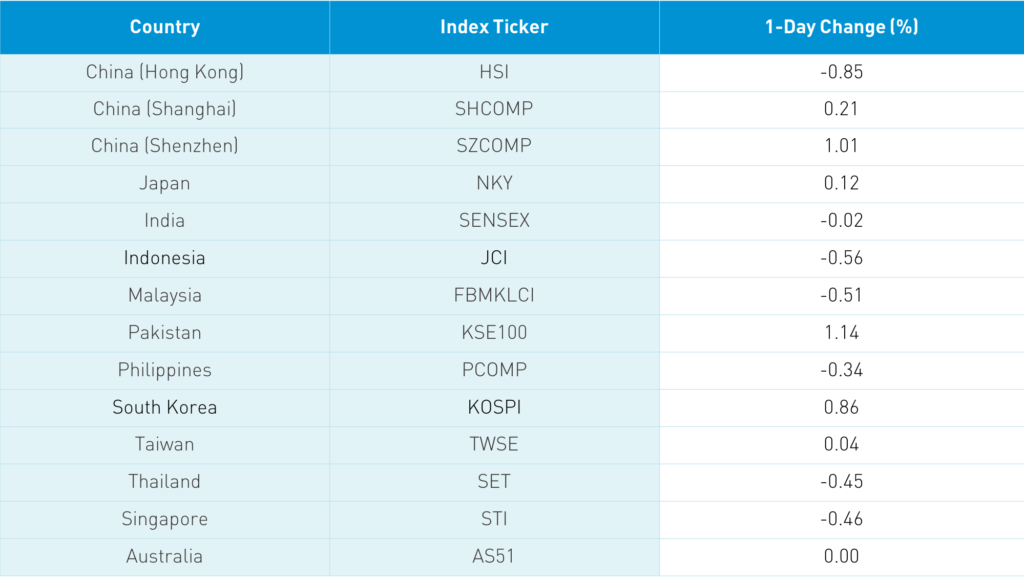

Asian equities were mixed and volumes were off as traders appeared distracted by the upcoming holiday season. The big news regionally was that Japan’s mobile phone giant NTT Docomo is being taken private by parent company Nippon Telegraph & Telephone in a $40 billion deal.

In Hong Kong, The Hang Seng was off a touch in very light volumes as we had two companies currently listed in the US relist locally: ZTO (2057 HK) and Baozun (9991 HK), which rose +9.17% and +1.33%, respectively. Hong Kong volume leaders were Tencent, which was off -0.1%, Alibaba Hong Kong, which was up +0.76% as the company’s investor conference finished day two today with positive analyst reports, AIA Insurance, which was off -1.1%, Ping An Insurance, which was off -0.81%, Xiaomi, which was off -0.74%, and HSBC, easing -2.6% after yesterday’s rally. JD.com Hong Kong was up +1.79% on chatter from the BABA investor day that noted increased competition for the giant. NetEase Hong Kong was off -0.35% and Yum China Hong Kong was up +1.21%. The Hong Kong Exchange was off -0.44% as legendary CEO Charles Li announced his retirement at year-end.

Financials were weak on chatter that companies with online insurance businesses will have to obtain a license and that mortgage lending rules will be tightened to curb speculation. Financials’ weakness is a problem for many Chinese benchmarks due to its high weight, such as the Hang Seng Index (44% financials) and Mainland benchmark CSI 300 (28% financials). The MSCI China All Shares Index (Hong Kong, Mainland, and US stocks) has a financial weight of just 16%, while the Mainland benchmark the MSCI China A Index has a financials weight of 22%.

Mainland China had a day defined by growth stocks outperforming with the Shenzhen Composite up +1.01%, while the financial-heavy Shanghai Composite lagged (28.9% financials). Foreign investors pivoted away from Shanghai Connect, which had an outflow of RMB 2.784B ($408mm) while Shenzhen Connect had an inflow of RMB 2.690 ($394mm). Domestic oriented growth sectors outperformed as chatter is picking up on the month-end policy meetings discussed further below. It's been fairly quiet on the US-China political rhetoric front as the US election could pivot toward domestic issues. Bloomberg noted that both the WeChat and TikTok download bans were blocked in separate rulings due to a failure to prove the apps are security threats.

Loosened restrictions on QFII, the foreign investment access program that has largely been replaced by Stock Connect, were the topic du jour among several brokers. The process for applying for access has been streamlined and the types of investments have been expanded to include private equity, commodity futures, equity index options, bond futures, and the NEEQ, which is China’s version of the pink sheets. Want to hear something crazy? There are no single stock options in China! There are equity index options and ETF options, but no stock options. Also mentioned was securities lending, which is interesting since shorting is very limited in China. I don’t see the band-aid being ripped off on this issue.

South China Morning Post had a good piece, noting that China’s policymakers will meet in Beijing on October 26th to review the next Five Year Plan which will be implemented in 2021. Investors expect health care, 5G, and tech to be emphasized in the plan. Another topic is “dual circulation”, which refers to the emphasis on raising the domestic economy after previously implementing an effort to globalize the economy. We won’t see the 14th Five Year Plan until next year, though there will be plenty of chatter on favored economic sectors as investors will want to align themselves with the top-down economic policy.

Weibo (WB US), the Twitter of China, reported Q2 results yesterday. While revenues were off -10% year-over-year to $387mm, Weibo added 37 million (just less than the population of California) new monthly users, bringing the total users to 523 million. The company also showed discipline by cutting expenses, which led to a jump in net income from $103mm to $198mm. Non-GAAP diluted EPS was $0.50 versus $0.68 in Q22019.

- South Korea – Closed Wednesday, Thursday, and Friday

- Taiwan – Closed Thursday and Friday

- India – Closed Friday

- Hong Kong – Closed Thursday and Friday

- China – Closed Thursday and Friday until Friday 10/9/2020

H-Share Update

The Hang Seng opened higher but slid lower to close down -0.85%/-200 index points to 23,275 as volume dipped -8%, which is well below the 1-year average. Breadth was off with 13 advancers and 37 decliners. The 204 Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -0.63%, with tech up +0.24% and energy up+0.03%, while utilities -2.13%, financials -1.49%, real estate -1.48%, and materials -1.09%. Southbound Stock Connect was closed today.,

A-Share Update

Shanghai & Shenzhen rallied in the morning and stayed higher at +0.21% and +1.01% at 3,224 and 2,148 respectively, as volume was up +1.3%, though was still well below the 1-year average. Breadth was positive with 2,670 advancers and 983 decliners. The 517 Mainland Chinese companies within the MSCI China All Shares Index were up +0.51%, led by tech +1.36%, industrials +1.26%, health care +1.18% while financials were off -0.63%, real estate -0.37%, and energy -0.14%. Northbound Stock Connect volumes were light as foreign investors sold Shanghai stocks and bought Shenzhen listed stocks. Foreign investors sold $13mm of Mainland stocks today as Northbound Connect trading accounted for 6.9% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.81 versus 6.81

- CNY/EUR 8.00 versus 7.94 yesterday

- Yield on 1-Day Government Bond 0.76% versus 0.45% yesterday

- Yield on 10-Year Government Bond 3.13% versus 3.11% yesterday

- Yield on 10-Year China Development Bank Bond 3.71% versus 3.69% yesterday