Growth Stocks Driven Higher as Singles Day Kicks Off, Five Year Plan Lifts Electric Vehicles & Clean Energy

4 Min. Read Time

Key News

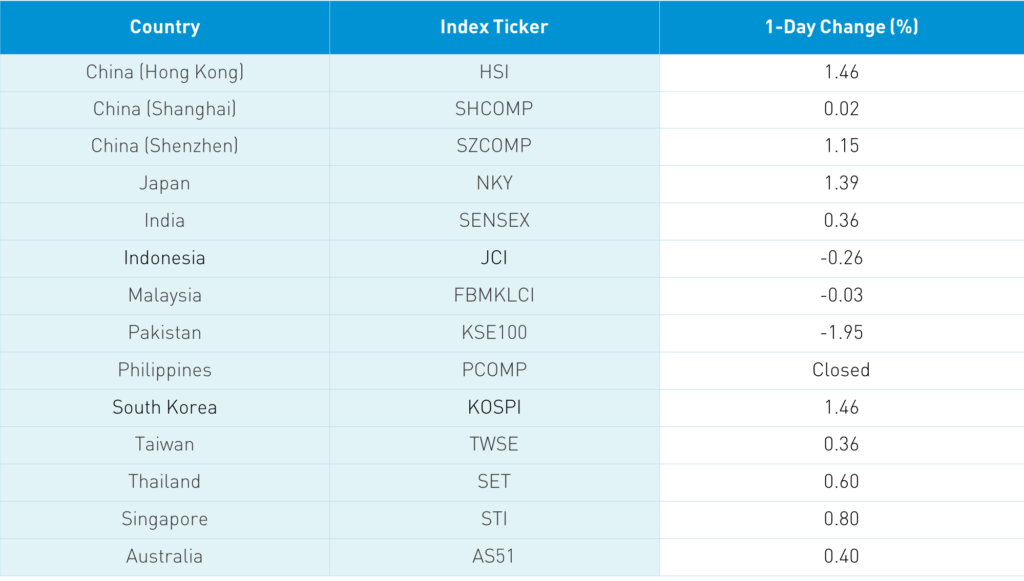

Asian equities had a strong day despite the US equity market’s weakness Friday and increased lockdowns in Europe. Meanwhile, Japan announced the easing of travel restrictions for several countries in the region. The Wall Street Journal noted the out-performance of stock markets in Asian countries that have largely contained the virus’ spread versus the US, where equity markets are hoping the coronavirus can be controlled. After having gone several months without knowing anyone who has contracted coronavirus, four people in my social/kids’ sports/school ecosystem have tested positive in the last week in a worrisome sign.

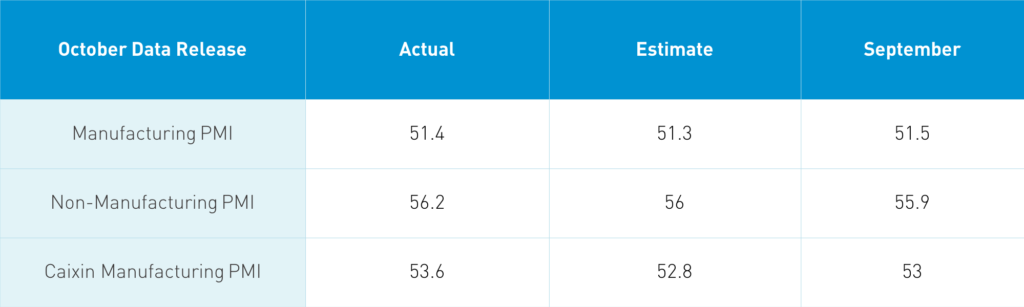

Takeaway: The “official” PMIs were released Saturday morning China time while the Caixin/”private” PMI was released Monday prior to the market’s open. By way of background, the “official” PMIs are a broad survey of large companies while “private”/Caixin is a smaller sample size of private companies with IHS Markit responsible for the survey of small and medium companies. Both PMIs are diffusion indexes measuring growth month over month with readings over 50 showing growth and readings under 50 indicating contraction. The manufacturing PMI showed strength across the board as output continued to grow along with new orders in both exports and imports while inventories shrank. The non-manufacturing PMI also saw new orders increase though new export orders did contract. Business expectations were very strong in both PMIs. The Caixin Manufacturing PMI was driven by stronger output and new orders while the rate of growth for exports did slow. IHS noted that exports continue to be affected by the economic consequence of global quarantines. That being said, business expectations did rise to the highest level since August 2014. Summing it up, the readings are further evidence that China’s economy is experiencing a V-shaped recovery.

