Bytedance’s China Rival Kuaishou Files For Hong Kong IPO, Week In Review

5 Min. Read Time

Week In Review

- Hong Kong and Mainland China markets began the week on good footing thanks to a positive October economic release and hints from policymakers that the new Five Year Plan will include market-friendly policies, especially for electric vehicles and clean energy.

- Ant Group's IPO in Hong Kong and Shanghai has been postponed due to regulators' warnings that they will be compelled to treat the company as a bank rather than just a technology company.

- Asian and China markets shook off the IPO postponement in Wednesday trading as a consensus opinion was formed that it will be another six months until Ant lists publicly.

- Alibaba released Q3 results Thursday that beat analyst estimates across the board. The positive release comes in the lead-up to the company's monumental "Singles Day" sales event on and around 11/11, which brought in $38 billion in revenue last year.

Key news

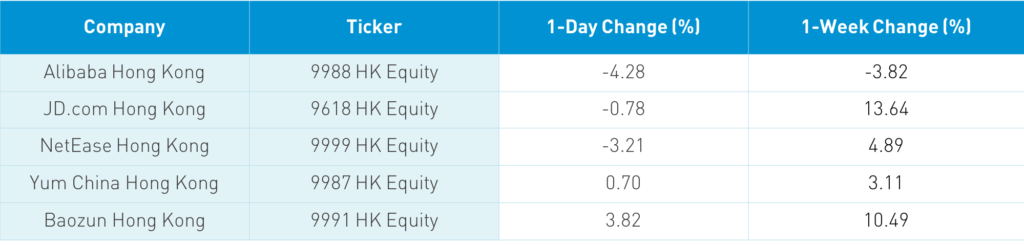

Asian equities ended the week on a high note accompanied by strong volumes outside of Mainland China, which saw profit taking today. Check out the week's returns, which were universally strong. Investors are finally taking note of Asia's outperformance as Europe and the US see an unfortunate pick up coronavirus cases, a trend that has been overshadowed by the election. The Hang Seng Index pulled a James Bond (RIP Sean Connery) gaining +0.07%. Volume leaders in Hong Kong were Alibaba HK, which fell -4.28%, Tencent, which fell -1.68%, BYD, which fell -1.62%, Xiaomi, which gained +3.51%, Meituan Dianping, which fell -0.85%, Geely Auto, which fell -2.34%, Ping An Insurance, which gained +0.49%, and AIA, which gained +0.25%.Growth names, especially Electric Vehicles and internet, saw some profit taking, while value plays played catch up.

It was funny to see the headlines trying to make sense of Alibaba's great quarterly results in light of the stock's decline. As we mentioned yesterday, Alibaba's China e-commerce growth rate came in a touch light at 26%, which is the likely culprit, along with the disappointment of Ant Group's IPO pulling pulled. That being said, Alibaba has good news coming with its Singles Day shopping extravaganza next week, which is akin to Black Friday or Cyber Monday in the US.

In a rare development, Mainland investors were net sellers of Hong Kong equities, though by a small amount, after having invested significant sums earlier in the week. Shanghai and Shenzhen were off slightly, -0.24% and -0.77%, respectively, as our DND trade (drugs/i.e. pharma stocks and drinks/i.e. alcohol stocks) took a hit. Pharma stocks were off on talk that China's drug procurement could be expanded to include heart stents as at a significantly lower price than currently. Mainland autos did well along with appliance makers. Foreign investors invested another $602mm overnight bringing the weekly total to $3.230B and YTD $15.965B.

