Markets Remain Rangebound, Ant Group IPO Listing Date Looms, Week In Review

3 Min. Read Time

Week in Review

- September and Q3 economic data was released Monday. China's GDP grew by 4.9% in Q3, missing the estimated 5.5%. Meanwhile, industrial production and retail sales grew by 6.9% and 3.3%, respectively, compared to estimates of 5.8% and 1.6%, in September.

- China's currency has been the best performing in Asia so far this year. As of Tuesday, CNY has gained 6.76% against the US dollar since its May 27th high of 7.16 per dollar, closing Tuesday at 6.68.

- Healthcare was a strong performer on Wednesday in both Hong Kong and the Mainland following news from the Mainland that strong progress is being made on a coronavirus vaccine with 13 different trials taking place, four of which involve human testing.

- On Thursday, Ant Group's updated, 740-page Hong Kong filing was released. Chatter is that the IPO could happen as soon as late next week. Check out Thursday's post for a review of the latest filing.

Key News

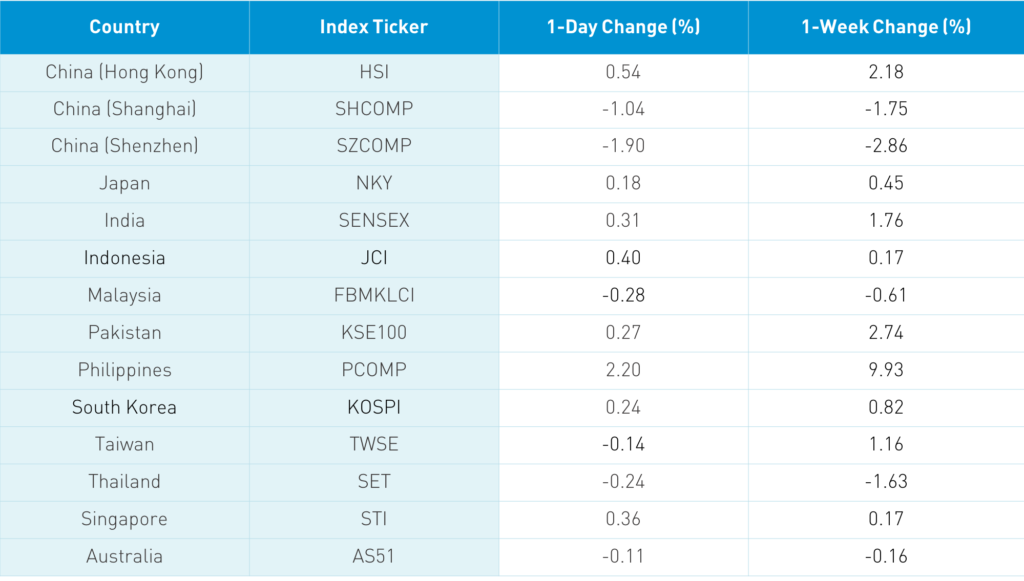

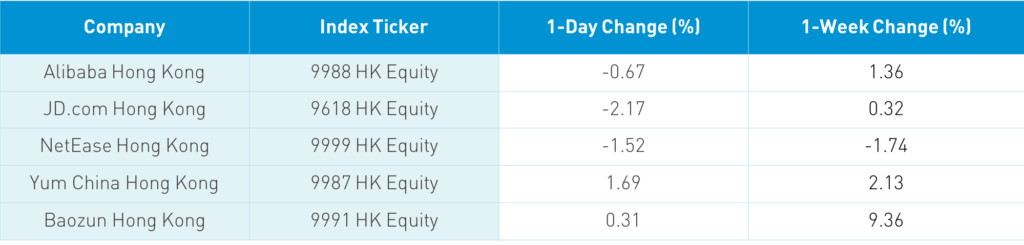

Asian equities posted modest gains today and for the week while Mainland China underperformed. The Hang Seng Index overcame morning losses to gain +0.54% as it climbs toward the 25k level though the broader Hang Seng Composite was off -0.08% and the Chinese companies listed in Hong Kong within the MSCI China All Shares fell -0.21% overall. Hong Kong volume leaders overnight included Ping An Insurance, which gained +2.31% on news that online lender Lufax Holdings, in which the company had invested, will pursue an IPO on the NYSE. The rest of the volume leaders were Alibaba HK, which fell -0.67%, Tencent, which fell -0.35%, Meituan Dianping, which fell -2.45%, BYD, which cratered -6.66%, HSBC, which gained +3.2%, Xiaomi, which fell -2.24%, China Construction Bank, which gained +0.17%, and ICBC Bank, which gained +1.27%. Value sectors performed well, driven by earnings from energy giant CNOOC, China Petroleum, which gained +6.67%, and China Telecom, which gained +3.24% while growth sectors/stocks were clipped.

One reason for growth stocks’ weakness could be a need to raise capital for the Ant Group IPO. Mainland China equities were off today in what was an off week as markets were up in the morning but sold off in the afternoon. However, there was little color on what drove the afternoon sell off as winners were clipped.

There was some chatter that a steeper yield curve will benefit financials in the US, though that does not apply in China. Investors appear to be waiting on the outcome of the US election, next week’s Five Year Plan drafting, and the Ant Group IPO. Northbound Stock Connect was closed today due to Hong Kong’s holiday Monday as foreign investors sold $2.1 billion worth of Mainland equities, bringing the YTD total to $13.98 billion.

