Ant IPO Delay: Key Considerations

3 Min. Read Time

Key News

Ant Group’s Shanghai and Hong Kong IPOs have been postponed. This past weekend Jack Ma made several remarks about financial regulators and banks stifling financial innovation at the Bund Summit. Yesterday, it was reported that regulators met with Mr. Ma and other Ant Group executives. A common misperception of Westerners toward China is that we view it as one single entity. The reality is that China is highly fragmented geographically combined with a massive population. Competition in China is fierce amongst companies as rivals fight it out against one another. Like here in the US, Chinese tech companies are disruptors infringing on very profitable businesses as Richard Branson called “challenger brands”. Banks in China are powerful entities connected politically just as they are here, and rightfully so as banks play an important role in the economy. Ultimately, I believe Mr. Ma may have flown a little too close to the sun with his comments.

There is public relations consequence for Chinese regulators and stopping such a high-profile IPO and the press around it is less than favorable. Logistically a lot of money has been raised for the IPO, which will be creating significant headaches. Do bankers return the money or hold on to it in hopes of a quick resolution? If the money is returned, it could ironically flow back into the stock market. Regulators will have to make a quick decision on allowing Ant Group to refile with new regulatory disclosures or to put it on hold. Regulators appear keen to tighten lending rates, which will affect Ant Group’s online lending unit, which accounted for 39% of revenue. I would lean towards a quick resolution as putting the IPO on ice would ultimately hurt retail investors who the regulators are responsible for protecting. Several large Chinese pension funds, including the National Security Fund, allocated to the IPO. Remember our go-to indicator on headline risk – CNH, China’s currency that trades during US trading hours. CNH has appreciated versus the USD thus far this morning.

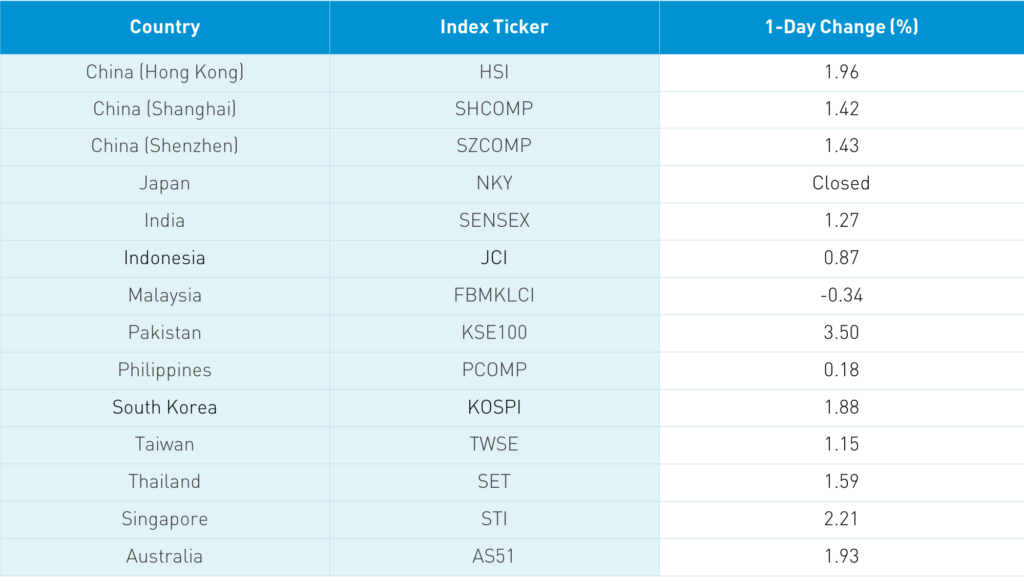

Asian equities had a very strong day with virtually every market showing a +1% gain, though Japan missed out on the fun with a market holiday for Culture Day. The Hang Seng Index gained +1.96% led by volume leaders Tencent, which fell -0.58%, Meituan Dianping, which rose +0.48% on chatter that it could list in the Mainland, Geely Auto, which gained +5.53%, Alibaba Hong Kong, which was up +0.67% on news that it will invest $300mm in luxury goods platform Farfetch, Xiaomi, which gained +0.455, Sunny Optical, which rose +7.8%, Semiconductor Manufacturing, which was up +4.61%, and AIA, which rose +6.27% after it was approved to operate in a Mainland province. Several themes played out both in Hong Kong and the Mainland as Electric Vehicles (EV) saw some profit-taking, though miners rallied based on the commodities needed for EV, tech did well on demand for computers from Singles Day and several value sectors played catch up today to the growth rally we’ve seen of late. Mainland China also had a strong day with Shanghai and Shenzhen up +1.42% and +1.43% respectively. Foreign investors bought a healthy $467mm of Mainland stocks today as CNY rallied versus the USD.

New Oriental Education (EDU US) continues the trend of US-listed Chinese companies listing in Hong Kong. According to Bloomberg, the company is scheduled to list 8.51mm shares, raising $1.3B. The Hong Kong ticker will be 9901 Hong Kong.

Earnings announcement dates are being released.

- Thursday - Alibaba and Autohome

- Friday - Baidu and iQIYI

- 11/10 - Tencent Music Entertainment

- 11/11 – Huya and Douyu

- 11/12 – Tencent and Joyy

- 11/13 – Weibo, VIPS, Trip.com, SINA

- 11/14 – JD.com and Meituan Dianping

- 11/18 – Bilibili

- 11/19 – Netease

- 11/20 – Pinduoduo, GSX and Baozun

H-Share Update

The Hang Seng opened higher and continued that way up +1.96%/+479 index points to close at 24,939. Volumes were up +11.57%, which is above the 1-year average while breadth was strong with 47 advancers and 2 decliners. The 204 Chinese companies listed in Hong Kong within the MSCI China All Shares Index rose +0.84%, led by energy +2.75%, tech +1.99%, real estate +1.87%, materials +1.86%, industrials +1.66%, financials +1.44% , utilities +1.44%, and discretionary +0.91% while communication was off -0.31%. Southbound Connect volumes were moderate as Mainland investors bought $949mm of Hong Kong stocks today as Southbound trading accounted for 12.4% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen gained +1.42% and 1.43% to close at 3,271 and 2,255 as volume contracted -3.4% which is just below the 1-year average. Breadth was strong with 3,211 advancers and 568 decliners. The 518 Chinese companies within the MSCI China All Shares Index gained +1.6%, led by materials +2.42%, financials +2.19%, communication +2.02%, health care +17%, tech +1.69%, energy +1.61%, real estate +1.53%, utilities +1.34% and staples +1.2%. Northbound Stock Connect volume was moderate as foreign investors bought $467mm of Mainland stocks today as Northbound Connect trading accounted for 6.1% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.68 versus 6.69 yesterday

- CNY/EUR 7.82 versus 7.78 yesterday

- Yield on 1-Day Government Bond 1.71% versus 1.91% yesterday

- Yield on 10-Year Government Bond 3.18% versus 3.18% yesterday

- Yield on 10-Year China Development Bank Bond 3.65% versus 3.65% yesterday