In the early 1990s, there was a fairly awful movie starring Don Johnson and Mickey Rourke called "Harley Davidson and Marlboro Man". It's the type of movie that only appeals to adolescent males with nothing better to do. Having attended an all-boys boarding school, my school mates and I fit the bill, which explains my unhealthy knowledge of the movie. A line from the movie that still sticks with me is "always kick a man when he is down as you'll never get a better a chance." One of the Chinese rivals of Bytedance, which is popular in the West for TikTok, is short video and live streaming platform Kuaishou. The company was founded in 2011 and backed by Tencent. Yesterday, it filed for a Hong Kong IPO to be led by Morgan Stanley, Bank of America Securities, and China Renaissance. The company looks to raise funds while its rival deals with the US government's questions on privacy issues for Tiktok. It is worth noting that Bytedance is rumored to be raising money themselves, which could value the company at $180B. With that said, the 733 page Kuaishou filing highlights several intriguing aspects of the company:

- 302mm daily users

- 776mm monthly users

- +85 minutes per daily user spent with an average 10 daily visits

- ~26% of monthly users post content with 1.1B videos post per month

- E-commerce gross merchandise value RMB 109.6B "through the sale of virtual items"

- Revenues grew from RMB 8.3B in 2017 to +143% RMB 20.3B in 2018 to +92.7% RMB 39.1B in 2019 to + 48.3% RMB 25.3B in the six months ended June 30, 2020

- Live steaming accounted for 4.2%/RMB 416B of China's retail e-commerce market in 2019 but could great to 23.9%/RMB 6.417 trillion by 2025

- The company has been profitable but appears to have thrown the sink at selling/marketing expenses and R&D recently though I would expect the next filing for the full 9 months to improve.

- PE investors include DST, Baidu, Sequoia, Temasek

The Wall Street Journal had a good article today titled "U.S. Firms Get Another Boost From China" as US companies oriented to Chinese consumers saw a pickup in China activity, offsetting global weakness. Per the article, in Q3 Cummins China revenue +46%/global revenue -11%, Daimler China +24%/global -8%, GM China +12%/-10% US, Ford China +22%/-5% globally. The article also mentions agriculture companies ADM and Bunge's positive comments on China revenue growth. Separately, I noticed a Mainland media source noted that ADM is expected to sign several billion dollar deals at the China International Import Expo taking place in Shanghai. I highly recommend you check out the article!

Alibaba and Richemont are investing $300 million each in online luxury goods company Farfetch and another $250 million each into a new joint venture that will pipe Farfetch into Alibaba's e-commerce ecosystem. Coincidentally, I noticed that Tencent inked a deal with Burberry to promote the brand in its "Honour of Kings" video game.

October Export, Import data and trade balance should be reported over the weekend. CPI and PPI for October will be released on Monday.

H-Share Update

The Hang Seng pulled off a James Bond +0.07%/+17 index points to close at 25,712 as turnover was off -6.84% from yesterday but still 140% above the 1-year average. Breadth was positive with 32 advancers and 16 decliners. The 204 Chinese stocks within the MSCI China All Shares Index fell -0.17% with materials +2.06%, tech +1.96%, and utilities +1.51%. Meanwhile, staples -1.79%, communication -1.27%, health care -1.19%, and industrials -0.28%. Southbound Connect volume was light as Mainland investors sold $43mm of Hong Kong stocks today as Southbound Connect trading accounted 9.6% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen were off -0.24% and -0.77% to close at 3,312 and 2,282, respectively, as volume rose +2% to 111% of the 1-year average. Breadth was off with 1,042 advancers and 2,679 decliners. The 518 Chinese stocks within the MSCI China All Shares Index gained +0.1% led by energy +1.48%, discretionary +1.18%, materials +1.16%, tech +0.8% and real estate +0.79%. Meanwhile, health care -2.28% and staples -0.41%. Northbound Stock Connect had foreign investors buying $602 million worth of Mainland stocks as Northbound Connect trading accounted for 6.2% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 6.61 versus 6.61 yesterday

- CNY/EUR 7.86 versus 7.80 yesterday

- Yield on 1-Day Government Bond 1.61% versus 1.56% yesterday

- Yield on 10-Year Government Bond 3.21% versus 3.19% yesterday

- Yield on 10-Year China Development Bank Bond 3.67% versus 3.66% yesterday