Ping An’s Q3 Results Weigh On Financials Highlighting Index Sector Weight Disparity

3 Min. Read Time

Upcoming Events

I invite you to join my colleague Nancy Davis tomorrow at 11 am ET for a conversation on how to hedge market volatility stemming from the US election and the uncertain path of stimulus and inflation.

Click here to register!Key News

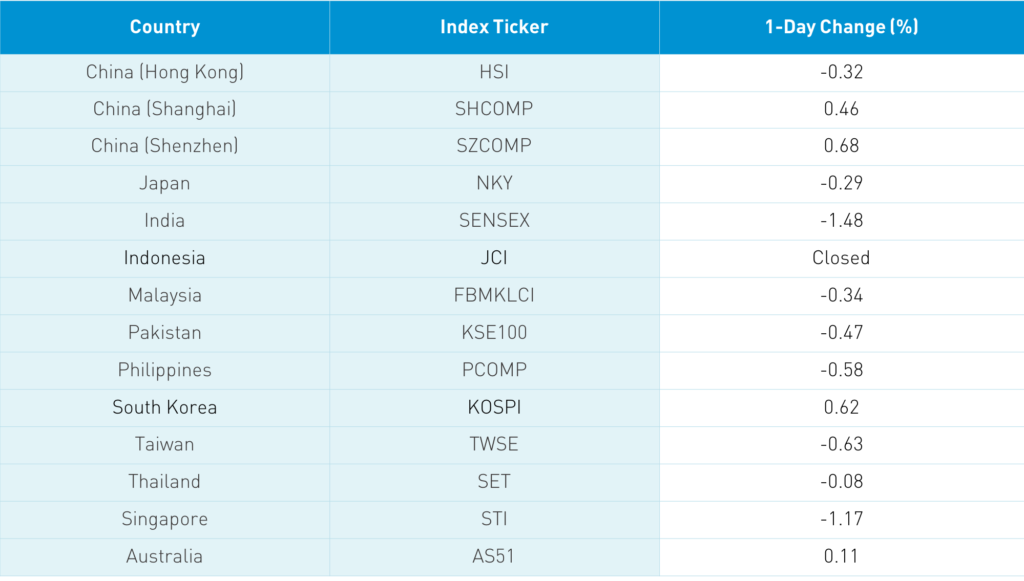

Asian equities were largely weak on rising coronavirus cases globally, though Mainland China and South Korea outperformed. While most quote the Kospi for South Korea, which rose +0.62% today/+6.7% YTD, it is worth noting that the Kosdaq rose +2.87%/+20% YTD. Today’s market action will highlight the disparity of investor’s definition of China. The catalyst was Ping An Insurance’s light Q3 earnings as new business fell -27% YTD year-over-year. Despite Q3 profit rising 8% and net income rising 7.8% year-over-year, investors were disappointed with the weak new business, which led to weakness in financial stocks in both the Mainland and Hong Kong.

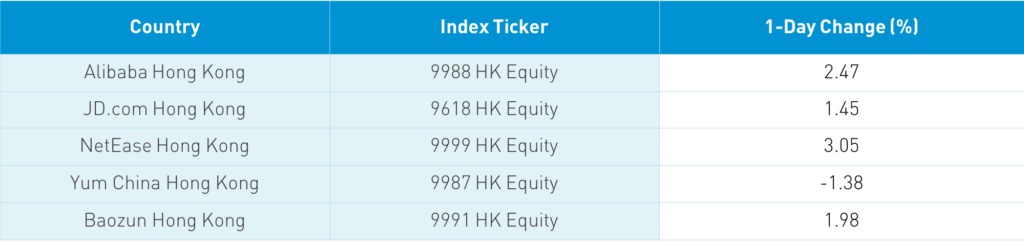

There was a very large disparity between value sectors and underperforming growth stocks in both Hong Kong and the Mainland. Financials’ high sector weight within certain indices is going to weigh heavily on those ETFs. This reminded me of this past weekend’s WSJ article on the value-oriented investment firm AJO closing due to poor performance as slow low growth sectors are out of favor, which has been exacerbated by coronavirus quarantines. Hong Kong volume leaders were Tencent, which gained +2.74% on chatter of the company investing in British music company Instrumental, Alibaba Hong Kong, which gained +2.47%, Meituan Dianping, which rose +5.26%, Ping An, which fell -3.19%, Hong Kong Exchanges, which was up +3.51%, Xiaomi, which gained +1.42%, and BYD, which rose +5.45%. Once again, the Hang Seng Index, which is only 50 stocks, was down due to its high financial sector weight (44%) despite the fact that Tencent and Alibaba were up.

Looking at the Chinese companies listed in Hong Kong within the MSCI China All Shares, Chinese companies listed in Hong Kong were up today. It is worth noting that Tencent has had large inflows via the Southbound Stock Connect platform the last several days. Despite financials’ weakness, Mainland China had a positive day with growth stocks outperforming along with Kweichow Moutai, which rose +2.45%. There is chatter that the pace of Mainland IPOs might slow, which would alleviate the pressure on existing shares due to new supply. One broker noted that earnings season for Mainland stocks will kick in over the next week. Foreign investors were net buyers of Mainland stocks, breaking the outflow streak of eight days.

CNY was off slightly versus the USD overnight as the PBOC removed a “counter-cyclical factor” in the pricing of CNY. The counter-cyclical was meant to dampen big swings in the currency as China’s currency depreciated versus the USD in 2017. The removal is driven by the renminbi’s strong appreciation versus the dollar of late. I don’t think this is a big deal.

US-listed Chinese live-streaming companies are apt to be weak this morning on new rules governing the sector from regulators. The challenge with live streaming is the “live” aspect as anti-pornography rules are difficult to enforce apparently.

Education firm New Orient (ticker EDU) will relist on November 9th in Hong Kong.

US-listed online auto sales company Autohome (ATHM US) announced an investment in a used car platform called TTP.

H-Share Update

The Hang Seng Index bounced around the room to close down -0.32%/-78 index points to close at 24,708. Volumes were +1% from yesterday which is above the 1-year average while breadth was off with 9 advancers and 40 decliners. The 204 Chinese companies listed in Hong Kong within the MSCI China All Shares Index rose +0.65%, led by discretionary +3.43%, communication +2.09%, and tech +0.7%, while energy fell -2.09%, financials -1.68%, utilities -1.47%, materials -1.11%, and industrials -1%. Southbound Stock Connect volumes were moderate with Mainland investors buying $1.222 billion of Hong Kong stocks as Southbound trading accounted for 12.5% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen opened lower but climbed higher the remainder of the day up +0.46% and +0.68% at 3,269 and 2,239 respectively. Volume gained +16% to just below the 1-year average while breadth was mixed with 1,697 advancers and 1,977 decliners. The Mainland companies within the MSCI China All Shares Index rose +0.78%, led by discretionary +3.25%, staples +2.16%, materials +1.25%, and communication +1.14%, while real estate was off -1.19%, and financials -0.57%. Northbound Connect volumes were light/moderate as foreign investors bought $27mm of Mainland stocks as Northbound Connect trading accounted for 7.1% of Mainland trading.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 7.02 versus 6.88 yesterday

- CNY/EUR 7.89 versus 7.94 yesterday

- Yield on 1-Day Government Bond 1.70% versus 1.70% yesterday

- Yield on 10-Year Government Bond 3.18% versus 3.16% yesterday

- Yield on 10-Year China Development Bank Bond 3.67% versus 3.71% yesterday