Revenge of the Value Nerds as Singles Day Kicks Off

3 Min. Read Time

Key News

Asian equities were mixed with Japan, Singapore, Malaysia, and Thailand outperforming while Mainland China and Taiwan lagged. Growth/WFH names are being sold globally to fund reopening/value stocks. Semiconductor-heavy Taiwan was off -0.35% while South Korea’s Kospi rose +0.23% as Kosdaq fell -1.22%. Large cap/value Shanghai was off -0.4% while mid/small cap growth Shenzhen was off -1.05%. The financial heavy Hang Seng was up +1.1% while the growth Hang Seng Tech fell -5.15%. In China, there was coverage that the regulator would look at monopolistic practices in the internet space, which didn’t help Hong Kong-listed stocks. However, this was by no means the culprit as non-internet technology stocks were also taken to the woodshed.

Hong Kong volume leaders (more like bleeders) were Tencent, which fell -4.42%, Meituan Dianping, which was off -10.5%, Alibaba Hong Kong, which dropped -5.1%, JD.com Hong Kong, which fell -8.78%, Xiaomi, which was off -4.31%, AIA, which gained +5.71%, Ping An Insurance, which rose +1.43%, HSBC, which was up +8.18%, and BYD, which fell -5.87%. Mainland China was a similar story as outperforming sectors were hit, though mid and small caps outperformed. A day after foreign investors bought $2.97B of Mainland stocks, they trimmed -$620mm. Foreign investors were net sellers of Shenzhen stocks and buyers of Shanghai stocks. CNY was stable overnight at 6.61.

Yesterday I had the pleasure of speaking with CNBC’s Bob Pisani on the ETF Edge program (cnb.com/ETF-edge/). China, which had its quarantine in the first quarter, provides a great preview of what is likely to play out globally, given that it is now two quarters out of quarantine. Chinese growth names have continued to outperform post-quarantine as the habits formed in quarantine have stuck, flowing through to their earnings. Asia can’t WFH because of urbanization (ie. apartments), but that isn’t true here in the US. The main catalyst for US value stocks would be a steepening yield, which will help bank stocks. The question is: does a rising US yield curve take the wind out of non US growth stocks? US FAANG stocks need to generate huge amounts of revenue to justify their current prices, which makes a value rally feasible. For China, we know growth names delivered on earnings post-quarantine in Q2. Now we are in Q3 earnings season. What happens if the China growth names deliver on earnings again? Think about this: by 11am EST today, Alibaba will start releasing Singles Day data. Think that will be good news? Me too!

Post-close, Tencent Music Entertainment reports earnings and MSCI provides the pro-forma for the month end Semi-Annual Index Review.

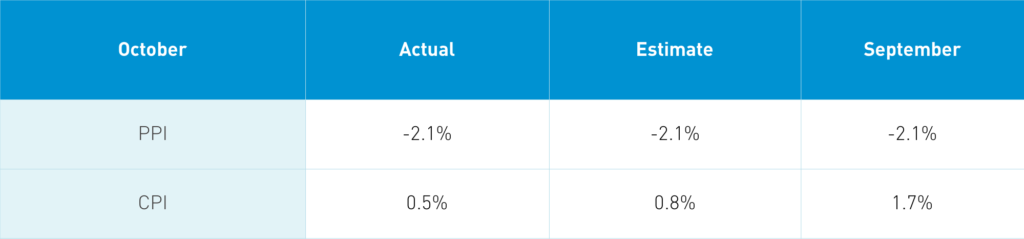

Takeaway: CPI was light driven by lower pork prices. Less food, China's CPI inflation came in somewhat light at +0.5%. The data release wasn’t a market mover in light of the rotation occurring.

H-Share Update

The Hang Seng gained +1.1% to close at 26,301 as volume rose +38% from yesterday to 200% of the 1-year average. Breadth was positive with 37 advancers and 13 decliners. The 204 Chinese companies within the MSCI China All Shares Index fell -1.88%, as energy +9.76%, industrials +1.96%, staples +1.65%, and real estate +1.55%, while discretionary fell -6.27%, tech -4.4%, communication -3.86%, and healthcare -2.24%. Southbound Stock Connect volumes were high as Mainland investors sold $150mm of Hong Kong stocks as Southbound trading accounted for 10% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen were off -0.4% and -1.05% to close at 3,360 and 2,308 respectively. Volume was off -9.6% from yesterday, though still 121% of the 1-year average. Breadth was off with 1,022 advancers and 2,755 decliners. The 518 Mainland stocks within the MSCI China All Shares Index fell -1.22%, led lower by discretionary -3.12%, health care -2.38%, tech -2.08%, utilities -1%, real estate -0.95%, industrials -0.87%, etc. Northbound Stock Connect volumes were moderate as foreign investors sold -$621mm of Mainland stocks as Northbound trading accounted for 5.5% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 6.62 versus 6.63 yesterday

- CNY/EUR 7.82 versus 7.86 yesterday

- Yield on 1-Day Government Bond 1.91% versus 1.81% yesterday

- Yield on 10-Year Government Bond 3.22% versus 3.24% yesterday

- Yield on 10-Year China Development Bank Bond 3.70% versus 3.71% yesterday