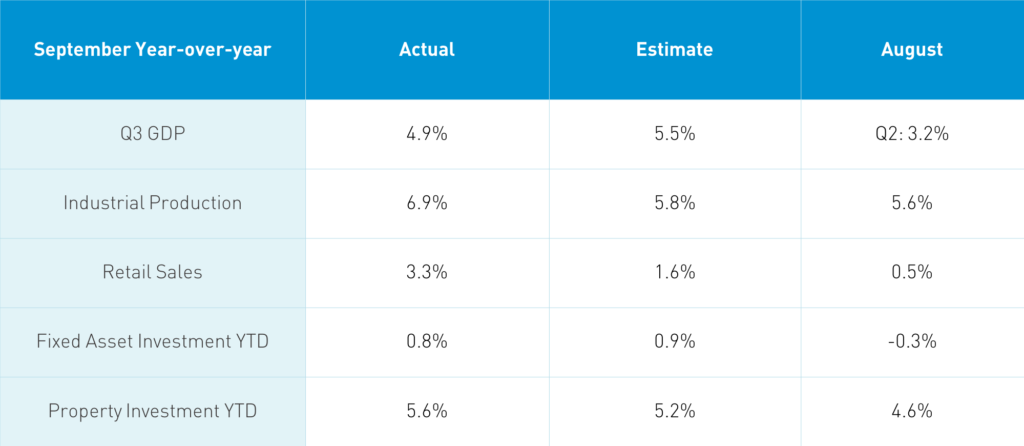

Q3 GDP, Industrial Production, & Retail Sales Mostly Positive

4 Min. Read Time

Key News

Asian equities had a positive start to the week though Mainland China was off. If the data was so good why did the market come down? GDP garners a large amount of attention and missed estimates though the remainder of the data was quite strong. Headlines at the time of the release screamed “GDP misses”, “GDP weaker”. Unfortunately, this narrative won the day though upon further examination headlines have downplayed the GDP miss. It is worth noting that many of China’s trade partners went up on the news.

Takeaway: The release came at 10 am local time and took the wind out of Mainland equities. GDP missed expectations, overshadowing an otherwise strong release. The release reconfirms not only China’s V-shaped recovery, but also themes we have discussed repeatedly such as e-commerce, health care and autos/EVs.

Within the GDP data, the manufacturing and service industries flipped into positive territory from -1.9% and -1.6% in Q2 to +0.9% and +0.4% in Q3. Manufacturing saw a strong uptick +7.6% year over year (YoY). It is also worth noting that pharmaceutical manufacturing picked up 7% YoY and auto manufacturing +16.4% YoY. Industrial Production beat expectations with a broad pick up across segments. It is worth noting that output of cars grew +3% YoY to 925,000 cars while EV picked up 51.1% to 136,000.

Retail Sales increased YoY and month over month from RMB 3.357 trillion to 3.530 trillion with restaurant sales still negative -2.9% YoY, but slowly and steadily picking up. Auto sales were up 11% YoY while beverages and tobacco/alcohol saw large month over month gains. Online retail sales of physical goods rose to 24.3% of total retail sales of consumer goods. Only to be found deep in the data release, disposable income came in a touch weaker. Fixed Asset Investment YTD finally reached positive territory as private companies are coming back more slowly than State Owned Enterprises. Private companies’ slow recovery shows in manufacturing (secondary sector), which fell -3.4%, while the services sector (the tertiary sector) accelerated along with agriculture (primary sector). It is worth noting that pharmaceutical, telecommunication/computers, and healthcare saw strong gains YoY and month over month.

Shanghai and Shenzhen have been in the same range since July and need a strong catalyst to punch through the resistance level. Hong Kong came off its intra-day high but ended positive with the Hang Seng Index closing up +0.64% though the broader Hang Seng Composite was up only +0.03% with fairly weak breadth.

Financials, which comprise 44% of the Hang Seng Index, had a strong day, which explains the divergence. Hong Kong volume leaders were China Construction Bank, which rose +1.8%, Alibaba HK, which rose +1.09% on news that the company is buying retailer SunArt Retail Group (6808 HK), shares of which rose +19.17%overnight, in a cash deal, Tencent, which rose +0.81%, Meituan Dianping, which fell -2.56%, Xiaomi, which fell -4.1% on several analyst downgrades, and Ping An Insurance, which rose +0.9%. Mainland equities were softer as leading sectors were clipped following broker chatter that the Mainland is taking a breather though macro tailwinds persist.

A Mainland broker is reporting that the CSRC, China’s mainland regulator, has approved Ant Group’s Hong Kong listing though there has been no news on the listing from the SFC, Hong Kong’s regulator, as of yet.

After college I lived in NYC with a good friend who was a trader at a well-known Wall Street firm. One night he was talking about how much C he traded that day. “C had big blocks, C traded up, C traded down, C was trading like crazy.” After hearing about C so often, I asked him if he meant Citigroup as its ticker is C? He shrugged his shoulders. He did not know or care that C was Citigroup’s stock. It made me think about how technical analysis removes the emotion from investing. Chart going up…buy it! Chart going down…sell it! For investing in China, technical analysis takes on a greater importance as we are constantly bombarded with negative headlines. Some of them scare me candidly! I always check CNH to see if the headline has any bite to it. Ultimately, the benefit of technical analysis is that it removes the headlines from our investment decision making progress.

Whenever a portfolio company files a regulatory document with the SEC on a Friday after the market’s close, I take a deep breath prior to opening. Filing such a document Friday after the market close is often a weak attempt by a given publicly traded company to provide bad news with the hope that it will be forgotten over the weekend. After my initial trepidation, I was pleasantly surprised by TAL Education’s (TAL US) Friday at 4:18 SEC filing as the online education firm updated its 2020 Share Incentive Program i.e. stock awards for employees. Corporate governance has often been an issue for those looking to invest in China. But, the times they are a changing as employees at many tech companies want to work hard and be rewarded for it, which is as true in China as it is here. Kudos to TAL’s management for aligning employee and shareholder interests.

H-Share Update

The Hang Seng came off morning highs a touch, but closed +0.64%/+155 index points at 24,542. Volume was up +8% versus Friday, which is above the 1-year average while breadth was positive with 36 advancers and 13 decliners. The 204 Chinese companies listed in Hong Kong gained +0.05% led by utilities +3.47%, financials +1.4% and communication +0.73%. Meanwhile, health care -2.05%, discretionary -1.78%, tech -1.4%, and industrials -1.04%. Southbound Connect volumes were light/moderate as Mainland investors bought $334 million worth of Hong Kong stocks as Southbound trading accounted for 10.9% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen opened higher but reversed following the economic data release falling -0.71% and -0.7% to close at 3,312 and 2,249, respectively. Volume was up +4% from Friday, which is below the 1-year average, while breadth was off with 1,281 advancers and 2,360 decliners. The 517 Mainland stocks within the MSCI China All Shares Index fell -0.63% with financials and materials gaining a mere +0.04% and +0.05%, while health care -2.34%, staples -1.13%, and industrials -0.4%. Northbound Stock Connect volumes were light/moderate as foreign investors sold -$485 million worth of Mainland stocks today as Northbound trading accounted for 6.2% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.68 versus 6.98 Friday

- CNY/EUR 7.85 versus 7.88 Friday

- Yield on 1-Day Government Bond 1.25% versus 1.25% Friday

- Yield on 10-Year Government Bond 3.20% versus 3.22% Friday

- Yield on 10-Year China Development Bank Bond 3.74% versus 3.74% Friday