China’s Trade Data & Car Sales Lift Mainland Stocks

2 Min. Read Time

Key News

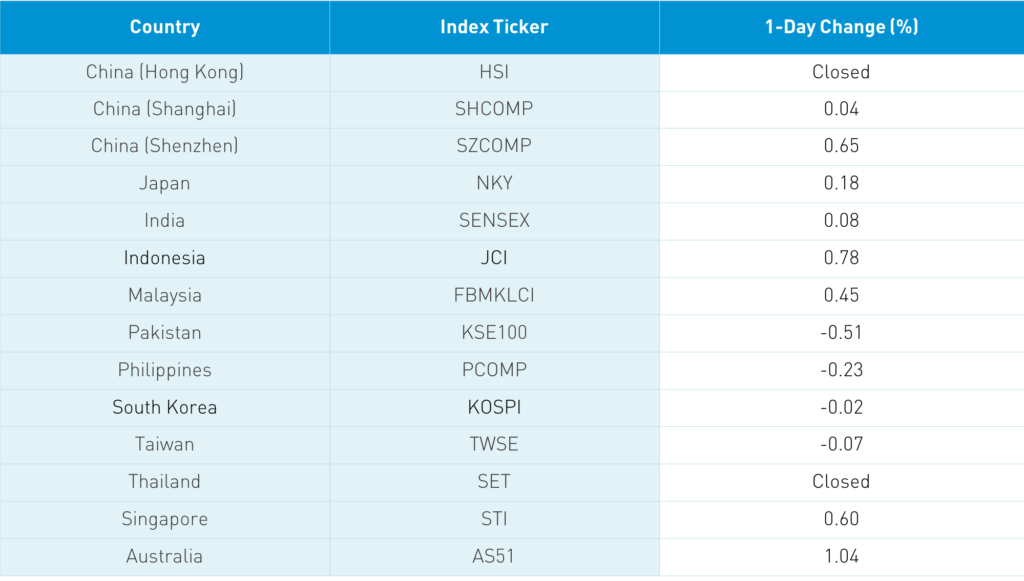

Asian equities had modest night moves as Hong Kong and Stock Connect trading was canceled due to Typhoon Nangka. Mainland China posted small gains as the market cheered the trade data release while autos had a strong day lifting discretionary stocks. BYD (002594 CH) was up +0.61% as the company raised its profit outlook. GM’s China partner SAIC (600104 CH) rose +2.84% following GM’s announcement yesterday that it sold 771,400 vehicles in China during Q3 2020, which is up +12% versus Q3 2019. According to Bloomberg, the China Passenger Car Association reported overnight that September car and vehicle data rose +7.4% to 1.94mm units. A Mainland media source noted that September EV sales were double year-over-year. Financials were off as two brokerage firms canceled a proposed merger after failing to agree on terms. Tonight we have President Xi’s speech in Shenzhen, which could be a strong catalyst for the market as financial and technology policies are apt to be articulated.

Reuters is reporting that Ant Group’s IPO has been slowed due to regulators looking at the company’s role in selling mutual funds focused on its IPO. I’ve not heard this elsewhere, though one broker reported the company saying that its IPO was moving along. With Hong Kong closed overnight, the news flow was light. I don’t foresee this being an issue as China is coming back online post-Golden Week holiday. I expect a virtual roadshow will kick off next week with the last week of October or early November listing.

A Mainland media source noted that 9mm residents of Qingdao were tested after six residents tested positive for coronavirus. Remarkable.

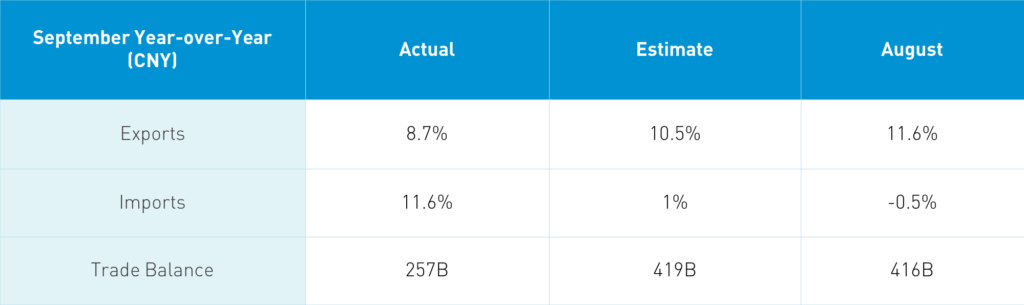

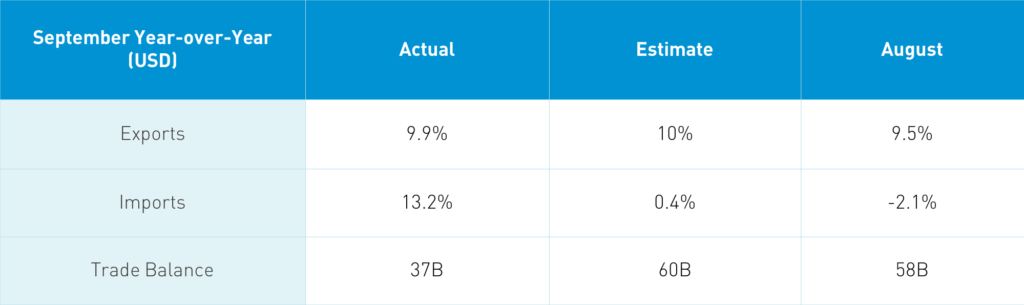

Chian's September trade data was released.

Takeaway: The numbers speak for themselves as export and imports all had a nice pickup month-over-month and year-over-year. As the middleman in global trade, China provides a great indication of the global economy. WSJ notes that demand for Chinese medical gear and drugs is a driver of exports, along with global demand for computers due to work from home activity. A Mainland media source noted that exports of medical instruments and devices increased +48% year-over-year, drugs and medical materials increased +21.8%, and laptops increased +17.6%. Commodity imports were largely firmer year-over-year and month-over-month as an element of China stimulus will be infrastructure-related.

Our friend William of Everbright Securities provided great insight on the strong technology imports from the US and Taiwan, as Chinese companies might be stockpiling in case US tech export restrictions are raised. Imports from the US rose +24.7% year-over-year versus exports, which rose +20.5%, though the value of imports was $13B versus $43B of exports. Without question, the US is China’s largest export destination, though one interesting takeaway from the data is how important Southeast Asia and Europe Union are to China, as it exported $34B to Asean countries and $34B to the EU. Ultimately the data is further confirmation of China’s V-shaped recovery.

H-Share Update

Hong Kong markets are closed due to Typhoon Nangka.

A-Share Update

Shanghai and Shenzhen overcame morning losses to close up +0.04% and +0.65% at 3,359 and 2,304 respectively. Volume slumped 14% from Monday, though still above the 1-year average. Breadth was off with 1,430 advancers and 2,263 decliners. The 517 Mainland stocks within the MSCI China All Shares Index gained +0.24%, led by discretionary +0.85%, staples +0.79%, health care +0.77%, and materials +0.71%. Real estate and financials lagged -0.89% and -0.43%.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.74 versus 6.75 yesterday

- CNY/EUR 7.93 versus 7.97 yesterday

- Yield on 1-Day Government Bond 1.00% versus 1.05% yesterday

- Yield on 10-Year Government Bond 3.20% versus 3.19% yesterday

- Yield on 10-Year China Development Bank Bond 3.74% versus 3.74% yesterday