Hong Kong Growth Names Gallop, China’s Post-Close Economic Release Surprises To Upside

2 Min. Read Time

Key News

Asian equities had a quiet night with no big moves up or down. Unfortunately, Apple’s iPhone release failed to ignite its Asia supply chain and President Xi’s Shenzhen speech celebrating the city’s 40-year anniversary of becoming a special economic zone status was not as specific as I had hoped.

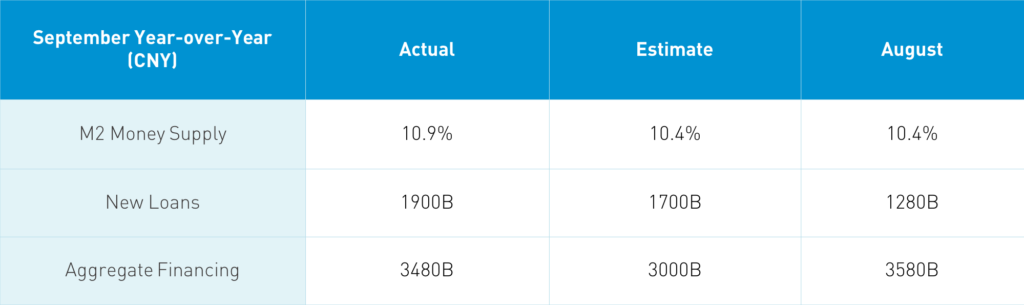

China released September loan data after the close overnight:

Takeaway: Most importantly, the release occured AFTER the market close.

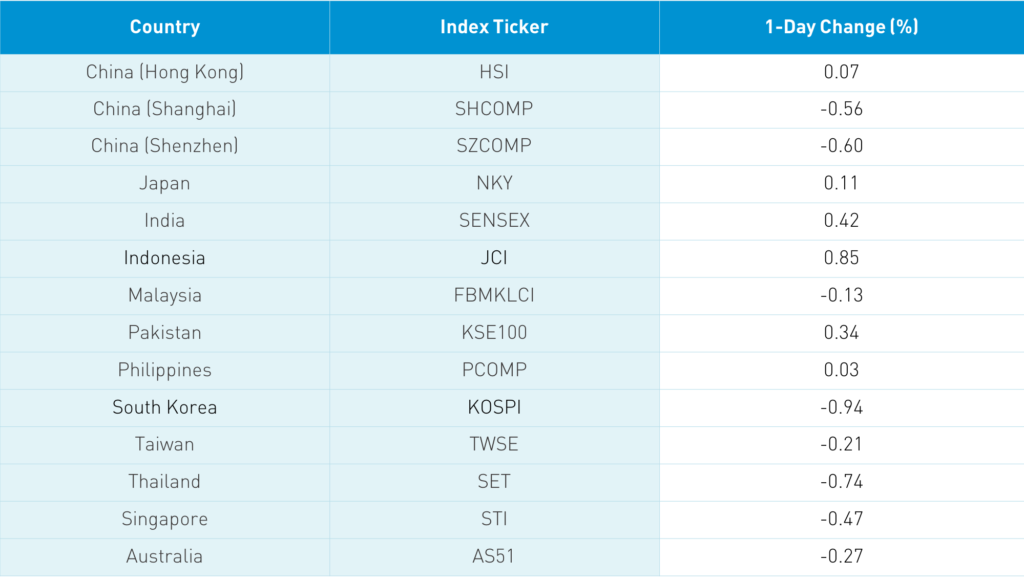

The Hang Seng Index pulled a James Bond gaining +0.07% but popping the hood shows a weak day in terms of breadth, i.e. stocks advancing versus declining, as growth stocks outperformed significantly. Hong Kong volume leaders where Tencent, which rose +2.96% following the highlighting of its League of Legends video game during the iPhone 12 release, Alibaba HK, which rose +1.92%, Meituan Dianping, which rose +1.16%, Xiaomi, which rose +2.42%, and Ping An Insurance, which rose +0.55%.

After the market close, Bloomberg reported that Tencent is raising its stake in Universal Music to 20%. Meanwhile, real estate giant Evergrande (3333 HK) cratered -16.9% after selling shares at a deep discount to raise cash, weighing on the real estate sector. Auto names such as BYD, which gained +4.26%, and Great Wall, which rose +10%, were standouts as investors seem to be recognizing the recent pick up in China auto sales. Macau casino stocks are being taken to the wood shed as poor Golden Week visitors were combined with the potential for new regulations on casino promotions in China. Mainland stocks had a quiet day as recent outperformers were hit with profit taking. Clean energy stocks had a strong day as chatter on solar and wind energy’s role in the drafting of the new Five Year Plan pervaded broker discussion.

Sell-side analysts are having their pre-quiet period talks with US and Hong Kong-listed Chinese internet and e-commerce companies before they report Q3 results in November. How are the talks going? You might have noticed price targets being raised, which is a strong indication that analysts came away with a good feeling.

Want a data driven analysis of the US election without personal biases? Check out the discussion between Larry McDonald (@Convertbond) and David Metzner (@davidametzner) of ACG Analytics on Twitter that was released last night. This has nothing to do with China, but I found it fascinating how close the election is likely to be.

A test of China’s digital currency has begun in Shenzhen. 50,000 residents were issued RMB 200 worth of the digital currency to be used at over 3,000 retail outlets. China’s is the first central bank to issue such a currency.

H-Share Update

The Hang Seng traded in a tight range closing +0.07%/+17 index points at 24,667. Volumes were +10% from Monday while breadth was off with 21 advancers and 27 decliners. The broader Hang Seng Composite Index gained +0.14% with 166 advancers and 289 decliners. The 204 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +0.66% led by communication +2.62%, utilities +2.06%, discretionary +1%, tech +0.82% and staples +0.46%. Laggards included real estate -2.65%, energy -2.51%, materials -1.84%, health care -1.38%, and industrials -0.83%. Southbound Connect volumes were light as Mainland investors bought $895mm worth of Hong Kong stocks as Southbound Connect trading accounted for 11% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen declined -0.56% and -0.6% to close at 3,340 and 2,290, respectively. Volume was basically flat from yesterday while breadth was off with 1,069 advancers and 2,707 decliners. The 517 Mainland stocks within the MSCI China All Shares Index fell -0.52%. Industrials gained +0.24% while tech -1.92%, real estate -1.15%, energy -0.71% and staples -0.61%. Northbound Stock volumes were moderate as foreign investors sold -$231 million worth of Mainland stocks as Northbound Stock Connect accounted for 7.3% of Mainland turnover.

Last Night’s Prices & Yields

- CNY/USD 6.72 versus 6.75 yesterday

- CNY/EUR 7.90 versus 7.92 yesterday

- Yield on 1-Day Government Bond 1.10% versus 1.10% yesterday

- Yield on 10-Year Government Bond 3.22% versus 3.20% yesterday

- Yield on 10-Year China Development Bank Bond 3.77% versus 3.74% yesterday