Ant Group IPO date is a moving target as some say next Friday while a Mainland broker said Friday, November 6th. I continue to go through the Ant Group filing and I will report my key takeaways on Monday.

The debate and the Giants/Eagles game were distractions last night. Giants were up by 11 with five minutes left so I flipped to the debate. I flipped back a few minutes later and they had lost! Do not get me started on the sorry state of New York sports!

There was news that the ETF Connect appears to be launching in a small pilot program. First, we had Stock Connect followed by Bond Connect, which allows foreign investors to access Mainland markets via the Hong Kong Exchange. This allows investors to utilize Hong Kong brokers and custodians to trade stocks and bonds listed onshore. It is also a two-way street as Connect also allows Mainland investors to access the Hong Kong market. I’m diving into the details and will report back Monday. Along with the Lufax IPO filing, I have a lot of reading to do this weekend!

H-Share Update

The Hang Seng overcame morning losses to close +0.54%/+132 index points at 24,918. Volume was up +4%, placing it at just below the 1-year average while breadth was positive with 28 advancers and 19 decliners. The 204 Chinese stocks listed in the Mainland were off -0.21% as energy +5.91%, financials +1.28%, and utilities +0.29%. Meanwhile, health care -2.02%, discretionary -2.02%, materials -1.62%, tech -1.52%, stales -1.18% and communication -0.2%. Southbound Stock Connect volumes were light as Mainland investors bought $465 million worth of Hong Kong stocks today as Southbound Connect trading accounted for 11% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen were up in the morning but sold off to close down -1.25% and -1.05% at 3,278 and 2,200, respectively. Volume was up +3%, placing it below the 1-year average while breadth was off with 760 advancers and 2,953 decliners. The 517 Mainland stocks within the MSCI China All Shares Index lost -1.52%, led lower by health care -3.18%, communication -2.48%, staples-2.44%, tech -1.82%, industrials -1.66%, discretionary -1.32%, utilities -1.11%, and materials -0.81%. Northbound Stock Connect is closed in advance of Hong Kong’s holiday Monday.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.68 versus 6.69 yesterday

- CNY/EUR 7.91 versus 7.91 yesterday

- Yield on 1-Day Government Bond 1.10% versus 1.20% yesterday

- Yield on 10-Year Government Bond 3.20% versus 3.17% yesterday

- Yield on 10-Year China Development Bank Bond 3.75% versus 3.73% yesterday