The Hang Seng Index had a strong day gaining +1.46%, albeit on low volumes as Hong Kong’s GDP grew +3% in Q3 year over year, ending a streak of five quarters of negative GDP growth. Alibaba’s Singles Day e-commerce extravaganza kicked off this weekend, sending Alibaba HK up by +1.57%. There are reports that Ant Group’s shares are up +50% in the OTC/grey market pre-IPO.

Hong Kong’s volume leader overnight was Tencent, which gained +1.78% as the stock benefits from re-rating due to Ant Group’s IPO, strong online gaming numbers, and talk of tracking Prosus’ share buyback plan. Tencent had another monster day of buying from Mainland investors via the Southbound Connect trading platform. There is broker chatter that Bytedance competitor Kuaishou, in which Tencent invested, is going to file for a Hong Kong IPO as soon as next week.

Geely Auto ripped +13.57% on high volumes as electric vehicle policies take center stage in the new Five year Plan. Meituan Dianping gained +2.22% while Xioami gained +0.45% and EV bus maker BYD gained +12.72%. Macau casino stocks had a decent day as October gaming data improved off a low base.

It is interesting to note that healthcare was off a touch despite the increase in global coronavirus cases. Shanghai and Shenzhen diverged, gaining +0.02% and +1.15%, respectively, as growth names outpaced value names and mid and small caps outpaced large caps. The new Five Year Plan’s emphasis on innovation likely helped lift growth names. Mega caps were off on the day as banks were weak on worries of an increase in loan defaults though brokers were very strong on IPO rules being amended.

Apple’s supply chain stocks were strong along with appliance makers, EV and clean energy stocks. Last week was a monster day for Mainland earnings as CICC reported that A-shares earnings grew 17% in Q3 year over year while ex-financials earnings grew 30%. Foreign investors were net buyers of Mainland stocks today while CNY appreciated slightly versus the US dollar.

Alibaba (BABA US) will report quarterly results on Thursday. The choice of Thursday is interesting as it coincides with the Ant Group IPO. The conspiracy theorist would say an in-line result might be overshadowed by Ant Group’s IPO. It is hard to say, though we’ll know soon enough. Strong economic data especially online retail sales would mitigate that concern.

South Korea’s Damwon Gaming team won this weekend’s League of Legends world championship. I haven’t been able to find the prize amount though it was hard not to notice the tournament’s high profile sponsors such as Red Bull, Louis Vuitton and smartphone maker Oppo.

This past weekend’s Investor’s Business Daily highlighted 5G smartphone shipments by region. Greater China had just over 150 million 5G phones produced in 2020, accounting for 62% of global shipments. In 2021, that number is estimated to double to over 300 million though the percentage of market share will decline as other regions play catch up.

H-Share Update

The Hang Seng opened higher and kept going to close +1.46%/+352 index points at 24,460. Volume plunged -23% from Friday, placing it below the 1-year average while breadth was positive with 35 gainers and 14 decliners. The 204 Chinese companies within the MSCI China All Shares Index gained +1.7% led by discretionary +3.27%, materials +2.94%, financials +2.45%, and communication +1.86%. Meanwhile, utilities and staples lagged -0.34% and -0.17%, respectively. Southbound Stock Connect volumes were moderate/light with Mainland investors buying a net $907 million worth of Hong Kong stocks today as Southbound Connect trading accounted for 13.6% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen had a choppy session but rallied later in the session to close +0.02% and +1.15% at 3,225 and 2,223, respectively. Volume was off -6.9%, placing it just above the 1-year average while 1,834 advancers and 1,914 decliners. The 518 Mainland stocks within the MSCI China All Shares Index gained +0.7% led by utilities +2.53%, discretionary +2.5%, industrials +1.55%, materials +1.44%, and tech +0.95%. Meanwhile, healthcare and financials fell -0.38% and -0.25%, respectively. Northbound Stock Connect volumes were moderate as foreign investors bought $460 million worth of Mainland stocks as Northbound Connect trading accounted for 5.8% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.70 versus 6.69 Friday

- CNY/EUR 7.78 versus 7.82 Friday

- Yield on 1-Day Government Bond 1.91% versus 2.05% Friday

- Yield on 10-Year Government Bond 3.18% versus 3.18% Friday

- Yield on 10-Year China Development Bank Bond 3.65% versus 3.67% Friday